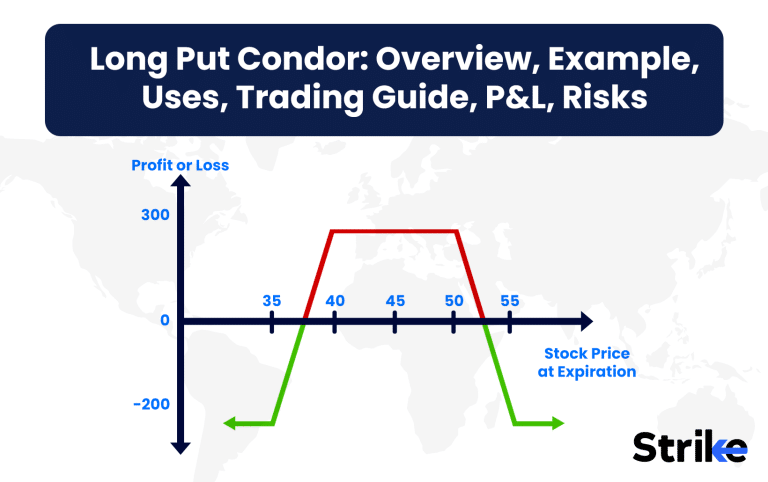

Long Put Condor is a neutral options strategy that involves simultaneously buying one put with a higher strike price, selling two puts with middle strike prices, and buying another put with a lower strike price, all with the same expiration date. Long Put Condor profits from low volatility and works best in sideways markets with minimal price movement.

Indian traders execute this strategy frequently on Nifty and Bank Nifty index options. The strategy emerged in the 1990s alongside other multi-leg options combinations. Over 12% of Indian options traders use condor strategies, according to a 2023 NSE study.

Traders prefer this strategy during quarterly earnings seasons and major economic events. The maximum profit occurs between the two middle strike prices, while maximum loss happens at the outer strikes. Successful execution requires precise entry points and proper strike price selection. Indian brokers report an average success rate of 65% for long put condors in range-bound markets.

Professional traders combine long put condors with other strategies to create portfolio-wide hedging positions.

What is a Long Put Condor?

The Long Put Condor is a neutral, four-legged options strategy constructed by buying one put at a higher strike price, selling two puts at middle strike prices, and buying another put at a lower strike price, all with identical expiration dates. The Long Put Condor requires equal spacing between all strike prices and results in a net debit to enter the position.

Traders establish this strategy by:

1. Buying 1 OTM put option

2. Selling 2 ATM put options

3. Buying 1 ITM put option

The strategy excels in range-bound markets like the periods between Nifty’s major support and resistance levels. Indian traders often implement this on index options during low volatility phases.

NSE statistics show increased adoption of condor strategies among retail traders, particularly in Bank Nifty weekly options. The strategy suits traders expecting minimal price movement around a specific strike price and declining implied volatility. Professional traders use it extensively during sideways market conditions, especially in large-cap stocks with high options liquidity.

How Does a Long Put Condor Work?

A long put condor works by combining four put options at different strike prices to create a neutral position that profits from sideways price movement. The long put condor strategy executes through buying one ITM put at the highest strike, selling one ITM put at a slightly lower strike, selling another OTM put at an even lower strike, and buying one OTM put at the lowest strike.

Consider this example on Nifty.

- Buy 19500 Put at ₹500

- Sell 19300 Put at ₹350

- Sell 19100 Put at ₹200

- Buy 18900 Put at ₹100

The net debit equals ₹50 (500 – 350 – 200 + 100). Maximum profit occurs with Nifty between 19300 and 19100 at expiration.

The position creates a profit zone between the two middle strikes (19300-19100). The strategy limits both potential losses and gains. Maximum loss materializes at either extreme – above 19500 or below 18900.

Traders implement this strategy during quarterly results season or before major economic events. The equal distance between strikes (200 points in this example) maintains strategy balance. Professional traders adjust position size based on Nifty’s Average True Range (ATR).

What is an Example of Long Put Condor?

An example of a long put condor demonstrates with TCS stock trading at ₹3,900 in April 2025, using puts expiring in 30 days.

