Short put condor involves selling a put spread and buying another put spread with wider strikes. Short put condor generates maximum profit at expiration if the underlying price settles between the middle strikes.

The strategy combines elements of bear and bull put spreads, aiming to capitalize on high volatility scenarios. Limited to the difference between adjacent strike prices minus the net premium received if the asset’s price remains between the middle strike prices at expiration, the strategy incurs a maximum loss.

Short put condors are particularly effective when traders anticipate significant market movements due to events like earnings reports or economic announcements. The defined risk and reward parameters make it a controlled approach to trading in volatile markets.

The short put condor is a strategic choice for traders expecting significant price swings, offering a balanced approach with limited risk and reward. Its effectiveness hinges on accurate market forecasts and disciplined trade management.

What is a Short Put Condor?

A short put condor is a four-legged neutral options strategy that profits from range-bound price action. Short put condor combines two put credit spreads with different strike prices, creating a position that benefits from time decay.

The strategy involves buying one put at a higher strike, selling two puts at middle strikes, and buying another put at a lower strike. Think of Nifty trading at 19300: Buy 19500 put, sell 19400 put, sell 19200 put, buy 19100 put.

The position requires careful monitoring of delta exposure. Successful traders maintain position sizes under 3% of portfolio value and close trades at 50% of maximum profit potential.

How Does a Short Put Condor Work?

Short put condor works by combining two credit spreads to create a neutral position. Short put condor works through four legs where traders buy one ITM put, sell one slightly ITM put, sell one slightly OTM put, and buy one OTM put.

The structure includes buying one in-the-money (ITM) put with the highest strike price, selling one slightly ITM put, selling another slightly out-of-the-money (OTM) put, and finally buying one further OTM put with the lowest strike price.

This combination results in two credit spreads — one on the higher end of the strike range and one on the lower end. The put options are selected such that the two sold options are closer to the current market price, and the two purchased options are further apart, forming a “condor” shape when plotted on a risk-reward graph.

Why Use a Short Put Condor Strategy?

A short put condor strategy is used to profit from a neutral market with limited risk and defined reward. It is ideal when a trader expects the underlying asset to stay within a tight price range until expiration. The setup involves collecting premium income while limiting downside exposure through protective legs.

This strategy takes advantage of time decay, making it suitable for range-bound environments. By selling two puts closer to the current price and buying two further out, traders create a position where the maximum reward is earned if the asset stays between the middle strikes.

The limited loss potential is another reason traders choose this strategy. Compared to undefined-risk strategies like short strangles, the short put condor offers peace of mind through clearly defined risk.

Short Straddle, Strangle strategies are especially popular during periods of low volatility, when price movement is expected to be subdued. Traders use them to earn consistent returns without needing directional accuracy.

When to Use a Short Put Condor?

A short put condor is best used when the market is expected to trade sideways with low volatility. This strategy works optimally when the underlying stock is consolidating within a range. Traders enter this position expecting minimal movement until the option expires.

Such scenarios typically occur after a strong trend when the asset begins to pause or form a base. Technical indicators like Bollinger Bands or Average True Range (ATR) help identify low volatility environments suitable for condor setups.

It is also practical before earnings releases or economic events if the trader expects no major surprises. During these windows, implied volatility may drop after the event, helping the strategy profit further.

Entering around 45 days to expiration allows time decay to accelerate without carrying risk for too long. This timing balances theta gains and market exposure effectively.

How Option Greeks Affects Short Put Condor?

Option Greeks effects the profitability and risk of a short put condor. Theta, Vega, and Delta are the primary Greeks influencing this strategy’s outcome. Each Greek highlights a specific sensitivity that affects trade performance.

Theta, or time decay, works in favor of this strategy. Since the position earns a net credit, the value of the sold options decreases with time, adding to profitability if the asset stays within range. High theta is desirable when holding condors.

Vega, the sensitivity to volatility, works against the trade when implied volatility increases. Rising volatility increases the value of all options in the condor, especially the long legs, which results in unrealized losses. A drop in volatility benefits the trader as premiums fall.

Delta exposure is low in condors but still matters. The goal is to remain delta-neutral, meaning the trade doesn’t benefit or suffer much from small price moves. Adjusting strikes close to the current price can balance delta for a more stable setup.

How to Trade using Short Put Condor?

