The ratio put spread is an options trading strategy that aims to generate profit by leveraging the predictable decay of set options premium over time. In ratio put spread, a trader sells more put options than they purchase, with all options having the same expiration date but different strike prices. Typically, the sold puts will be at a lower strike price than the purchased puts. By establishing this ratio structure, the trader takes on increased obligations if the underlying stock moves strongly lower.

However, the strategy is profitable if the stock remains stable or moves higher as time passes. This is because the premium value of all positions will naturally decline as the options near expiration. For the trader, the ratio is designed so that this expected “time decay” generates profits even if the stock finishes slightly below the short strike price. While offering this potential, ratio put spreads also carry significant risks. If the market moves sharply against the trade, all short puts could be assigned, resulting in losses greater than the premium collected.

For this reason, traders employ risk management techniques like position sizing to limit the downside. Ratio put spreads require accurate prediction of stock behaviour and volatility. They are best suited for outlooks expecting limited short-term downside but acknowledge the risk of higher losses if predictions prove wrong. Careful analysis is needed to employ this leveraged strategy appropriately.

What is the Ratio Put spread?

A ratio put spread, or put ratio back spread, is an options trading strategy used to profit from a moderate downside move in the underlying security. A ratio put spread involves buying a number of put options at a higher strike price and selling more put options at a lower strike price in a ratio of longer puts to short puts.

The ratio put spread aims to capitalise on situations with an expectation of a modest decline in the underlying security. By using a ratio of more long puts versus short puts, the strategy creates a net debit position that has unlimited profit potential on the upside and limited risk on the downside.

The trader would carry out the following actions to open the position.

First, buy more put options with a higher strike price (this is the long put leg).

Second, sell fewer put options at a lower strike price (this is the short put leg).

The disparity between the number of long and short puts creates a net debit, meaning the trader pays a premium to establish the spread. However, the maximum loss is limited to the net debit.

Here is an example to help you understand.

Stock ABC is trading at Rs. 50.

A trader buys 2 put contracts with a strike price of Rs. 45 for Rs. 2 per contract.

Trader sells 1 put contract with a strike price of Rs. 40 for Rs. 3 per contract.

Net debit to initiate the trade is Rs. 1 per share ((2xRs. 2) – Rs. 3).

The maximum loss on this trade is the Rs. 1 debit paid to put on the position. The maximum gain is unlimited if the stock falls below the long put strike of Rs. 45. The critical P/L situations are shown below.

The entire debit of Rs. 1 per share is lost if ABC stock stays above Rs. 45 at expiration.

The position breaks even if ABC drops to Rs. 44.

The short put leg is assigned stock at Rs. 40 if ABC drops below Rs. 40, while the long puts gain value, allowing for potential unlimited upside.

The ratio put spread benefits from time decay on the short puts, allowing the trader to collect more premium than what was paid. It profits from a moderate downward move in the stock. However, if the stock crashes below the short put strike aggressively, losses sometimes accumulate quickly.

Proper position sizing is essential with a ratio put spread, as the short puts expose the trader to more shares of the underlying security. The risk-reward profile is similar to simply owning the stock but with limited downside risk.

The ratio put spread allows traders to take advantage of rich put premiums while limiting maximum loss. By selling fewer puts at the lower strike and buying more at the higher strike, the position benefits from volatility contraction. The put ratio backspread offers a means to sell expensive options while retaining the ability to profit if the underlying stock declines moderately. It sometimes produces consistent profits when appropriately managed if the trader’s view on market direction proves correct.

How does Ratio Put Spread work?

Ratio put spread work by combining short and long put options at different strike prices on the same underlying asset to profit from a sharp move lower in the underlying price.

A ratio put spread is constructed by selling one put option at a higher strike price while buying two or more put options at a lower strike price. All the options share the same expiration date. For example, a trader could implement a 1×2 ratio put spread by selling 1 XYZ 50 put and buying 2 XYZ 45 puts.

The short put generates income from the premium received and has uncapped downside risk if the underlying drops below the 50 strike at expiration. The multiple long 45 puts provide leveraged profits if the price falls below 45. The maximum loss is limited to the spread between the strikes minus the net premium received.

This strategy aims to benefit from a pronounced decline in the underlying asset. The short put provides income to offset the long put costs and define risk. The multiple long puts create amplified profits if the bearish forecast is correct. Ratio put spreads allow traders to profit from a sharp move lower while limiting losses if the drop does not materialize before expiration.