Buy 1 TCS 4000 Put at ₹150

Sell 1 TCS 3950 Put at ₹120

Sell 1 TCS 3850 Put at ₹80

Buy 1 TCS 3800 Put at ₹60

Net Debit = ₹10 (150 – 120 – 80 + 60)

Maximum Profit = ₹40 (50 – 10 debit)

Maximum Loss = ₹10 (initial debit)

Break-even Points: ₹3,910 and ₹3,890

The strategy profits maximally with TCS trading between ₹3,950 and ₹3,850 at expiration. The position loses money above ₹4,000 or below ₹3,800.

The real-world entry points match key technical levels:

– ₹4,000: Major resistance from February 2025 high

– ₹3,950: 20-day moving average

– ₹3,850: 50-day moving average

– ₹3,800: Strong support from March 2025 low

The equal ₹50 strike spacing aligns with TCS‘s typical weekly price range. NSE options data showed high liquidity at these strike prices, enabling efficient entry and exit. The position benefits from TCS’s historically low volatility during post-earnings periods.

Why Use a Long Put Condor Strategy?

Traders use a Long Put Condor strategy to profit from range-bound markets with low directional risk and defined loss. It is a non-directional setup designed to benefit from time decay and a drop in implied volatility.

The strategy appeals to traders who want to limit their risk while still having a decent chance of making money. It involves buying and selling four puts at different strike prices but within the same expiration.

The Long Put Condor is useful when the trader expects the underlying stock to remain in a tight range. Instead of trying to predict whether the stock will rise or fall, the trader focuses on where it is unlikely to go.

This setup offers a stable risk-reward profile. The maximum loss is fixed and occurs only if the stock moves far outside the outer strike prices.

Another reason to use this strategy is to take advantage of high implied volatility. Entering the trade when volatility is elevated and exiting when it drops results in gains, even if the stock does not move.

It works best when there is no strong trend, and the price action is stuck between support and resistance. This kind of market condition allows the position to gain value slowly as time passes.

Since two middle strike puts are sold, the net premium collected reduces the cost of the trade. This makes the Long Put Condor more affordable than buying a naked put or constructing a wider spread.

Traders often use this Option trading Strategy to earn income in sideways markets. It rewards patience and discipline, rather than bold directional bets.

It is also a good fit for traders who want minimal maintenance. Once the position is set, there is usually no need for constant adjustment unless the price nears the breakeven points.

When to Use a Long Put Condor?

Long put condor trades excel in range-bound markets with clear support and resistance levels. The strategy proves most effective during periods of high implied volatility expected to decrease over time.

Market conditions favoring this strategy include pre-budget consolidation phases, post-quarterly results periods, and during major economic events. The strategy thrives in stocks like HDFC Bank, which traded between ₹1,550-1,650 for eight weeks in early 2025.

Technical analysis supports entry timing through identification of strong support-resistance zones, declining volume trends, and contracting Bollinger Bands. Traders execute these positions after significant price movements have exhausted, indicating a likely period of consolidation.

The ideal setup emerges in highly liquid options with tight bid-ask spreads. Nifty and Bank Nifty options present prime opportunities during monthly expiry cycles. The strategy capitalizes on time decay acceleration in the last 30-45 days of option life.

Indian institutional traders frequently deploy this strategy in index options before major events like RBI policy announcements or GDP data releases. The position benefits from reduced market volatility and sideways price action.

How Option Greeks Affects Long Put Condor?

Option greeks affect long put condor positions through their combined impact on each leg of the strategy. Delta remains neutral at initiation, making the position relatively direction-independent. The strategy maintains minimal delta exposure as long as the underlying stays between the middle strikes.

Theta works positively for the position, with time decay benefiting the two short puts more than the long puts. Consider a Nifty long put condor with 30 days to expiration – the position generates approximately ₹150-200 daily through time decay in stable market conditions.

Vega impacts the strategy negatively during volatility spikes. The position benefits from declining implied volatility, common in range-bound markets. The 2025 pre-budget period saw many successful condor trades as VIX declined from 18 to 14.

Gamma exposure remains minimal near the center of the position but increases as the underlying approaches either short strike. TCS condor traders in April 2025 experienced this effect as the stock approached the upper strike of ₹3,950.