To trade using a Short Put Condor, you construct a four-leg credit spread designed to profit if the underlying, such as the Nifty index, expires outside a defined price range. In this example,

selling one in-the-money (ITM) put at 24300 for ₹215, buying one at-the-money (ATM) put at 24200 for ₹145, buying one close-to-the-money (CTM) put at 24150 for ₹115, and selling one out-of-the-money (OTM) put at 24050 for ₹75. With a lot size of 75, your total premium received is ₹290, and total premium paid is ₹260, resulting in a net credit of ₹30 per lot, or ₹2,250 in total.

The above graph outlines the strike prices and the critical breakeven points. It shows that for profits, Nifty must expire above 24300 or below 24050, outside the blue lines indicated on the chart. As expiry approaches (in this case, just three days away), the range becomes crucial—if Nifty closes outside this range, you retain the full net premium.

The strategy’s structure means you profit if the market moves sharply in either direction, but risk a defined loss if it stays within a narrow band.

Your maximum profit of ₹2,250 occurs if Nifty expires above 24300 or below 24050, as all puts will either expire worthless or offset each other, leaving you with the initial premium. The maximum loss is capped at ₹5,250, happening if Nifty expires between 24150 and 24200, where both short puts are in-the-money and losses on the long puts dominate. The breakeven points are calculated as 24080 (lower) and 24270 (upper).

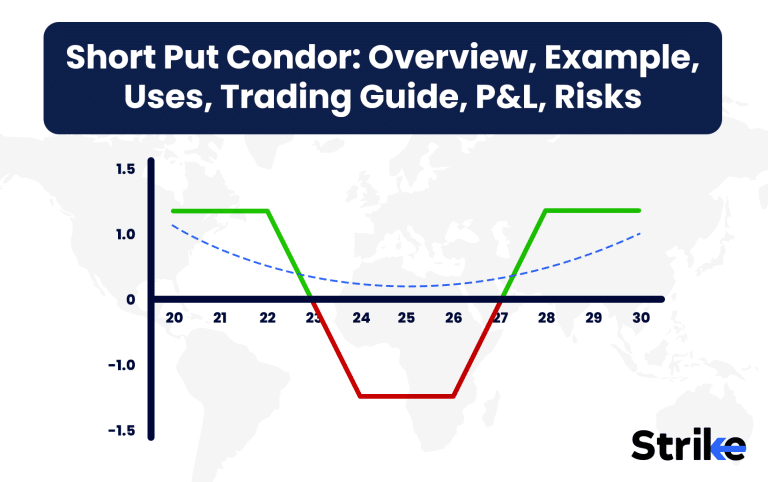

The above is a payoff diagram that clearly visualizes the profit and loss profile of the Short Put Condor. The green areas illustrate where you profit, while the brown area between the inner strikes shows the maximum loss. This strategy is ideal when you expect volatility or a strong move in either direction, while keeping your risk limited and known upfront. Key elements such as the strike price and expiration of options play a crucial role in determining the potential outcomes and risk-reward of this strategy.

What are the Maximum Profit & Loss, Breakeven on a Short Put Condor?

The maximum profit in a short put condor equals the net premium received, while the maximum loss is the difference between adjacent strikes minus the premium. Breakeven points occur when the underlying asset reaches either of the middle strikes plus or minus the net credit.

In case the underlying price ends up between the two middle strikes at expiration, all options expire worthless. In this scenario, the trader retains the entire premium collected at trade entry. This is the ideal outcome for the strategy.

The maximum loss is realized if the asset closes beyond either of the outer bought strikes. The loss is limited because the long puts act as insurance against sharp movements. Subtracting the premium from the spread width gives the total loss.

Knowing breakeven points helps in deciding entry and managing expectations. Profit zones are clearly defined, making this a controlled-risk strategy suited for sideways price action.

How to Adjust a Short Put condor?

Adjusting a short put condor involves managing position risk by shifting strikes, closing legs, or converting the setup. Adjustments become necessary when the underlying starts moving beyond expected limits. The goal is to reduce losses or recenter the trade.

One approach is to roll the entire position to a new expiry or different strikes if there’s still a neutral outlook. Rolling extends the timeline for profits while maintaining defined risk. This helps when the setup is still valid but needs more time.

Suppose the price breaches the lower end – consider removing the losing leg and converting the trade to a vertical spread. Also, open a new condor closer to the price for better alignment. This shift allows time decay to work in your favor again.

Active monitoring is key to managing short condors. Adjusting early helps avoid large losses and preserves capital for future trades. Having a pre-defined adjustment plan improves decision-making under pressure.

