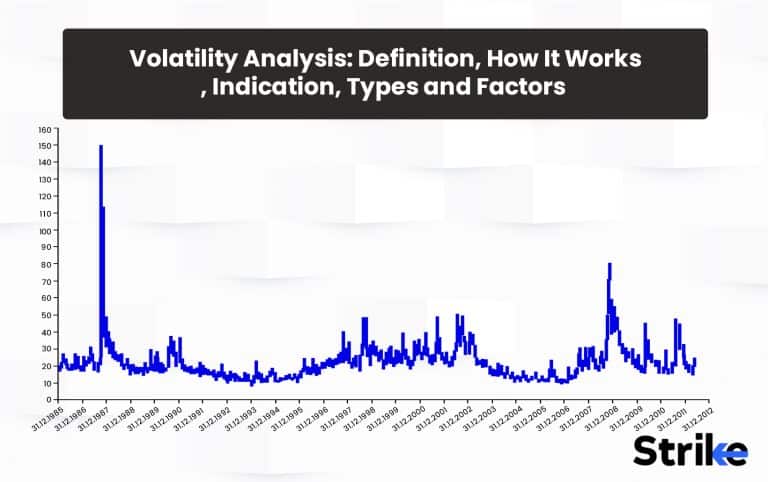

Volatility analysis involves studying the changes in the price of a security over time. Volatility analysis measures how much and how quickly the price fluctuates.

High volatility means large price swings, while low volatility means the price is relatively stable.

Volatility analysis works by looking at historical price data over a period of time. Statistical techniques like standard deviation are used to quantify volatility. The more prices deviate from the average, the higher the volatility. Charts like candlesticks also visually show volatility.

High volatility indicates greater risk but also greater profit potential. Low volatility indicates lower risk and steadier returns. Traders use volatility to identify trading opportunities and manage risk. Strategies like straddles and strangles benefit from high volatility.

Volatility studies can be extremely useful for short term trading and intraday derivatives trading. Scalpers and day traders use volatility to trade in options trading as option buyers and option writers, both expect volatility to be high for better returns over time.

Major types of volatility analysis include historical volatility, implied volatility, and statistical volatility. Historical volatility looks back at actual price changes. Implied volatility uses option prices to estimate future volatility. Statistical volatility uses statistical models to forecast volatility.

Key factors influencing stock volatility include economic events, earnings reports, industry announcements, interest rates, political events, and investor sentiment. Stocks of smaller companies also tend to have higher volatility. Understanding what drives volatility helps traders position themselves.

What is Volatility Analysis?

Volatility analysis refers to the study and measurement of fluctuations in the price of a security over a specified period of time. Volatility analysis is a mathematical analysis of the variation in the price of a financial instrument over time.

Volatility analysis is an important concept in the stock market because it helps investors quantify and analyze risk. It provides a statistical measure of the magnitude and speed of price movements. Volatility is a major consideration when evaluating an investment, as it directly impacts the potential profitability and risk associated with a security.

Volatility analysis, specifically, examines how much and how quickly security prices move.

High volatility indicates large price swings and more pronounced ups and downs.

Low volatility indicates more modest price changes and relative stability. The more volatile a security is, the wider the price range between its high and low trading prices over the measured timeframe. Volatility analysis is carried out in the following ways:

- Historical volatility measures the actual volatility observed in past price activity over a specified lookback period. It quantifies the volatility already experienced by the security based on a statistical analysis of historical prices.

- Implied volatility uses the current market prices of a security’s options to estimate what future volatility could be. It looks at options pricing to determine the market’s expectation of volatility going forward.

- Statistical volatility uses statistical models and forecasts to predict the range of potential future price movements. This technique relies on quantitative methods versus past price or option data.

How Does Volatility Analysis Work?

Volatility analysis involves studying and measuring the fluctuations in the price of a stock over a particular time period. It aims to quantify how much and how quickly security prices move. The main goal of volatility analysis is to measure the amount of risk and potential reward associated with a security. Let us look at the main methods used to conduct volatility analysis.

Historical Volatility

This approach measures the actual volatility observed in past price movements over a specified lookback period, such as 20 days or 90 days. Historical volatility is calculated by analyzing the historical closing prices of a stock over the selected timeframe.

The most common way to quantify historical volatility is by using the standard deviation. The Standard deviation measures how dispersed the price data points are from the statistical mean, or average price. A higher standard deviation indicates wider price swings and higher volatility. In the chart uploaded below, one can see, banknifty script is attached with a historic volatility indicator with default settings. In the first box, one can observe the candles are huge, meaning large price fluctuations taking place in higher volatility periods whereas the second box represent price fluctuation in lower volatility periods. Candles are small meaning lesser price fluctuations on a daily basis.