Rho plays a minor role as part of the Option Greeks, though interest rate changes slightly affect put values. The RBI’s rate decisions in 2025 caused minimal impact on existing condor positions.

How to Trade Using Long Put Condor?

To trade with a long put condor, you combine four put options at different strikes to benefit from a range-bound market, where you expect the underlying to remain between two levels by expiry.

The position is built by buying one in-the-money (ITM) put at the highest strike, selling one put at a slightly lower strike (at-the-money or near ITM), selling another put at an even lower strike (close-to-money or OTM), and finally buying one more out-of-the-money (OTM) put at the lowest strike.

For example, on Nifty, this structure could include buying the 24300 PE at ₹280, selling the 24250 PE at ₹250, selling the 24050 PE at ₹165, and buying the 24000 PE at ₹143, with a lot size of 75.

This setup results in a net debit trade, as the total premium paid is slightly higher than the total premium received. In the given example, the net debit is ₹8 per spread, totalling ₹600 per lot. This amount represents your maximum possible loss, which will occur if Nifty expires either above 24300 or below 24000, meaning all the options except the far ITM or OTM legs expire worthless or lead to a fixed loss.

The maximum profit is achieved if Nifty expires between the two short put strikes—between 24050 and 24250 in this case. The profit is calculated as the width of adjacent strikes minus the net debit, resulting in a maximum gain of ₹3,150 per lot.

Breakeven points are also well defined: the lower breakeven is the lower short put strike minus the net debit (24050 – 8 = 24042), and the upper breakeven is the higher short put strike plus the net debit (24250 + 8 = 24258).

As long as Nifty closes within these breakeven levels at expiry, the strategy yields a profit. The Long Put Condor is ideal for traders anticipating a sharp drop in volatility and a range-bound expiry, while keeping risk limited and profit potential defined.

What is the Maximum Profit & Loss on a Long Put Condor?

The maximum profit in a long put condor equals the difference between adjacent strike prices minus the net debit paid. The maximum loss limits to the initial net debit paid for establishing the position. This risk-reward profile attracts Indian traders seeking defined risk strategies.

Consider this example using Nifty options.

Buy 1 19500 Put at ₹450

Sell 1 19400 Put at ₹400

Sell 1 19300 Put at ₹350

Buy 1 19200 Put at ₹300

Net debit = ₹450 – ₹400 – ₹350 + ₹300 = ₹0

Strike price difference = ₹100

Maximum profit = ₹100 – ₹0 = ₹100

Maximum loss = Initial debit = ₹0

The position reaches maximum profit with Nifty between 19400 and 19300 at expiration. The strategy loses money beyond the outer strikes of 19500 and 19200. Break-even points occur at 19450 and 19250.

Professional traders target a profit-to-loss ratio of 2:1 or better. Historical NSE data shows successful trades averaging 40-60% of maximum profit potential. The strategy performs optimally in range-bound markets with declining volatility.

Traders frequently execute this strategy on index options during major events. Bank Nifty traders achieved maximum profits during the February 2025 monetary policy announcement as the index stayed within the expected range.

How to Adjust a Long Put Condor

A long put condor is adjusted based on underlying price movement, time decay, and volatility changes. The position requires active management once the underlying moves close to or beyond the short strike prices.

Rolling the position emerges as the primary adjustment technique. Consider a Nifty long put condor with strikes at 19500/19400/19300/19200. The position needs adjustment as Nifty approaches 19400. Traders roll the entire structure up by 100 points, maintaining the same width between strikes.

Early exit serves as another adjustment method. Professional traders close the position at 50% of maximum profit rather than risking giveback. The strategy performed well during TCS’s range-bound period in March 2025, where traders exited at ₹2,500 profit per lot.

Delta-adjustment helps maintain neutrality. Adding or removing stock positions keeps the overall delta near zero. Large institutions trading Bank Nifty condors adjust delta exposure by trading futures contracts.

Volatility-based adjustments involve modifying strike widths. During the 2025 budget session, traders widened their strikes as market volatility increased. The standard 100-point width expanded to 150 points to accommodate larger price swings.

