A long put butterfly is a limited profit, limited risk options strategy used when an investor expects moderate downside movement in the underlying asset. Long put butterfly involves buying a put spread and selling a put between the spread strikes to finance the trade and reduce cost. Maximum profit occurs if the underlying is at the short put strike at expiration. Profit is capped between the difference in strikes less net debit paid. The maximum loss happens if the underlying is above the higher strike or below the lower strike. Loss is limited to the net debit.

A long-put butterfly benefits from a moderate downside forecast in the underlying asset. As the short put decays faster than the long puts due to higher theta, profitability increases if the underlying drops slightly below the short put strike. It is a defined risk strategy allowing traders to profit from a directional downward forecast within a range. It can be used ahead of events with downside uncertainty, like earnings reports.

What is a Long Put Butterfly?

A long put butterfly is an options trading strategy that involves buying a put option with a higher strike price, selling two put options with a middle strike price, and buying a put option with a lower strike price. All the options have the same underlying security and expiration date.

The long-put butterfly strategy aims to profit from the underlying security trading in a range or closing between the middle strike prices at expiration.

The maximum profit is attained when the underlying security closes right at the middle strike price at expiration. The profit is limited to the net credit received when initiating the trade. The risk is also capped at the difference between the wing strike prices minus the net credit received.

There are four separate put option contracts involved. One long put with the highest strike, two short puts with a middle strike, and one long put with the lowest strike. All have the same expiration date.

The upper and lower strike puts are purchased, while the middle strike puts are sold. Typically, the distance between the strike prices is equal. It is named a butterfly spread because the shape of the profit/loss diagram resembles a butterfly’s wings.

The long put butterfly is used when the trader expects low volatility and for the underlying security to be trading in a range through expiration. It benefits from time decay as the options move closer to expiration.

The maximum loss occurs if the underlying security closes below the lower strike or above the higher strike at expiration. The trade loses money if the security closes outside the wings. The breakeven points are at the lower strike price plus the net credit received and the upper strike price minus the net credit received. Entering the trade involves buying the lower strike put, selling two puts at the middle strike, and buying the higher strike put. All options have the same expiration date.

The net debit or credit, when entering the trade, sets the maximum profit cap and affects the breakeven points. Wider wing spreads reduce cost but also limit profit potential. The best case scenario, if held to expiration, is for the stock to close exactly at the middle strike price. Any close between the middle strikes results in profit.

Is Long Put Butterfly the same as 1-3-2 Butterfly Spread?

The long put butterfly and the 1-3-2 put butterfly are different names for the same options trading strategy. They involve the same structure of buying a put at one strike, selling puts at a middle strike, and buying a put at another outer strike.

They both have a long put wing, a short put body, and another long put wing. These are their main commonalities. There are 4 legs total, with 1 long put, 2 short puts, and 1 long put. Maximum profit occurs if the underlying expires at the middle strike. Defined maximum loss if the underlying finishes outside the wings.

While they refer to the same basic butterfly spread structure, there are a couple of subtle differences in the terminology.

Long put, the butterfly emphasizes the directional bias. It conveys that the trade involves being long put at the wings.

1-3-2 butterfly spread describes the ratio of long to short options. It conveys the specific ratio of 1 long put, 3 short puts, and 2 long puts.

However, these are minor syntactic differences. The core strategy and structure are identical between the long-put butterfly and the 1-3-2 butterfly.

They have the same profit/loss profile – limited profit if finishing at middle strike, defined risk outside wings.

They imply the same market expectation – range-bound trading in the short term.

They benefit from the same factors – time decay and low volatility.

They have the same breakeven points.

They involve the same options, positions and ratios.

Long put butterfly and 1-3-2 put butterfly are different terminologies to describe the same spread trade.

Buying OTM put wing, Selling 2 ATM puts, Buying OTM put wing, all the same expiration, For net debit or credit, profit with stock at the middle strike at expiration.

The only distinction is that long put butterfly emphasizes directional bias, while 1-3-2 butterfly specifies the ratio. But in practice, they define identical trades.

What is the importance of the Long Put Butterfly in Options Trading?

The long put butterfly is an important instrument in the options trader’s toolkit as it provides a way to express a forecast for low volatility and range-bound prices leading up to options expiration. The long put butterfly serves six strategic purposes in options trading.

First, it offers a defined risk profile. The maximum loss is capped to the wings’ widths minus the net credit received. This limit on downside is attractive for traders wary of uncapped risk in other strategies.

Second, the long-term butterfly benefits from time decay. As the options move closer to expiration, the value decays – especially for the short options. This erodes the premium paid and produces profits. Managing time decay is crucial in options trading.

Third, the long-put butterfly has split directional exposure. The wings provide long-term exposure to benefit from a decline. But the body’s short puts mean some offsetting positive delta exposure. This dual-directional outlook is unique.

Fourth, it is a relatively inexpensive strategy. With 4 legs, it is established for a net credit or small debit. Many other multi-leg approaches require greater capital outlay. The lower cost makes long-put butterflies more feasible.