In addition to standard deviation, historical volatility can also be represented by metrics like variance, beta, R-squared, and more. Historical volatility provides insights into how volatile the stock has been in the recent past.

Implied Volatility

Implied volatility is calculated from the current market prices of a stock’s options. It uses options pricing models to analyze the market’s expectation of future volatility. Implied volatility looks forward, while historical volatility looks backward.

Implied volatility uses the prices of calls and put options on a stock to estimate the potential movement of the underlying stock going forward. Higher implied volatility means the market is anticipating wider price swings in the future compared to lower implied volatility.

This implied volatility rises during certain times like their major announcements from the government about policy or central bank meetings or individual stock’s board meetings. Traders usually anticipate a rise in volatility because when these events end, the implied volatility crushes giving advantage to option writers/sellers. This is a highly used trading technique by large capital players.

Traders look at comparisons between historical volatility and implied volatility to identify mispricings and trading opportunities. For example, it may indicate overvalued options if implied volatility is much higher than historical volatility.

Statistical Volatility

Statistical volatility uses quantitative models and forecasts to estimate a range for potential future price movements. It does not directly rely on past prices or option data. Some common statistical methods used include GARCH, EVWMA, and JP Morgan’s Risk Metrics model.

For instance, GARCH is a time series model that uses past volatility data to forecast volatility going forward. The expected future volatility estimated by these statistical models is also called forecasted volatility.

Investors use volatility measures to compare risk across securities, adjust position sizing, identify trade opportunities, and more. Understanding both past and expected future volatility is key to making informed investment decisions.

What is the Indication of Volatility Analysis?

Volatility analysis provides important insights and indications about the risk, potential returns, and overall market sentiment related to a particular security. One of the main insights that volatility analysis provides is quantifying the risk profile of a security. The higher the volatility, the riskier the security and the wider its potential price swings. Lower volatility indicates lower risk and more stable, predictable returns.

Volatility metrics like standard deviation give investors a statistical measure of risk that allows comparing volatility across securities. For example, Stock A has a higher risk profile if Stock A has a 30-day volatility of 25% and Stock B has a 15% 30-day volatility.

High volatility indicates greater risk but also indicates the potential for higher returns. Extreme price swings also mean profits are amplified along with risk. Volatile stocks have the potential for dramatic price gains in short periods. Investors need to weigh whether the risk is worth the potential reward based on their goals and risk tolerance.

Periods of volatility expansion or contraction often create trading opportunities. Analyzing shifts in volatility using metrics like implied versus historical volatility can signal mis-pricings in options or identify mean reversion opportunities.

For quantitative traders and volatility arbitrage strategies, changes in volatility trends are key markers to identify profitable trades. Volatility analysis highlights these potential opportunities.

Volatility trends also provide insights into overall market psychology and sentiment. Periods of high implied volatility compared to historical volatility signal investor fear and uncertainty. Low volatility suggests overconfidence and complacency.

For example, volatility will typically spike during market crashes as investors panic. Because when markets crash, traders and investors buy far month put options of index and stocks to protect their investments from damage. This long position in put options naturally increases the volatility causing greater fluctuations in price. Analysing volatility around earnings reports also gives clues into market expectations and reactions.

Volatility metrics help traders size positions appropriately and manage risk. Volatile securities require smaller position sizes and tighter stop losses. Less volatile securities allow for larger position sizes with wider stops.

Knowing a stock’s volatility characteristics aids in calculating the appropriate trade size for a given risk tolerance. It prevents overtrading volatile stocks or under-trading stable ones. Dynamic position sizing based on volatility helps manage portfolio risk.

The key indications from volatility analysis include determining a security’s risk profile, return potential, market sentiment, trading opportunities, and appropriate position sizing and risk management.

Understanding what volatility implies about these vital factors provides insights that allow investors to make strategic trades aligned with their objectives and risk-return profile. Volatility illuminates the personality and expected behavior of security, giving traders an edge.

How Does Volatility Analysis Contribute to Understanding Stock Market Behaviour?

Volatility analysis helps investors gain important insights into market sentiment, risk, and future price movements. Volatility is a direct measure of market risk and uncertainty. Higher volatility indicates larger price swings and greater uncertainty, while lower volatility reflects more stable and predictable conditions. Investors determine the level of risk involved in a particular stock, sector, or overall market by quantifying volatility. Popular volatility metrics like the VIX (the “fear measure” index) allow us to identify when market sentiment is becoming fearful or complacent.

Periods of low volatility signifies overconfidence and excessive optimism, while high volatility signals panic selling or period of uncertainty. Tracking volatility trends over time provides an objective view of how much uncertainty exists in the market. Analyzing volatility patterns helps traders identify opportune moments to enter or exit positions. Volatility tends to revert to the mean over time; spikes are often followed by declines, and vice versa. Traders profit from the eventual reversion by spotting extreme volatility readings that may be unsustainable.