The ratio put spread aims to benefit from a modest decline in the stock by utilising more long puts versus short puts. It offers a helpful method for profiting from pessimistic forecasts with specified and constrained downside risk when managed carefully. The imbalance between the number of long and short puts creates the leverage for potentially substantial profits. The ratio put spread sometimes generates reliable profits while limiting losses when employed appropriately and in the appropriate market circumstances.

What are the components of Ratio Put Spread?

Longs puts, short puts, strike prices, expiration date, etc, are the critical components of the Ratio put spread. Below is more information.

1.Long Put Options

Extended put options give the buyer the right, but not the obligation, to sell the underlying asset at the strike price on or before the expiration date. The long puts are purchased with the expectation that the underlying stock will fall below the strike price, allowing the put options to be exercised or sold back at a profit.

The buyer pays an upfront premium to purchase the extended put options. The maximum loss is limited to this premium paid. However, the profit potential is substantial if the underlying stock falls sharply below the strike price. The intrinsic value of the long puts increases as the stock declines.

Long puts are often used to speculate on downside moves or hedge an existing long stock position. They provide leveraged exposure to bearish sentiment on the underlying. The defined and capped risk profile from long puts makes them advantageous for specific trading strategies.

The primary purposes of incorporating long-put options into an options trading strategy are the following mentioned.

Profit from a sharp decline in the underlying stock without having to short-sell shares. The long puts provide leveraged profits if the bearish view is correct.

Protect an existing portfolio or long stock position from substantial downside risk. Long puts help limit losses if the underlying asset falls.

Sell the long puts back at a higher premium if implied volatility rises after purchase. The time value erodes more slowly for longer-dated puts.

Control many shares for a fraction of the cost of buying the stock outright. It allows taking a directional view with a lower capital outlay.

Maximum loss is capped at the premium paid for the extended put options. Risk is quantifiable, unlike short-selling stock.

Calendar call spreads involve buying long-dated call options and simultaneously selling short-dated calls at the same strike. Adding extended put options at the same strike as the short call leg serves to define and limit the maximum risk.

Without long puts, calendar call spreads face an uncapped downside if the stock falls sharply below the strike price. The naked short calls would be exposed to unlimited losses in a crash.

By incorporating extended put options, the maximum loss is reduced to the net premium paid to establish the entire position. The long puts protect the strike price while the upside remains unlimited from the extended call options.

The long puts in a calendar call spread act as a form of cheap downside insurance. They allow traders to define and contain the risk on short-call options with a high probability of expiring worthless.

2. Short Put Options

Short put options obligate the seller to purchase the underlying asset at the strike price if the options are exercised by the buyer. The short puts are sold to collect premium income in exchange for taking on the obligation to buy the stock if it falls below the strike.

The seller receives the premium upfront by writing the short put options. The maximum gain is limited to this premium collected if the puts expire worthless. However, substantial losses sometimes occur if the stock declines sharply below the strike price at expiration.

Short puts are often used to earn income from overvalued stocks expected to remain range-bound or rise. They must buy the stock at disadvantageous prices if bearish sentiment emerges. Managing this downside risk is critical with short-put strategies.

The primary purposes of incorporating short put options into an options trading strategy are the following.

Income Generation, earn premium income by selling puts on stocks forecasted to remain flat or rise. It is ideal for overvalued stocks with rich put premiums.

Entry Strategy, get paid to become obligated to buy a stock at a lower price. Allows entering a position at a discount to the current market.

Leverage Gains, sell puts on a more significant number of shares than are afforded to control with the outright purchase of stock. Provides greater upside if the stock rises.

Speculation, profit from rich put premiums if the view of limited downside in the stock is correct. Serves as an alternative to short-selling stock.

Reduce Cost Basis, the original premium collected lowers the effective purchase price if we assign stock on the short puts.

Calendar call spreads use short-dated short calls to fund long-dated long calls. Adding short puts at the same strike as the short calls provide premium income to offset the cost of the spread.

The short puts do not add downside risk since the naked short calls already carry an uncapped risk if the stock falls. The additional short puts allow for collecting more premium income.

The short puts expire worthless for maximum gain if the stock remains above the strike price. Short calls and puts are assigned at the same price if the stock goes below the strike, maintaining losses consistent with holding the calendar call spread.