Fifth, it has a high probability of profit if the forecast is accurate. The whole credit is realized as profit if the underlying remains within the centre of the strike prices. This probabilistic edge is desirable.

Sixth, risk is shifted from the wings to the body. The highest likelihood of expiration OTM lies with the body shorts. This focuses on risk in the high probability area.

The long-put butterfly is especially useful when neutral volatility and prices are expected in the near term until expiration.

How does Long Put Butterfly work?

A long put butterfly spread is an options trading strategy constructed using only put options that are designed to profit from a moderate price decline in the underlying asset. It involves a specific configuration of puts at different strike prices to create a risk/reward profile resembling a butterfly shape.

The long put butterfly is constructed by the following steps mentioned below.

Buying a lower strike out-of-the-money put.

Selling two or more at-the-money or middle strike puts.

Buying another higher strike out-of-the-money put.

The mechanic behind how long put butterflies work relates to the shape created by the different puts at varying strikes. The sold puts at the middle strike create the body of the butterfly. This defines the maximum profit zone if the asset settles here at expiration after a moderate decline.

The wings are formed by the long puts at the lower and higher strikes, which create defined breakeven points. Losses start to mount if the asset closes below the lower strike put or above the higher strike put. This defines the maximum loss.

The trader profits if the asset price declines moderately and finishes within the body between the middle strike short puts at expiration. The wings limit both the profit potential and the amount of capital at risk.

The at-the-money or middle strike short puts create the body of the long-put butterfly. This defines the ideal settlement price at expiration to achieve maximum profit. Selling these puts also generates income to offset the cost of the wings.

The wings composed of the lower and higher strike long put create the defined maximum profit zone and breakeven points. The breakevens represent where losses begin accumulating if the settlement price moves beyond them.

Maximum profits exist between the breakeven points established by the wings. The maximum loss is also established if the price settles below the lower strike put or above, the higher strike put comes expiration.

The long-put butterfly works best under a moderately bearish outlook. The trader profits within the body range at expiration. Large upside or downside price moves beyond the wings result in losses.

Selling the extra puts at the middle strike generates premium income, which reduces the net debit cost. This credit offsets the price paid for the lower and higher strike long puts.

The wings clearly define profit zones versus loss zones, allowing better risk management compared to just buying puts outright. The maximum loss is known at the outset.

Long put butterflies work by utilizing a carefully constructed body and wings position using options at different strikes to express a view on the moderate downside in the underlying asset price. The wings establish limited profit and risk, while the body creates the ideal settlement price at expiration. The trader makes money when the asset drops gradually into the body.

How commonly do traders use the Long Put Butterfly strategy?

The long put butterfly is a moderately popular options trading strategy but not necessarily extremely common compared to some other spreads.

The long-put butterfly options strategy sees decent but not extremely heavy usage among options traders. It occupies a niche for expressing a view on the moderate downside in the underlying asset. Traders sometimes utilize long-put butterflies selectively for certain situations, but other bearish strategies tend to see more widespread regular usage overall.

Reasons the long put butterfly sees moderate but not extremely high usage are the following.

Profits require a specific moderate price decline.

Capped upside beyond wings limits profit.

Requires active management into expiration.

Directional assumption wrong if rally occurs.

Other bearish strategies sometimes have an edge in certain cases.

The long put butterfly is best suited for situations where a moderate price decline is expected, ideally finishing around the middle strike price. This relatively narrow profit zone makes the strategy selective rather than an overtly common high-volume approach.

The profit potential being capped reduces appeal for traders focused on unlimited upside. The requirement to actively manage into expiration also diminishes use among traders looking for more passive positions.

Strategies like long puts, bear spreads, and short selling see more frequent usage for outright bearish market views. In cases where substantial downside is expected, these strategies sometimes provide greater profit potential.

However, the long-put butterfly does occupy a niche among options traders, preferring defined and limited risk. It is used selectively when moderate declines are anticipated, providing an efficient use of capital with leverage compared to long puts alone.

The usage frequency tends to be higher among experienced options traders with the knowledge to deploy this specific strategy in the appropriate situations. Less experienced traders sometimes gravitate toward simpler directional long puts or bear put spreads.

The long-put butterfly also sees more frequent use when option prices are elevated due to high implied volatility. The ability to profit from IV contraction expands the appeal.

How to Construct a Long Put Butterfly?

A long put butterfly spread is constructed by buying and selling puts at three different strike prices. The stages of establishing the post are listed below.

Select the underlying asset you want to trade options on. This could be a stock, ETF, index, or futures contract. The liquidity of the options contracts will impact construction.

Define your market thesis. A long put butterfly profits from a moderate downside in the underlying asset price. Predict the potential move and target price range.

Choose the expiration date for the options contracts. The timeframe should provide enough opportunity for your thesis to play out. Typically, 1-3 months out.

Buy a put with a strike below the current underlying price. This creates the lower wing of the structure. The farther out of the money, the lower the cost.

Sell twice as many puts (or more) at the strike that is at or closest to the current market price. This establishes the body and funds the trade.

Buy a put with a strike above the current market price to complete the upper wing. This defines the maximum profit range.

Review the net debit price to establish the full position. The credit from the sold puts should offset some of the cost of the wings.