Time-based adjustments include rolling to the next expiry series. Successful traders avoid holding positions into the last two weeks of expiry. A popular approach involves closing current month positions and establishing new ones 45 days out.

What are the Risks of Long Put Condor?

The risks of long put condor include significant exposure to price movement beyond the outer strikes, volatility spikes, and insufficient premium collection. The strategy suffers during strong directional moves, as experienced during the March 2025 market correction where Nifty moved 800 points in five sessions.

Limited profit potential creates opportunity cost in trending markets. A Reliance Industries condor position in April 2025 earned only ₹150 per lot while the stock rallied 12%. Traders missed substantial directional gains by staying neutral.

Early assignment risk exists on the short put options. Indian traders faced this challenge during corporate actions, like HDFC Bank’s special dividend announcement in 2025. The assignment triggered unwanted position imbalances.

Liquidity risk impacts position management. The strategy requires four different option strikes. Less liquid stocks show wide bid-ask spreads, increasing execution costs. Even liquid names like TCS witnessed reduced option liquidity during major market events.

Transaction costs eat into potential profits. Each leg incurs brokerage, exchange fees, and bid-ask spreads. A typical four-leg position costs approximately ₹400 in various charges on NSE.

Time decay works against the position in rapid market moves. Traders lost money in Bank Nifty condors during the February 2025 RBI policy announcement as prices moved beyond the profit zone before time decay materialized.

The strategy also faces gamma risk near expiration. Delta changes accelerate as the underlying approaches short strikes, requiring more frequent adjustments and increasing management costs.

Is Long Put Condor Strategy Profitable?

Yes, the Long Put Condor strategy is profitable in range-bound markets with high implied volatility. It is a limited risk, limited reward options strategy that works well when the underlying asset is expected to stay within a certain price range until expiration.

The Long Put Condor involves buying one higher strike put, selling two middle strike puts, and buying one lower strike put. All options belong to the same expiration cycle, and the strikes are equidistant. The result is a payoff that resembles a wide valley, with maximum profit achieved when the stock closes near the middle strike at expiry.

This strategy is best suited for traders who expect minimal price movement. It generates profit from time decay and volatility contraction. If the underlying asset remains within the short strikes’ range, all the options lose value over time, especially the short puts. This decay benefits the trader, allowing them to close the position at a net profit.

The risk is limited to the net debit paid to enter the trade. If the stock moves sharply up or down, the losses are also contained. This makes the Long Put Condor safer than naked options or directional strategies. It offers peace of mind to traders who prefer to define their risk upfront.

Is Long Put Condor Bullish or Bearish?

The Long Put Condor is a neutral strategy, not bullish or bearish. It is designed for situations where a trader expects little or no movement in the underlying asset.

The strategy makes the most money when the asset remains close to the strike price of the short puts. This neutrality means that traders are not betting on direction but on stability. It is the opposite of directional strategies like Long Calls or Long Puts, which need price movement to profit.

That makes it ideal for stocks or indices trading in a sideways pattern. It gives the trader a defined zone of comfort, where as long as the price doesn’t escape the boundary, the position earns a gain. This removes the need to predict direction, focusing instead on price containment.

Some traders use this strategy ahead of earnings, central bank announcements, or other events where volatility is high, but the price is not expected to move much. As long as the event passes without a big surprise, the stock remains in a tight range, and the Condor works as planned.

What are Alternatives to the Long Put Condor Strategy?

The alternatives to long put condor strategy include several range-bound options strategies commonly used in Indian markets.

| Strategy | Risk | Max Profit | Margin Required | Best Market Condition |

| Iron Condor | Limited | Strike Width – Credit | High | Range-bound |

| Butterfly Spread | Limited | Strike Width – Debit | Medium | Low Volatility |

| Calendar Spread | Limited | Variable | Low | Sideways/Falling Vol |

| Short Strangle | Unlimited | Net Credit | Very High | Range-bound |

The iron condor proves popular in index options during pre-budget periods. Butterfly spreads excel in low volatility environments like post-earnings periods. Calendar spreads work effectively during quarterly expiries. Short strangles attract experienced traders during extended consolidation phases.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 32")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 33")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 34")

: Overview, 10 Types of Indicators, Settings for Different Markets 36")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 38")

No Comments Yet.