The short puts provide incremental income and allow share ownership at an effective net cost basis reduced by the premium collected. In calendar call spreads, short puts augment profits while maintaining defined risk.

What is the Purpose of Ratio Put Spreads?

The primary purpose of ratio put spreads is to profit from a sharp downward move in the underlying asset while limiting potential losses if the bearish forecast does not play out.

Ratio put spreads aim to amplify profits on the downside by utilizing multiple long put options. The few short puts serve to lower the net cost of the spread and define maximum risk.

Traders use this strategy when they expect a pronounced decline in the underlying price but wish to implement the trade at a lower net cost compared to only buying puts outright. The short puts also limit losses if the drop does not materialize or is more modest than expected.

The dual long puts provide leveraged exposure to increase profits if the underlying falls sharply below the long strike price. This compensates for the short-term exposure above that level.

Ratio put spreads are used when the trader has a bearish outlook and expects the price of the underlying asset to decrease significantly by options expiration.

By purchasing more long puts at a higher strike price and selling fewer short puts at a lower strike price, the position realises leveraged gains from downward price moves. The higher number of long puts accumulates intrinsic value faster.

The trader can benefit from a significant downward move while capping and defining maximum loss exposure if the bearish forecast is wrong.

Why might an investor choose to use a ratio put spread strategy?

The primary motivation for using a ratio put spread is having a moderately bearish outlook on the underlying stock. This options strategy aims to profit from a controlled downward move, not a significant crash. The ideal scenario is a modest dip in the stock price. A ratio put helps capitalise on moderate bearishness.

With a ratio put spread, the imbalance between the number of long and short puts creates asymmetric leverage to downside moves. The additional long puts provide greater sensitivity to declines in the stock. This leveraged exposure allows profiting more from the anticipated downward trend.

A significant benefit of the put ratio spread is the maximum loss is strictly limited and quantifiable. There is a cap on the downside even if the stock drops precipitously. For investors looking to define and contain potential losses, this strategy offers appeal.

Establishing ratio put spreads involves an upfront debit but requires less capital than taking a short stock position for similar downside exposure. The net cost is also reduced by premiums collected from the short put leg.

Ratio put spreads carry defined, fixed risks not found in outright short selling of stock, which faces theoretically unlimited losses. For traders aiming to express bearish views with risk controls, this strategy provides an alternative.

Investors sometimes use ratio put spreads when implied volatility is elevated, benefiting from rich premiums on short puts. Potential volatility compression after initiating the trade would enhance profits.

Incorporating a ratio put spread on an underlying stock held in a portfolio provides a hedge to protect against moderating pullbacks. The long puts help cushion the downside, while the short puts lower costs.

Ratio put spreads allow positioning for measured downside in stock while limiting losses if wrong. For investors and traders with moderately bearish biases and a desire to control risk, this strategy is advantageous under the right market conditions. The ability to profit from downtrends using defined, capped risk makes ratio put spreads a compelling choice.

What is the strategy of Ratio Put Spread?

The ratio put spread is an options strategy that involves buying more long put options at a higher strike price and selling fewer short puts at a lower strike price. This unequal number of puts creates leverage to benefit from a bearish outlook on the underlying asset.

The strategic advantage of ratio put spreads is the ability to profit from significant downward moves while strictly defining maximum losses. The strategy’s main components are listed below.

Ratio put spreads allow speculating on bearish price moves with capped downside risk. Maximum loss is limited to the net debit paid upfront to establish the spread position. This defined risk enables using leverage without exposure to unlimited losses.

The strategy provides a favourable risk-reward profile. Potential gains have unlimited upside if the price drops sharply, while losses cannot exceed the debit amount. This asymmetry aligns with the trader’s objective to profit from a decline.

The use of additional long puts versus short puts creates asymmetric leverage. Buying more puts increases positive exposure to falling prices without requiring a proportional increase in capital outlay.

For example, a 2:1 ratio controls 200 shares with a margin requirement of just 100 shares. The higher leverage leads to outsized percentage gains relative to the margin committed.

A key strategic advantage is the ability to pursue leverage with capped losses. This differentiates ratio put spreads from outright long puts or shorting stock, which have unlimited risk.

Buying long puts alone requires paying the full premium, which is sometimes expensive due to high implied volatility. Ratio put spreads reduce net cost through the credit from short put sales.

The lower capital outlay improves the strategy’s risk efficiency. Compared to naked long puts, the maximum loss is lower for the same upside potential.