Analyze the maximum profit versus loss. The wings create defined breakeven points beyond which losses accrue. The body defines max profit.

Send the whole order to concurrently purchase the lower strike put, sell the intermediate strike puts, and buy the higher strike put when you are ready.

Monitor the position regularly. Make adjustments if the forecast is wrong or to protect capital based on movement.

When to enter a Long Put Butterfly strategy?

A long put butterfly options spread is best entered when neutral to moderately bearish market conditions are expected. The long-put butterfly strategy is designed to profit from a moderate price decline in the underlying asset. As a result, ideal entry conditions are neutral to moderately bearish market environments.

Entering a long-put butterfly when the market outlook is overly bullish would contradict the directional assumption of the trade. The best time to deploy a long put butterfly is when the technicals, fundamentals, and sentiment indicate neutral to bearish bias ahead.

Five specific entry conditions that align well with utilizing a long-put butterfly strategy include the following.

Asset is stuck in a trading range or sideways chop.

Mild selling pressure exists in the market.

VIX is relatively low, indicating complacency.

Analysts were mixed and bearishly biased on assets.

Technicals reflect support and resistance boundaries.

These types of neutral to moderately bearish environments provide an ideal backdrop to enter long-term butterfly spreads. The probability of the asset experiencing a modest down move increases under these conditions.

Alternatively, entering a long put butterfly when the VIX is spiking, analysts are overwhelmingly bullish, and the technical chart displays a strong uptrend would be ill-advised. The directional assumption would have a low probability of playing out.

The ideal conditions align more with range-bound and mildly bearish markets. The trader is looking for the asset to decline modestly in value and expire within the body of the long put butterfly structure after a period of neutral sideways action.

Entering long put butterflies 45-60 days out from expiration takes advantage of time decay accelerating in the final 30-45 days. The short options sold at the body of strikes lose value rapidly if the forecast is correct.

When to exit a Long Put Butterfly strategy?

Knowing when to exit a long put butterfly requires active position management and discipline. Five scenarios that sometimes signal an exit include the following.

Underlying price breaches wings.

Significant time decay is accelerating.

Major change in market conditions.

Better opportunities in different positions.

Loss reaches the maximum pain threshold.

With time left, the price of the underlying asset sometimes indicates an exit if it falls below the lower strike wing or climbs over the higher strike wing. The forecasted move is not playing out, and losses begin accumulating beyond the wings.

As expiration approaches in the last 30-45 days, time decay often accelerates rapidly. With little time left, an early withdrawal may be justified if the trade is far out of the money.

A modification or early withdrawal is sometimes wise if market conditions shift such that the forecast has a low likelihood of happening. For example, if bullish catalysts emerge after entry.

Closing the long put butterfly to free up funds for the new position sometimes makes sense if investigation reveals another trading scenario with a superior risk-reward profile.

A market price exit is sometimes required to preserve money if the unrealized loss approaches the point of maximum discomfort when the trader feels uncomfortable holding any longer.

Long-put butterflies are often closed ahead of expiration week to avoid assignment risk on the short options. Taking at least 50% of profits when available is also advisable.

A trader enters a long 90/100/110 put butterfly on stock XYZ at Rs. 100 per share. The stock rallies to Rs. 105 over the next month. The trader exits the entire position for a loss as it exceeds the higher strike wing.

The upside move contradicts the directional assumption. By exiting, further losses are limited as premiums erode on the long puts. The trader sometimes looks to redeploy capital into a new opportunity.

What is the maximum loss for Long Put Butterflies?

The maximum loss for a long put butterfly spread is defined and limited based on the strikes chosen. The maximum potential loss occurs if the underlying stock finishes below the lower strike or finishes above the higher strike at expiration.

In this worst-case scenario, both long put options expire worthless while the short put options are deep in-the-money. This results in the maximum loss based on the wings’ widths reduced by the initial net credit received for selling the body.

For example, consider a long butterfly consisting of the following.

Long 100 Put

Short 120 Puts

Long 140 Put

The maximum distance between the wing strikes is 140 – 100 = 40 points.

The following will happen if this is decided for a net credit of 5 points.

The absolute maximum loss is 40 – 5 = 35 points.

Or Rs. 3500 per contract since each point equals Rs. 100.

This defined and capped risk is a key feature of the long-put butterfly. Without the long-wing put options, the short-body puts alone have unlimited downside risk if the stock declines aggressively. But combining them with the wings defines and limits the loss.

Of course, most finished long-put butterflies will not reach the absolute maximum loss. But that represents the fundamental worst-case scenario.

In practice, traders close out positions before expiration if losses mount. Allowing the maximum loss at expiration to rarely occur.

For example, if the stock breaches the lower strike, that long put is sometimes closed to lock in some gains and reduce further loss. Active management prevents ballooning to the maximum loss.

What is the maximum profit for Long Put Butterfly?

The maximum profit for a long put butterfly spread is equal to the initial net credit received when establishing the trade. This occurs when the underlying stock is precisely at the middle strike price at expiration after having sold the body shorts and purchased the wings long.