For example, unusually high volatility presents a chance to buy on dips, while abnormally low volatility provides an opportunity to sell into strength. Traders also build strategies around volatility-based indicators like Bollinger Bands, which plot standard deviation levels above and below a moving average. Volatility analysis, overall, allows traders to time markets and capitalize on price changes.

The level of volatility is connected to where we are in the overall market cycle. Periods of expansion and optimism generally see low and stable volatility as bull markets steadily advance. As markets reach the late cycle and peak, volatility tends to rise. Finally, recessions bring extreme volatility spikes as investors react to unfamiliar negative conditions. Analysts determine what stage the market cycle is at and what may come next by observing volatility. For example, a sudden volatility uptick in a bull market could signal that the top is approaching. The market maxim “the bigger the boom, the bigger the bust” is directly linked to the evolution of volatility over the full market cycle.

Some financial studies have demonstrated a relationship between volatility and future market returns. Robert Shiller showed that stock prices fluctuate much more than changes in dividends explain, making the market excessively volatile. High volatility today might indicate lower-than-average returns in the future once the volatility normalizes. Panic selling and high volatility, on the flip side, tend to be followed by above-average returns going forward. One arrives at educated estimates for future market returns by assessing current volatility conditions. A simple strategy would be to increase stock exposure after major volatility spikes subside. The VIX index is an instrument used to measure volatility going on in the Indian market.

Volatility metrics are critical for measuring portfolio risk and constructing optimal asset allocations. The most basic portfolio decisions, such as stock/bond ratios, international exposure, and sector tilts, are improved by incorporating volatility. For example, shifting from stocks to bonds when stock volatility is elevated allows one to dynamically adjust portfolio risk. Many target-date retirement funds use volatility signals when deciding how much equity vs fixed income exposure to maintain over time. Beyond strategic asset allocation, options strategies like straddles and strangles are used for tactical portfolio protection if volatility appears likely to spike. Overall, analyzing volatility leads to better diversification and risk management outcomes.

Rising volatility indicates the growth of an asset bubble fueled by speculation. Volatility expands dramatically as prices detach further from fundamentals. This was observable in the lead-up to crashes like 1929, the tech bubble, and the housing bubble. One identifies bubbles and the associated systemic risks they pose by monitoring unusually sustained spikes in volatility. Central banks like the RBI also track volatility when measuring financial stability and bubble levels in the economy. Overall, abnormal volatility growth signifies bubbles forming and signals mounting risks of a crash once the bubble pops.

The proliferation of derivatives and volatility-linked ETFs has made volatility more accessible for analysis and trading. Volatility should be a key component of any systematic approach to the markets, combining both quantitative metrics and qualitative insights. While volatility is unnerving, understanding it more deeply arms investors with a significant advantage.

What Are the Key Indicators Used in Volatility Analysis?

The Cboe Volatility Index, or VIX, is the most widely followed measure of stock market volatility. Known as the “fear index”, it measures the implied volatility of Nifty 50 or Bank Nifty options across multiple strike prices. VIX values above 20 generally signal elevated volatility and investor fear, while values below 12 reflect complacency and low volatility. Sharp rises in the VIX often precede market bottoms, while sudden declines signal market tops.

Historical volatility calculates the degree of price variation for a security over a past period. It is measured statistically using the standard deviation of returns. 30-day and 90-day historical volatilities are the most common. This metric quantifies realized volatility based on actual prices, contrasting with implied volatility measures that are forward-looking.

Implied volatility (IV) represents the expected future volatility of a stock or index as implied by the prices of options on that security. It is computed from option pricing models like Black-Scholes. Implied volatilities tend to rise in bear markets and fall when optimism prevails. Comparing implied historical volatility identifies mispricings.

Standard deviation is a widely used indicator to track volatility of scripts.

Developed by John Bollinger, these bands plot standard deviation envelopes above and below a simple moving average. The width of the bands quantifies volatility; during tranquil markets, the bands narrow, while increased volatility pushes the bands wider apart. Price touches off the band’s signal overextended conditions and marks turning points. Bollinger Bands adjust dynamically to changing volatility conditions. The chart uploaded below shows how bollinger bands can be utilized to estimate the ongoing volatility in the script. Appropriate risk management should be incorporated to take high probability trades.

The Average True Range (ATR) calculates the average daily trading range over a period, accounting for gaps and limit moves. This provides a volatility metric useful for short-term traders making decisions on stop placement and position sizing. A high ATR signifies increasing volatility and choppiness, which are favorable for breakout strategies. A low ATR points to trading ranges where mean reversion approaches are effective.