What are the Risks of Short Put Condor?

The main risk in a short put condor is loss of capital if the underlying moves sharply beyond the outer strikes. Although losses are capped, they can still be significant relative to the potential reward. Understanding these risks is essential before entering.

Another risk is volatility expansion. The value of all options increases if implied volatility rises sharply after trade entry,. This leads to unrealized losses and affects the ability to close the position profitably. Hence, entering in low IV environments is important.

Liquidity is also a concern. Illiquid options increase the bid-ask spread and reduce the ease of entering or exiting at fair prices. Choosing underlyings with high open interest and narrow spreads helps reduce this issue.

Psychological pressure cause early exits. Traders panic and close positions unnecessarily if the price moves near breakeven point,. Confidence in the setup and disciplined risk management are essential to stay consistent with this strategy.

Is Short Put Condor Strategy Profitable?

Yes, the short put condor strategy is profitable when the underlying stays within a defined price range and volatility contracts. It works well in stable markets where price movement is limited and predictable. The strategy profits by collecting premium upfront and allowing time decay to erode the value of the sold options.

The profitability of the setup depends on careful strike selection, proper timing, and favorable volatility conditions. Traders must identify underlying assets that are consolidating or trading sideways. In such cases, all four options in the condor can expire worthless, allowing the trader to keep the net credit received at the outset.

Time decay plays a significant role in driving profits. Since the position is net credit, every day that passes without the asset breaching key levels increases potential gains. Moreover, if implied volatility drops after the trade is entered, option prices fall, benefiting the trader further.

Is Short Put Condor Bullish or Bearish?

The short put condor is a neutral strategy, not bullish or bearish. It is specifically designed for traders who expect the underlying asset to remain within a tight range. Unlike directional trades, this setup doesn’t rely on price moving up or down.

This neutrality makes it different from strategies like bull puts or bear calls that require directional bias. In a short put condor, maximum profit occurs only if the underlying finishes between the two middle strike prices. The strategy loses value if the price moves significantly in either direction.

The ideal setup is when the trader identifies a strong support and resistance zone. This gives a well-defined range where the asset is likely to consolidate. The condor is then built around this zone, ensuring the price remains between the two short strikes at expiration.

What’s The Difference Between a Short Put Condor & Long Put Condor?

The difference between a short put condor and a long put condor lies in their construction and market outlook.

| Feature | Short Put Condor | Long Put Condor |

| Position | Sell 2 middle puts, buy outer puts | Buy 2 middle puts, sell outer puts |

| Credit/Debit | Net credit received | Net debit paid |

| Max Profit | Limited to credit received | Difference between middle strikes minus debit |

| Profit Zone | Between middle strikes | Outside middle strikes |

| Market View | Range-bound | Expects large move |

| Time Decay | Benefits position | Hurts position |

| Volatility | Benefits from decrease | Benefits from increase |

What are Alternatives to Short Put Condor Strategy?

Alternatives to the short put condor strategy include Iron Condor, Short Put Spread, Short Strangle, and Calendar Spread, each suited to different market views and risk profiles. These alternatives give traders flexibility to adapt based on volatility expectations, directional bias, and risk tolerance.

An Iron Condor is the closest relative. It combines a short put condor with a short call condor, creating a non-directional setup with two credit spreads. It profits when the underlying stays within a broader range, making it ideal for ultra-low volatility environments. Since it uses both puts and calls, it has more exposure but also a wider profit zone.

The Short Put Spread is more directional in nature. It involves selling a put and buying a lower-strike put to limit risk. This strategy is best when the trader has a mildly bullish view and expects the stock to stay above a certain level. It has lower margin requirements and a straightforward risk-reward structure.

A Short Strangle involves selling an out-of-the-money put and call. It offers higher potential profits than a condor but comes with unlimited risk on the upside and significant risk on the downside. It suits experienced traders willing to monitor trades closely and exit quickly when price moves aggressively.

The Calendar Spread, unlike the others, focuses on volatility and time decay differences between short- and long-dated options. It involves selling a short-term option and buying a longer-term option at the same strike. It profits from time decay and changes in implied volatility. This strategy is useful during low-movement phases with upcoming catalysts like earnings.

Each alternative has trade-offs. The choice depends on the trader’s market view, comfort with risk, and strategy preference.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 24")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 25")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 26")

: Overview, 10 Types of Indicators, Settings for Different Markets 27")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 30")

No Comments Yet.