For example, suppose a put butterfly is constructed for a net credit of Rs. 100. In that case, the maximum achievable profit is Rs. 100 per contract at expiration if it closes right at the middle strike.

Unlike many multi-leg strategies, which have unlimited profit potential, the long-put butterfly profit is strictly limited by the net credit amount. Even if the stock moves aggressively higher, the short puts gain value, but the wings cap the profit on that side.

Achieving the full maximum profit requires the stock to be right at the middle strike at expiration. Any deviation above or below reduces profitability from the optimum.

In practice, traders will typically close out the spread at a profit prior to expiration if it achieves a satisfactory gain. For example, if a Rs. 100 initial credit turns into Rs. 150 as expiration nears, the position may be exited at Rs. 150 rather than risk waiting until precisely at the middle strike.

The maximum profit on paper is the original net credit. But traders routinely capture a portion of that profit early if the opportunity presents itself rather than holding all the way to perfection.

The limited profit potential is the tradeoff for the long-put butterfly’s defined and capped risk. The upside is constrained by the credit amount, but the downside is also much more controlled compared to many strategies.

For certain trading objectives, giving up home run upside for better risk parameters is sometimes desirable. The long-put butterfly exhibits this balanced profit/loss relationship.

How does implied volatility affect the Long Put Butterfly?

Higher implied volatility increases the value of both long and short options, while lower volatility reduces values. For the long-term butterfly, volatility has some nuanced effects.

Overall, lower implied volatility is beneficial for the strategy. As volatility declines, the time value priced into the options erodes faster. This dynamically benefits the short options more than the wing longs.

Specifically, diminished volatility enhances the time decay effect, which is central to profiting on a long-put butterfly. The passage of time reduces option value and moves quicker at lower volatility. This amplifies the time decay of the short options.

However, extremely low volatility environments also limit profit potential. Some volatility provides room for the wing values to erode optimally relative to the short options.

Periodic spikes in volatility, for example, around earnings or events, sometimes actually present attractive entry points. This inflates the option values initially to provide better credit when establishing the spread. As volatility reverts lower in the weeks ahead, this magnifies the time decay.

The ideal scenario is initiating after a volatility spike, then benefiting as it declines into expiration.

High sustained volatility is detrimental. It reduces time decay, inflates the short options, and makes reaching the maximum profit at the centre strike less likely.

Overall, the long put butterfly works best played when volatility crushes are expected rather than expansion. Lower volatility enhances the favourable time decay dynamics.

How do traders break even with Long Put Butterfly?

The breakeven points on a long put butterfly spread are the underlying prices at which the trade breaks even – where the losses equal the gains at expiration.

There are two breakeven prices, one above and one below the middle strike price. Reaching either breakeven represents the underlying trading outside the profit range but not exceeding the maximum loss.

The lower breakeven point is calculated by taking the lowest strike price of the wings and adding the initial net credit received for the trade.

For example, if the lower strike is 40, and the credit is Rs. 2, the lower breakeven would be 40 + 2 = Rs. 42.

At this underlying price, the losses on the short puts offset the gain in the low-wing put.

The higher breakeven point takes the higher wing strike and subtracts the initial credit received.

For example, if the higher strike is 60, and the credit is Rs. 2, the higher breakeven would be 60 – 2 = Rs. 58.

At this stock price, the gain in the high-wing put offsets the losses from the short puts.

Below the lower breakeven or above the higher breakeven, the trader begins accruing incremental losses. The breakevens represent where those losses exactly offset the credit collected when opening the trade.

Breakeven points sometimes shift over the life of the trade as options are dynamically repriced by the market.

How does Long Put Butterfly strategy assignment risk occur?

Assignment risk in a long-term butterfly refers to the possibility of having short options assigned and being obligated to fulfil the options contract. For the long put butterfly, assignment risk lies primarily with the short body puts sold at the middle strike.

The short puts become in-the-money and are more likely to be assigned if the underlying stock declines below that intermediate strike.

Assignment typically happens unexpectedly on ex-dividend dates or before earnings releases. The option holder calls away the short puts to capture intrinsic value or dividend payments.

To fulfil assignment, the short put writer must purchase 100 shares per contract at the strike price to deliver to the assigned counterparty. This requires having sufficient cash to handle the assignment.

With the long put butterfly, early assignment of the short puts becomes problematic. It forces the purchase of stock at the middle strike before the wings potentially expire for a profit.

Traders might exercise the long wing puts to counter an early assignment on the shorts. But these caps gain ahead of expiration.

Traders mitigate assignment risk by closing out or rolling the spread as it goes in-the-money. Additionally, avoiding holding shorts into ex-dividend or earnings dates reduces the odds of early assignment.

However, unexpected assignments can still occur and require action to fulfil the delivery and potential stock purchase.

What is the impact of Time Decay on Long Put Butterflies?

Time decay, or theta, is a major factor that impacts the profit potential of a long-put butterfly spread. As options approach expiration, the time value priced into the options declines exponentially. This time decay benefits the short options at the body of the butterfly more than the long options at the wings.

The goal is for time decay to maximize gains on the short puts while the wings retain value. This expands the spread at expiration.