Charting tools like Donchian Channels track volatility by plotting the highest high and lowest low prices over a lookback period. Wider channels reflect expanding volatility while contracting channels signal falling volatility. The price breaking out of the channel indicates a volatility regime shift, which identifies trading opportunities.

These indicators examine different aspects of ongoing and future volatility of the markets. Analysts take this information and create appropriate trading plans based on existing volatility as the higher volatility may hit stop losses due to larger fluctuations in the price. The multiple indicators and tools are used to form a complete picture about the market instability, risk and the trading opportunity. This gives possible direction of volatility in future.

What are the Types of Volatility in Stock Market Analysis?

Three primary types of volatility are widely recognised: Historical Volatility, which examines past fluctuations to discern trends; Implied Volatility, which is derived from the market price of a market-traded derivative (like an option); and Future-Realized Volatility, which is a projection of potential volatility based on statistical and mathematical models.

1. Historical Volatility

Historical volatility is a statistical measure of the degree of price fluctuation for a security over a specific period of time. It quantifies the dispersion of returns relative to the average return, indicating how rapidly and unpredictably prices have changed in the past.

Historical volatility is calculated by taking the standard deviation of past price changes over a set lookback window. Typically, historical volatility is expressed on an annualized basis, meaning the metric represents the expected amount of volatility over a 1-year period. Common lookback windows are 30 days, 60 days, and 90 days. The formula is:

Annualised Historical Volatility = Standard Deviation of Returns x √(Number of Periods per Year)

For example, the 30-day historical volatility for a stock is the standard deviation of 30 daily returns, annualized by multiplying by the square root of 365, since there are 365 trading days in a year.

This provides an objective and measurable way to quantify realized volatility and compare the volatility across different stocks or indexes. Higher historical volatility means wider price swings and more pronounced ups and downs, while lower volatility signifies more subdued and stable price action.

Historical volatility is important for investment analysis because it provides insights into an asset’s risk profile and an empirical basis for forecasting potential fluctuations. Below are its key uses.

- Estimate the typical range of returns for use in position sizing, stop losses, and risk management.

- Compare volatility across stocks and indexes to identify higher or lower-risk opportunities.

- Model potential future returns using Monte Carlo simulations based on historical volatility.

- Analyze the statistical relationships between volatility, returns, and other variables.

- Verify whether implied volatility levels priced into options match up with historical trends.

- Backtest trading systems across different historical volatility regimes.

- Identify volatility clusters, trends, spikes, and seasonal patterns through time series analysis.

The main advantage of historical volatility is that it directly quantifies realized volatility based on known prices rather than relying on estimates or assumptions. It is, however, backward-looking and may not capture shifts in volatility dynamics.

Historical volatility, which solely analyzes past price fluctuations, stands in contrast to both implied and forecasted volatility. While historical volatility provides an objective account of what has been directly observed, implied volatility looks into the future, estimating what the volatility is expected to be based on the market price of a derivative, such as an option. On the other hand, forecasted volatility uses models like GARCH to generate forward-looking volatility estimates grounded in historical data. Therefore, both implied and forecasted volatilities incorporate market expectations, assumptions, and statistical models, which distinguishes them from a purely historical perspective.

2. Implied Volatility

Implied volatility is a measure of the expected future volatility of a stock based on its option prices. Implied volatility indicates how much the market thinks the stock price will fluctuate in the future. Implied volatility differs from historical volatility because it looks forward rather than backward.

Implied volatility is derived from the price of a stock’s options using an options pricing model like Black-Scholes. This model calculates the fair value of an option based on variables like the current stock price, strike price, time to expiration, interest rates, and volatility.

You take the market price of an option and plug it into the pricing model along with all the other known variables to calculate implied volatility. Then you solve for the one remaining unknown, which is volatility. The volatility number that makes the model output match the actual market price is called implied volatility.

Higher implied volatility means the market thinks future stock price swings will be larger. Lower implied volatility means the market expects smaller price moves. Implied volatility generally increases when investors are uncertain and decreases when investors are complacent.

During major news and announcements, meetings, central bank or government policies, the implied volatility increases sharply and after these events end, the IV crushes. Option sellers use this crushing of IV as a straightforward measure of selling the highly priced options that are supposed to be settled due to events that have got over.

Implied volatility helps traders understand the market’s view on upcoming volatility. This insight into future expectations is valuable for six main reasons.

Buying and selling options

Implied volatility impacts option pricing. Understanding whether implied volatility is high or low allows traders to better time entries and exits. Options tend to be more expensive when implied volatility is high. Traders consider selling options when implied volatility is high. Options tend to be cheaper when implied volatility is low. Traders look to buy options when implied volatility is low and depressed.

Hedging portfolios

Checking implied volatility helps determine if options are overpriced or underpriced relative to historical norms. This allows for more cost-effective hedging against stock price moves. During a market crash, investors buy index put options to protect the portfolio.