In the final weeks before expiration, the time value erodes rapidly. This dynamic allows the short options sold at potentially inflated values to expire worthless or very low value. As the shorts decay, the trader pockets the premium collected.

Meanwhile, the lower time decay of the wings preserves their protection in case the stock moves outside the range. This imbalance in time decay is core to the strategy.

However, the impact of time decay is not linear. It accelerates in the last month before expiration and even faster in the final two weeks. Traders must consider this curve when planning entry and exit points. Initiating too early reduces decay benefits.

But waiting until too close to expiration offers less protection from the wings as their time premium also rapidly decays.

To maximize time decay, traders want enough lead time for the short puts to erode but not so distant that the wings lose protection power. Typically, initiating long-put butterflies 2-6 weeks out from expiration offers an optimal decay curve.

This balances maximizing erosion of the shorts while retaining sufficient extrinsic value in the wings.

How does expiration risk affect the Long Put Butterfly strategy’s gains and losses?

Expiration risk significantly impacts the profitability of long-put butterfly spreads. Here is an overview of how expiration affects this strategy’s gains and losses.

As a long-put butterfly spread approaches expiration, actively monitor the heightened risks and uncertainty. The final settlement price in relation to the strikes and the speed of time decay acceleration sometimes dramatically sway the trade outcome.

In the last 30-45 days before expiration, closely track how rapidly time decay is accelerating as options lose their remaining time value. For out-of-the-money long-put butterflies, this sometimes severely erodes unrealized gains or amplifies losses. Make adjustments to manage time decay.

Closely follow how the underlying asset price is moving relative to the wings. The biggest risk is finishing below the lower strike long put or above the higher strike long put. This results in the maximum loss condition. Monitor how the probability of the forecast playing out diminishes as expiration nears.

The short puts at the middle strike carry assignment risk if in-the-money at expiration. To avoid being assigned 100 shares per the contract that sometimes ties up additional capital, proactively buy back short puts to mitigate this risk.

As expiration approaches, monitor how bid/ask spreads on the options are trending. Widening spreads erode gains when closing the position. Trading illiquid options exacerbates spread-widening risks near expiration week.

Consider whether pushing the position’s expiration date out further makes sense if the initial premise is still true, but additional time is required. This delays risks but creates costs. Analyse if rolling can be justified.

As expiration nears, active position management becomes essential. Evaluate exiting at a profit, loss, breakeven, or rolling the trade based on the circumstances. Avoid complacency, as doing nothing heightens risks.

Typically, long-put butterflies should be closed by mid-expiration week at the latest to eliminate assignment risk and volatility skew exposure on the short options. Avoid holding into actual expiration.

Long-put butterfly spreads face amplified risks approaching expiration week. Proactively manage time decay, price movement, assignment risk, bid/ask spreads, and overall position outlook to mitigate adverse expiration outcomes. Appropriate action is required to protect capital.

How to adjust Long Put Butterfly?

Traders adjust long-put butterfly spreads in various ways to manage their position and profit from changing market conditions. The goal is typically to reduce cost basis and risk exposure while maintaining or increasing the potential profit zone. One method is rolling the untested short options up, down, or out in strike price and/or expiration date to collect additional credit.

\This brings in premium income to offset the initial debit and lower breakeven points. Traders can also roll the tested short option to repair the spread. If the market moves against the position, they may roll the challenged short put up or out to avoid assignment. In a favourable market, they can roll the tested short put down or stay within the profit zone.

Converting the Long Put Butterfly to an iron condor or custom spread is another adjustment approach. Traders also choose to leg out of certain sides at opportune times to capture gains. Proper adjustments help optimize outcomes for long-put butterfly traders as market conditions evolve over the life of the position.

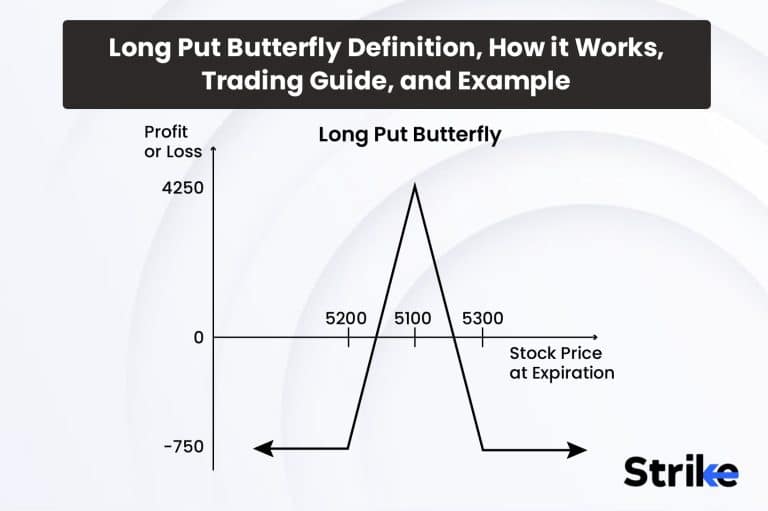

What is an example of a Long Put Butterfly?

Let’s walk through an example of constructing a long-put butterfly spread. We’ll look at defining the trade parameters, placing the orders, calculating profit potential, and evaluating risks.

We’ll use a hypothetical scenario where an investor initiates a long put butterfly in XYZ stock. The stock is currently trading at Rs. 50 per share. The investor believes it will remain stable at around Rs. 50 through the option expiration date in 3 months.

To capitalize on this forecast, they use the following strikes and premiums.

Buy 1 Put at Rs. 45 strike for Rs. 1.00.

Sell 2 Puts at Rs. 50 strikes for Rs. 2.50 each.

Buy 1 Put at Rs. 55 strike for Rs. 4.00.

Trade Setup

By purchasing the lower Rs. 45 strike put, shorting two at-the-money Rs. 50 puts, and buying the higher Rs. 55 strike put, they create a long put butterfly. The cost to enter the trade is a Rs. 1 credit.

Rs. 1 (long 45P)

-Rs. 5 credit (short 2x 50P)

-Rs. 4 (long 55P)

Net credit = Rs. 1

The maximum risk on the trade is the difference between the bought put strikes minus the credit collected. Here it is Rs. 3.

Max Risk = Strike distance – Credit

= Rs. 55 – Rs. 45 – Rs. 1

= Rs. 9 – Rs. 1

= Rs. 3

The maximum reward is obtained if XYZ closes exactly at Rs. 50 at expiration. In that case, the 45P and 55P expire worthless while the 2 short 50P gets assigned. The trader pockets the original Rs. 1 credit as profit.

Now, let’s examine the full profit & loss profile at expiration.

Loss of Rs. 3 if XYZ is less than Rs. 45

Profit between Rs. 1 and Rs. 3 if XYZ is between Rs. 45 and Rs. 50.

The maximum profit is Rs. 1 if XYZ is Rs. 50.

XYZ Rs. 50-Rs. 55: Profit between Rs. 1 and Rs. 3

Loss of Rs. 3 if XYZ exceeds Rs. 55.

We can see the trader profits in a narrow Rs. 5 wide range around the short Rs. 50 strike. Above or below that band results in the maximum Rs. 3 loss.

The obvious risk is that XYZ finishes outside the Rs. Rs. 45-55 range at expiration. To mitigate this expiration risk, the trader could close the position before expiration to lock in profits or limit losses. They could also hedge by purchasing put options below Rs. 45.

What are the advantages of Long Put Butterfly?

The long put butterfly is an options trading strategy with defined risks and capped profits that involves being long a put vertical spread while short another put vertical at a middle strike. It offers ten advantages if utilized properly.

1.Defined and Capped Risk

The long put butterfly has defined maximum loss, which is the difference between the strike prices of the long put vertical spread minus the net credit received for the short vertical spread. The maximum loss occurs if the underlying asset closes below the lower long put strike or above the higher long put strike at expiration.

The maximum profit is capped at the initial net credit amount and is achieved if the underlying closes exactly at the short put strike at expiration.

The defined and capped risk allows traders to precisely calculate their potential loss ahead of time before entering the trade.

2. Benefits from Time Decay

With the short options positioned at the middle strike and the long options on either side, the long put butterfly benefits from time decay, eroding the value of the long options faster than the short options. The trader profits as the entire structure slowly declines in value.

The ideal scenario is for the underlying price to be at the short strike as expiration approaches, so all the options expire worthless except the profitable short puts.

3. Lower Margin Requirements

The initial margin requirement for a long put butterfly is often lower than just being long puts outright since it entails long options and short options. This frees up capital for other opportunities.

The lower margin and net credit entry also provide more leverage than just a long put vertical spread on its own.

4. Wide Range of Underlying Assets

Long-put butterflies are sometimes traded on stocks, ETFs, indexes, commodities, and other putable assets, giving them diversity.

They work well for assets expected to stagnate within a range through expiration as the trader profits from time decay.

5. Lower Breakeven

The breakeven points are wider apart than a simple long vertical spread, so the trader has more wiggle room for the underlying price at expiration.

6. Flexibility in Strikes

The wings of the long butterfly are sometimes adjusted wider or narrower based on forecast range expectations.

7. Credit Entry

The received credit upfront lowers breakeven points and cushions against losses.

8. No Upfront Debit

Long butterflies only require paying commissions, avoiding an upfront debit cost.

9. Defined Max Loss

The maximum loss is known and limited even if the underlying drops drastically.

10. Directionally Neutral

Profits from time decay rather than directional movement, making it market-neutral.

The limited risk, breakeven points, credit entry, and leverage attributes of the long-put butterfly provide several advantages for capitalizing on a neutral forecast.

What are the disadvantages of Long Put Butterfly?

Here is an overview of 10 potential disadvantages or risks when using a long-put butterfly options strategy.

1.Expiration Risk

The maximum profit is only achieved if the underlying is precisely at the short strike price at expiration. Any deviation above or below results in loss.

Traders have to be very confident in a narrow trading range through expiration. Time decay accelerates rapidly in the final weeks, increasing risk.