Forecasting stock volatility

Traders look to implied volatility rather than historical volatility when estimating future volatility. Implied volatility reflects the market’s forward-looking view, whereas historical volatility looks backwards.

Determining sentiment

High implied volatility signals fear among options traders. Low implied volatility suggests complacency. Monitoring implied volatility reveals how uncertain or confident investors feel about future stock price action.

Evaluating mispricing

Large discrepancies between implied and historical volatility signal mispriced options. Traders look to capitalize on these distortions.

The key difference between implied and historical volatility is that implied looks forward, while historical looks backward. Historical volatility measures past price fluctuations over a specific timeframe. It is calculated from actual stock prices using statistical formulas. Historical volatility only tells you what volatility was over a past period. Implied volatility is derived from option prices and represents the market’s expectations for future volatility. It tells you what the volatility is expected to be over the life of the option contract. Historical volatility is based on known actual results; implied volatility is an educated guess about the future. Traders mainly rely on implied volatility for decision-making because it provides a forward-looking perspective.

3. Future-Realized Volatility

Future-realized volatility refers to the actual volatility realized over a specific future period. Future-realized volatility is an important metric to compare with implied volatility to see how accurately options markets can forecast upcoming volatility.

Future-realized volatility is the historical volatility calculated over a defined future timeframe. For example, a trader may look at the future-realized volatility of a stock over the next 30 days. You have to wait until the end of the future period to calculate it. Then take the stock’s price changes over that period and plug them into a historical volatility formula. Common measures include the standard deviation of returns or variance. The volatility result tells you the actual volatility the stock experienced over the future time frame. This is known as future-realized, realized future, or simply future volatility.

Comparing future-realized volatility to implied volatility is crucial for evaluating the performance of options pricing models. Implied volatility is the market’s forecast, while future-realized volatility is the actual result. The accuracy of the forecast determines how well investors are able to estimate upcoming volatility. Key uses of future-realized volatility include the following.

Testing implied volatility

Implied volatility is lower than future-realized volatility, meaning actual volatility exceeded the market’s estimates. This suggests traders were not bearish enough. Traders overestimate the actual volatility if implied volatility is higher.

Improving forecasting models

Comparing implied to future-realized volatility allows for continual improvement of option pricing models. Models are adjusted to align implied volatility closer to eventual results.

Determining trader performance

Traders rely on implied volatility to make trading decisions. Comparing it to future-realized volatility shows if their volatility assumptions were correct. Good volatility forecasts lead to better trades.

Analyzing sentiment

Consistently high implied volatility relative to future-realized volatility may signal a bearish bias among options traders. Traders expect bigger moves than they materialize.

Identifying mispriced options

Divergences between implied and realized volatility reveal expensive or cheap options to trade. Options may be mispriced relative to actual volatility.

Implied volatility is a forecast, while future-realized volatility is the actual outcome. Implied volatility is what options traders expect volatility to be over a future period. Future-realized volatility is the volatility that truly unfolds over that timeframe. Since future-realized volatility cannot be known in advance, traders rely on implied volatility to estimate where future volatility will be. Comparing the two metrics after the fact evaluates the accuracy of implied volatility forecasts.

Implied volatility is calculated from current option prices using an options pricing model. Future-realized volatility is based on the actual historical volatility realized over a future time frame. Implied volatility represents expectations for the future. Future-realized volatility tells us what actually happened. Implied volatility is forward-looking. Future-realized volatility is backwards-looking over a future period. Implied volatility reflects market sentiment. Future-realized volatility eliminates sentiment and provides an objective volatility measure. Implied volatility is readily available in real time. Future-realized volatility is only calculated retroactively after a time period passes.

What Are the Major Factors that Influence Stock Market Volatility?

Stock market volatility refers to the magnitude and frequency of price fluctuations in the overall market or individual stocks. Certain factors impact volatility levels. Understanding these influences provides insight into the causes of market fluctuations. The major factors that drive stock market volatility include the thirteen listed below.

1. Economic News

Major economic data releases like jobs reports, GDP, inflation, and consumer sentiment move markets if the numbers deviate significantly from expectations. More positive news tends to lower volatility by reassuring investors. Weaker economic reports tend to increase volatility and uncertainty.

2. Central Bank (Reserve Bank of India RBI) Policy

Changes to interest rates and monetary policy by the RBI impact stock valuations, risk appetite, and volatility. Accommodative policy like rate cuts reduces volatility while tightening policy like rate hikes generally boost volatility.

3. Geopolitical Events

Major global political developments like elections, wars, revolutions, and unrest add uncertainty and volatility. Investors dislike instability and policy shifts. Events reducing geopolitical tensions calm markets, while conflict and uncertainty cause volatility spikes.