2. Minimum Price Move Risk

It is impossible for all the options to expire worthless for maximum profit if the gap between the strike prices is less than the minimum tick size.

The minimum price move risk skews the maximum profit zone downward.

3. Uncapped Loss Potential

Even if the maximum loss is specified, losses can occasionally surpass this limit if short options are prematurely assigned before expiry.

4. Low Probability of Profit

The underlying finishing right at the middle strike at expiration is relatively unlikely, so the probability of max profit is very low. Most outcomes result in loss.

5. Bid/Ask Spread Risk

Wide bid-ask spreads on the options leg significantly impact the net credit received and breakeven points.

6. Requires Close Monitoring

The position needs to be actively managed and closed before expiration rather than held until maturity like other strategies. This increases commission costs and effort.

7. Subject to Volatility Skew

Volatility skew on the put options impacts the net credit available. It benefits from a skew toward making trading rich.

8. Low Liquidity Risk

Illiquid options increase the trade entry cost and make managing the position more difficult.

9. Capped Profit Potential

Unlike a long call, the maximum gain is limited regardless of how far the underlying price moves favourably. The defined payout is modest for the risk taken.

The long-put butterfly has several disadvantages traders should understand before implementation, especially the expiration, probability, and liquidity risks that prevent profiting from the position.

Is Long Put Butterfly risky?

Yes, the long-put butterfly options strategy does carry a high degree of risk. At its core, the long-put butterfly has substantial risk due to its very narrow profit zone at expiration. The trader is extremely vulnerable to where the underlying asset’s price finishes as the options expire. The position only reaches maximum profit if the price settles precisely at the short strike price. Even finishing one strike higher or lower results in a loss. This makes it tremendously risky and difficult to consistently profit from.

Compounding the expiration risk is the accelerating time decay in the final month before the options expire. As expiration approaches, the value of the long-put butterfly erodes rapidly, nowhere near the idealized curves of theoretical options pricing models. This time decay pattern significantly raises the risk of ending up with a large loss in the final weeks before maturity if the trader fails to properly manage the position.

Another major risk is that the probability of finishing right at the short strike price is extremely low, so the anticipated maximum profit is rarely achieved. In most probable scenarios, the price settles above or below the short strike, resulting in loss. The trader takes high risks for a very low probability of the ideal outcome.

Furthermore, any early exercise of the short options before expiration creates additional risks. The trader sometimes experiences uncapped losses over the specified maximum loss at maturity if the short puts are issued before maturity. The early assignment risk is difficult to predict and manage.

Is Long Put Butterfly a good options strategy?

Despite some appealing attributes on the surface, the long put butterfly is generally not considered a good options trading strategy overall compared to alternatives.

While the long-put butterfly does cap maximum losses, the probability of reaching the maximum profit is extremely slim. The underlying asset price finishing precisely at the middle strike price at expiration is unlikely. More commonly, the trader will end up with a total loss as the position expires worthless. The limited risk comes at the cost of an extremely low probability of profit.

The strict dependence on the underlying price settling in a narrow range also makes long-put butterflies risky and inconsistent. Other strategies like credit or debit spreads have wider profit zones and greater flexibility to still profit if the forecast is slightly off. Butterflies offer less room for forecast error.

Compounding this is the accelerating time decay in the final month as expiration approaches. The long options erode faster than the short options, rapidly reducing the position’s value. This makes properly timing an exit incredibly difficult.

While the net credit entry sometimes appears attractive for lower capital requirements, alternative strategies like credit call spreads also provide credit. The modest credit collected rarely justifies the butterfly’s high cap on profits and narrow profit zone.

The perceived benefit of limited risk is counteracted by the early assignment risk on the short options. While maximum loss is fixed at expiration, early exercise generates uncapped losses exceeding expectations.

Finally, the long-put butterfly is highly vulnerable to low liquidity in the options. Wide bid-ask spreads will negatively impact entry and exit costs.

Is Long Put Butterfly hard to use?

The long put butterfly is generally considered a more challenging options trading strategy that beginner traders will likely find difficult to use successfully. There are three key reasons why the long-put butterfly strategy tends to be hard for beginners.

Firstly, the strategy has an extremely narrow profit zone that requires the underlying asset to finish precisely at the short strike price at expiration for maximum profit. Even finishing one strike higher or lower results in a loss. Hitting this precise target is extremely difficult for novice traders.

Secondly, managing the acceleration of time decay in the final weeks before expiration requires experience that beginners typically lack. The nuances around expiration dynamics and theta cause beginners to struggle with closing the trade at the optimal time.

Additionally, the odds strongly favour the underlying settling outside the tight profit range, resulting in full loss. Many beginners are attracted to the limited risk but underestimate the low statistical probability of achieving that maximum profit. This results in consistent losses in practice.

Other factors like wide bid-ask spreads, managing position Greeks, thin liquidity in the options, and early assignment risks create further challenges. Active management is required, unlike simple buy-and-hold approaches.

Is Long Put Butterfly a bullish strategy?

No, the long put butterfly is generally considered a neutral options trading strategy, not a bullish one.

The long put butterfly involves simultaneously buying a put vertical spread while selling another put vertical spread at a middle strike price. This market-neutral construct profits from time decay as the options lose value over time rather than needing bullish directional movement.

The ideal scenario for a long put butterfly is for the underlying asset price to be at the short strike as expiration approaches. The trader does not care if the price is trending up or down before that. They simply want it to be at the short strike at maturity so the surrounding long puts expire worthless while the short puts finish in-the-money.

The trader does not gain an advantage whether the price is below the lower strike put or above the higher strike put heading into expiration. They only care about where it settles on the actual expiration date, not the preceding trend. As a result, the strategy is indifferent to bullish or bearish price action in the underlying asset.

Additionally, the long put butterfly achieves max profit at the short strike target regardless of whether the underlying asset rallied aggressively into expiration or declined steadily into it. The previous market direction is irrelevant to capturing the maximum gain.

It is worth noting the trader prefers relatively low volatility and a stagnant trading range environment. However, this is different from a bullish bias since low volatility benefits both calls and puts in the structure. The trader wins by the options expiring worthless, not rising put values.

Is Long Put Butterfly the most effective Butterfly spread strategy?

The long-put butterfly is not the most effective butterfly spread strategy overall. Here is an overview comparing the long-put butterfly to alternatives and explaining its limitations in effectiveness.

Compared to alternative butterfly strategies, the long-put butterfly is generally one of the least efficient and effective approaches. Its extremely narrow profit zone and exposure to time decay make it unlikely to produce consistent gains for most traders.

An alternative like the long call butterfly will have a higher probability of profit. A debit spread butterfly offers greater leverage on directional moves. An iron butterfly has wider wings and profit potential. Even a short-put butterfly collects more premium with lower cost of entry.

The long-put butterfly’s maximum profit is capped at the initial credit received regardless of how far past the short strike the underlying moves. Other approaches offer uncapped returns for large directional moves.

While the long-put butterfly benefits from time decay, the acceleration of theta in the final month also creates a substantial risk that the position gets crushed right before expiration. Properly timing the exit is extremely difficult.

Advanced traders sometimes still use long-put butterflies selectively when their forecast precisely matches the required price action before expiration. However, for most traders, alternatives like call or iron butterflies will be easier to manage and have greater effectiveness at generating consistent profits across market conditions. The long put butterfly has a niche application but lacks the efficiency and versatility to be considered a top butterfly spread strategy.

What is the difference between Long Put Butterfly and Short Put Butterfly?

The long put butterfly involves being long a put credit spread while also being short a put debit spread at a middle strike. In contrast, the short put butterfly is short the put credit spread and long the put debit spread instead. This positioning flip results in very different risk-reward profiles between the two strategies.

The long put butterfly has a fixed maximum loss defined as the difference between the strike prices minus the net credit received. The max loss occurs if the underlying finishes below the lower long put strike or above, the higher long put strike at expiration. Whereas the short put butterfly has an undefined maximum loss beyond the long put strike prices since it collects a net debit.

This means the short-put butterfly faces an uncapped downside if the underlying drops sharply. The long-term butterfly’s loss is limited. However, the short-put butterfly sometimes achieves much higher potential profits if the underlying rallies outside the wings. The long butterfly’s profit is capped at the modest initial credit amount.

The Greeks also differ substantially. The long-put butterfly benefits from declining option values across all legs as time decay accelerates into expiration. The short-put butterfly loses money daily from time decay and needs directional movement to profit.

Furthermore, the breakeven points are different. The long put butterfly breakevens are the lower and higher strikes minus the net credit received. But the short put butterfly breakevens are the lower and higher strikes plus the net debit paid. Wider distance for the short butterfly.

What is the difference between Long Put Butterfly and Long Call Butterfly?

The long put butterfly involves being long a put credit spread while also being short a put debit spread at a middle strike price. In contrast, the long call butterfly is long a call credit spread and short a call debit spread. The change from put options to call options significantly alters the fundamentals of the strategy.

The long put butterfly achieves max profit if the underlying is exactly at the short put strike at expiration. All options expire worthless except the profitable short puts. The long call butterfly wants the underlying to be at the short call strike instead. Here, the profitable options are the short calls.

While both strategies rely on time decay across the structure, the long put butterfly benefits from declining put values, while the long call butterfly profits from declining call values instead. They have similar market-neutral stances but with puts or calls determining the effect.

The maximum loss on the long put butterfly occurs if the stock finishes below the lower put strike or above the higher put strike. For the long call butterfly, maximum loss happens if the stock is below the lower call strike or above the higher call strike. The boundaries flip.

The long-put butterfly performs best with low implied volatility to accelerate time decay. But the long call butterfly benefits more from rising volatility to offset time erosion. Different vega exposures.

Finally, the long-put butterfly trader is bullish on volatility while bearish on stock price directionality. But the long call butterfly trader is bearish on volatility and neutral on direction. Opposing volatility and directional outlooks.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 28")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 29")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 30")

: Overview, 10 Types of Indicators, Settings for Different Markets 32")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 34")

: How We Used This 70/30 Indicator in 6 High Win-rate Strategies 38")

No Comments Yet.