4. Corporate Earnings

Quarterly earnings reports from major companies provide insight into their financial health and growth outlook. Strong earnings and guidance lower volatility by signaling healthy business conditions. Disappointing results or guidance stoke volatility by increasing uncertainty.

5. Investor Sentiment

Bullish sentiment reduces volatility as optimism steadies markets. Bearish sentiment increases volatility due to increased fear and uncertainty. Sentiment extremes often signal volatility changes as markets revert to the mean.

6. Technical Levels

Key technical price levels like previous highs and lows often act as support or resistance. Breaking above resistance or breaking below support frequently sparks volatility as it signals a potential trend change.

7. Market Corrections

Sustained market downturns increase volatility due to negative sentiment, uncertainty, and increased trading activity around the declines. Corrections tend to persist until uncertainty subsides.

8. Sector and Industry Trends

Volatility frequently emerges in specific sectors based on industry conditions. Examples include tech volatility, energy volatility, and financial volatility. Issues impacting key sectors spread to the overall market.

9. Institutional Trading

Trading by large institutions like hedge funds, mutual funds, and banks whips markets around in the short run based on repositioning. Increased institutional trading generally elevates intraday volatility.

10. Retail Investor Activity

Surges in trading by individual investors, especially using options or margin, increase speculative activity. This exacerbates volatility as retail money amplifies market swings.

11. Algorithmic/High-Frequency Trading

Computerized trading systems trigger big price swings by reacting to news events or technical levels in milliseconds before humans process information. This exacerbates intraday volatility.

12. Index Rebalancing

Indexes like the Nifty 50 rebalance their constituent stocks, which forces institutional investors to trade stocks going in or out of the index. This trading on index adjustment days spikes volatility.

13. Financial Crises

Extreme events like recessions, market crashes, and credit crises drastically elevate volatility due to unprecedented uncertainty and selling activity as investors liquidate assets. This is seen in events like the 1930s Great Depression or the 2008 Financial Crisis or COVID Fall. The fallout has kept volatility high for years.

Volatility often creates opportunities for savvy investors who distinguish between normal volatility causes and more persistent risks.

How Can Volatility Analysis Help Investors Manage Risk in Their Stock Market Portfolios?

Volatility analysis metrics like the standard deviation help determine an appropriate position size based on a security’s usual price range. High-volatility stocks warrant smaller positions to limit risk. Low-volatility stocks can justify larger positions. Proper position sizing ensures that no single position jeopardizes the portfolio. Analyzing the correlation between the volatility of different assets helps construct diversified portfolios. Securities with low or negative correlations have volatility that moves independently. Combining these assets minimizes overall portfolio volatility and concentration risk.

Volatility allows for quantifying a security’s risk-reward profile. High-volatility assets should generate sufficient returns to compensate for their elevated risk. Comparing volatility to expected returns ensures an adequate payoff for the risk level. Measuring current implied volatility helps forecast upcoming volatility and expected risk. Security selection can factor in implied volatility to target trades with favorable risk-return outlooks.

Derivatives like options are used to hedge volatility risk. Comparisons between implied and historical volatility reveal when options are overpriced or underpriced relative to typical movements. This facilitates cost-efficient hedging. Volatility metrics like the standard deviation are used to construct projected drawdown ranges for a portfolio. Investors can size positions to limit drawdown risk or adjust holdings proactively as prices approach expected drawdown levels.

Conservative investors can utilize low-volatility stocks and derivatives to minimize capital losses during downturns. Managing volatility preserves capital for additional opportunities later in the cycle. Spikes in volatility often signal transitions from bull to bear markets. Heightened volatility provides warnings to adjust allocations to more defensive positions before large corrections unfold.

During volatility expansion, investors often take a step to buy far month put options in order to protect the equity holdings. The strategy is well known and it indeed increases the volatility further. The risk management models are usually breached in high volatility environments that is the reason investors actively hedge the portfolio to control damage.

Quantifying volatility helps determine the required portfolio liquidity for rebalancing and meeting cash flow needs. Greater liquidity buffers are necessary for high-volatility assets. Comparing portfolio volatility to market benchmarks aids asset allocation decisions based on the desired risk profile. Lower volatility than a benchmark may signal excessive conservatism. Exceeding benchmark volatility may indicate undue risk concentration.

What are the common statistical models used in stock market volatility analysis?

Volatility modeling is essential for quantifying and forecasting price fluctuations. Statistical models provide mathematical frameworks for estimating volatility based on historical data and relationships between variables. The most common statistical models are as follows.

- Simple Moving Averages: The moving average of a security’s price over a set timeframe serves as a basic volatility indicator. Shorter windows focus on near-term volatility, while longer windows measure long-term volatility trends.

- Weighted Moving Averages: Applying greater weight to more recent data and less weight to older data allows you to react faster to volatility changes. Exponentially weighted moving averages accomplish this easily.

- Bollinger Bands: Applying moving average bands several standard deviations above and below a price plot highlights periods of high and low volatility. Wider bands reflect higher volatility.

- ARCH/GARCH Models: Autoregressive conditional heteroskedasticity models forecast volatility based on past volatility clustering and mean reversion. Generalised ARCH adds exogenous variables like interest rates.

- Stochastic Oscillator: This momentum indicator measures volatility as well as the speed of price movement. Oversold below 20 and overbought above 80 signal upcoming volatility reversals.

- Parkinson Volatility: This isolates volatility independent of price drift using the high/low price range. It offers a simple volatility metric based on daily data.

- Garman Klass Volatility: An extension of Parkinson’s modeling using both the high/low range and open/close prices. Provides more stable volatility estimates.

- Rogers-Satchell Volatility: Another range-based model using open, high, low, and close prices. Weights closing prices heavily to capture volatility at market close.

- Intraday Volatility: Measures volatility over set intraday time frames rather than daily. Reveals how volatility changes throughout trading sessions.

- Realized Volatility: Sums daily squared returns over time frames like a month or year. Provides historical volatility averages over long periods.

- Implied Volatility: Uses option prices and the Black-Scholes model to quantify the expected future volatility implied by the options market. India VIX is an index used to study implied volatility for Indian markets. Derivative traders watch the VIX constantly to monitor IV situations.

- GARCH Volatility Forecasting: Predicts future volatility by modeling volatility clustering and mean reversion in residual returns using past data.

- Value at Risk (VaR): Estimates volatility-adjusted maximum loss thresholds for a position or portfolio at a given confidence level. Useful for quantifying downside risk.

Applying statistical models to stock price data reveals insightful volatility patterns and trends. Simple volatility averages provide baseline analysis, while more advanced models deliver detailed forecasts and volatility derivatives. Combining modeling approaches provides robust insights for guiding investment decisions and risk management. Volatility lies at the heart of most statistical analyses due to its central importance for quantifying risk and uncertainty.

How Does Regime Shift Impact the Stock Market Volatility?

Regime shifts refer to transitions between periods of high and low volatility in financial markets. These shifts in volatility trends dramatically impact stock market volatility and are driven by changes in investor sentiment, risk perceptions, and market structure. Regime shifts can create opportunities but also lead to greater uncertainty and risk.

During low-volatility regimes, stock market volatility declines as investor sentiment remains persistently bullish and risk appetites are high. Stocks experience extended rallies with shallow and brief pullbacks. Implied and realized volatility dropped to low levels not seen since before the 2008 financial crisis. This steady tranquility, however, breeds investor complacency and vulnerability to shocks.

Markets are full of uncertainty. The uncertainty persists in every regime. In low volatility situations, price fluctuation is less thus the gains are steady and exposed risk is eventually less but when the regime shifts to high volatile situations like a geopolitical event or bad economic news, the market sentiment is shifted and there is increased risk of losses due to larger price fluctuations. This regime shift in high volatility situations makes conservative traders take short trades and protect gains generated during low volatility periods. Even algorithms may undergo slippages during flash crash. This creates lesser liquidity that in turn contributes to falling prices.

What Does High Volatility Mean for Stock Market Investors?

Periods of high volatility in the stock market present both risks and opportunities for investors. Volatility refers to the magnitude of day-to-day price fluctuations in the market. High volatility is characterized by large daily swings and heavy trading volume as investors react to new developments. Understanding the implications of spikes in volatility is key to navigating turbulent markets.

High volatility triggers greater uncertainty and fuels fear. This fear inturn triggers investors to protect portfolio holdings by making short trade setups in futures. These investors often buy far month index put options and stock options to protect control the damage on the gains.

Majority of times, high volatility indeed fuels bearish sentiment thereby panicking short term and long term buyers.

The larger price fluctuations cause greater degree of emotional instability between traders and investors. Thus maintaining a disciplined approach is crucial.

High volatility removes the weak hands that may have gained some returns on their respective investments.

High volatility frequently occurs around market regime changes and major turning points. For example, volatility spiked during the COVID crash removed the weak hands but provided discounted entries to value and patient investors.

High volatility indicates elevated uncertainty and investor fears. Markets hate uncertainty. It signals investors are having trouble quantifying risk and forecasting returns when volatility rises. This makes participants more reactive and prone to selling into weak bounces. High VIX readings above 20 indicate high volatility and investor anxiety.

Traders adept at trading volatility thrive during spikes. Options, volatility ETFs, and VIX futures provide opportunities to capitalize on big swings. However, trading these instruments requires extensive volatility knowledge.

What Does Low Volatility Means for Stock Market Investors?

Stock market volatility declining and remaining persistently low signals a stable, trending market. However, extended periods of low volatility also lead to investor complacency and vulnerability to shocks. Understanding the implications of low volatility provides useful insight for portfolio management.

Low volatility indicates investors broadly agree on the market’s direction and outlook. Uncertainty diminishes significantly during prolonged bull runs. The VIX falling below 15 shows investor fears have evaporated. With reduced uncertainty, investors focus on buying dips rather than selling rips.

Low volatility usually fuels bullish sentiment the majority of times. As the price fluctuations are small, traders and investors enjoy sluggish and trendy gains. Risk is lesser and so are the gains. Low volatility is liked by traders, they end up discarding the risk management rules and end up chasing markets in hunger for steady profits.

Sustained low volatility situations give way to renewed volatility regimes. The shift occurred just before the COVID crash that wiped out the gains generated during these low volatility situations.

Low volatility reduces the number of tradable swings and opportunities in short-term instruments like options. Markets become trending and directional with limited counter-swing trades. Strategies are adaptable to trending markets.

Does Volatility Represents How Large an Asset’s Prices Swing from the Mean Price?

No, this is an oversimplification of what volatility represents. Volatility includes more specific statistical measures, although it is related to the degree of price fluctuation around a mean or average price.

More accurately, volatility refers to the standard deviation of an asset’s returns. The Standard deviation quantifies how dispersed the returns are from their average. It is calculated by taking the square root of the average squared deviations of returns from their mean.

So in mathematical terms, volatility generally refers to how much asset prices deviate from their mean. But the standard deviation is the specific statistic used to quantify volatility, not just the general amount prices vary from their average.

Is Standard Deviation One of the Other Ways to Measure Volatility?

Yes, standard deviation is one of the most common and widely used measures of volatility in finance. The Standard deviation quantifies the amount of variation or dispersion in a set of values from their average (mean). The Standard deviation is calculated using the historical returns of a security or market index. The standard deviation of returns measures how much those returns typically deviate from the average return over a period of time.

Larger standard deviations indicate higher volatility; smaller standard deviations indicate lower volatility. An example is attached below. The chart is of Infosys Ltd and the green line is the Standard Deviation indicator. The blue vertical line represents the times of greater volatility whereas the orange line represents the times of lower volatility.

Does Volatile Assets are Considered More Riskier than Less Volatile Assets?

Yes, volatile assets are generally considered riskier than less volatile assets in investing. More price fluctuations indicate greater uncertainty in returns. Volatile assets have wider distributions of possible returns, including larger potential losses. This makes returns less predictable. Volatility represents the potential for a permanent loss of capital.

Stocks with high volatility have a greater chance of sharp declines compared to stable assets like bonds. Volatile assets require constant monitoring and risk management. Less volatile assets need less oversight to hold for the long term. Psychologically, volatile assets test investor discipline due to frequent price swings. It’s easier to stick with less volatile holdings through ups and downs.

Is Volatility an Important Variable for Calculating Options Prices?

Yes, Volatility is one of the most critical variables in determining fair values for option contracts. The volatility of the underlying security directly impacts the probability of the option finishing in the money by expiration. Quantifying volatility is essential for pricing models to accurately calculate the fair premium the option should trade for based on its playoff probabilities.

The most widely used options pricing model, the Black-Scholes model, has volatility as one of its key inputs along with stock price, strike price, time to expiration, interest rates, and dividends. The volatility input relies on historical volatility as a proxy for expected future volatility. Higher volatility assumptions increase the probability of the stock reaching the option’s strike price, thus raising the fair value price for the option.

Comparing implied and historical volatility often reveals when options are overpriced or underpriced relative to historical trends. For example, options may imply much higher volatility than historical expectations for an upcoming event like an earnings report. This signals expensive options. Options sometimes imply lower volatility than historical levels following a spike in volatility that has since reverted. This presents potential opportunities to buy cheap options in anticipation of volatility normalizing.

Does High Volatility Represents only bearish markets?

No, high volatility represents bearish markets 99% of the time. But in shorter time periods, high volatility can result in a clean bullish trend for a short period as the derivative positions experience short covering. The short covering in derivatives means mass exit of call sellers, fresh call buys, future short exits, fresh long future positions and fresh long equity positions that contribute in increasing the upside potential thereby increasing the volatility as well.

Traders and investors are supposed to note that such volatility spikes settle faster when markets turn bullish. Because the majority of times, the volatility increase leads to panic and fear that causes bearish sentiment to increase causing markets to pull back, fall or even crash. The chart uploaded below showcases how 1% of time, rise in volatility may cause markets to rise. The volatility rose, causing exit of derivative short positions that resulted in sharp breakout. Notice the volatility cooled down immediately after a significant rise.

Previous Article

Previous Article

31")

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 34")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 35")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 36")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 40")

No Comments Yet.