Varying the ratio, strikes, and expiration allows fine-tuning the risk-reward balance. Wider spreads increase leverage but also increase the debit. Higher ratios amplify both upside and downside exposure.

The trader sometimes strategically customises the position to their outlook and risk appetite. This flexibility helps calibrate the optimal strategic use of capital for a given trading opportunity.

Ratio put spreads sometimes hedge portfolios by benefiting from market pullbacks. Their defined risk makes them attractive for insuring long stock positions against ephemeral declines.

The strategy enables efficiently capitalising on bearish outlooks across diverse scenarios – from sector rotations to rising volatility to anticipating recessions.

The strategy of ratio put spreads uses defined risk and asymmetric leverage to profit from bearish views on the underlying. The risk-reward profile and cost-efficiency, when appropriately organised, offer an alluring tactical tool for speculating on declining prices.

How does a ratio put spread profit from changes in the underlying asset’s price?

A ratio put spread generates profits based on the price action of the underlying stock in relation to the strike prices of the long and short puts. The imbalance between more long puts versus short puts creates asymmetric leverage to benefit from downside price moves.

The ideal situation is for the stock to decline moderately and finish right between the strike prices of the long and short puts at expiration. In this case, the long puts end up deep in-the-money with significant intrinsic value.

Meanwhile, the short puts expire worthless, resulting in the trader keeping the full premium collected. This allows the position to realise the maximum gains.

The trader is assigned on the short put contracts and must buy shares at that lower price if the stock falls precipitously below the strike price of the short puts. However, the long puts become extremely valuable in this scenario and offset any losses.

In fact, if the stock were to drop to zero, the profits from the long puts would outweigh the losses on the short puts. The additional number of long puts creates a buffer that insulates the position from substantial downside moves.

The long and short puts expire worthless if the stock rises or stays above the long put strike at expiration. The trader’s loss is limited to the net debit paid when initiating the trade. The short puts cap and defines the maximum risk in this upmove scenario.

The ratio put spread is structured to benefit from moderate downside moves in the stock. The additional long puts create enhanced sensitivity and leverage to lower prices. While unlimited losses are theoretically possible if the stock rises sharply, the short puts cap and defines maximum risk under most scenarios. Volatility trends also impact the strategy’s profit potential from the asymmetrical long/short put ratio.

What is the risk-reward profile of a ratio put spread?

A key feature of ratio put spreads is their defined and capped maximum loss. The most the trade sometimes loses is the net debit paid upfront when establishing the spread position.

For example, suppose a 2:1 ratio put spread is initiated for a net debit of Rs. 200. In that case, the maximum downside is strictly limited to Rs. 200, no matter how far the underlying price might move against the trade.

This defined risk creates an attractive asymmetric risk-reward profile. The spread gains leveraged upside from downward moves in the underlying while losses cannot exceed the fixed debit amount.

In contrast to the strictly defined maximum loss, the potential profit of ratio put spreads has no upside limit. The more the underlying asset price declines below the long put strike prices, the greater the gains realised.

For example, if the price were to drop to zero, the long puts would be valued at their total strike price, resulting in the maximum possible profit. The short puts would expire worthless in this scenario.

The uncapped profit potential comes from the unequal number of long versus short puts. The additional long puts accumulate intrinsic value faster from downward moves, leading to leveraged gains.

The trader sometimes adjusts the risk-reward payout through brilliant strike selection and ratio management. Wider spreads between the long and short strikes increase potential profits but also increase the net debit and maximum loss.

Higher ratios like 2:1 or 3:2 provide greater upside from downward moves but also increase the upfront costs. More conservative 1:1 spreads have lower breakevens but capped profits.

An aggressive trader confident in a bearish forecast sometimes utilises a wide 2:1 spread to maximise optics gains. A more cautious trader sometimes prefers a narrower 1:1 spread to limit the debit amount at risk.

The risk-reward profile also changes as the options decay in value towards expiration. Time decay erodes value more significantly for the short puts compared to the long puts.

This sometimes creates profits for the spread position even if the underlying remains flat. Short put time value erosion helps offset the slower time decay in the long puts.

The flexible nature of ratio put spreads allows traders to strategically craft positions with risk-reward profiles aligned closely with their market outlook and risk tolerance. The uncapped upside potential and defined downside make the tradeoffs attractive.

What are the advantages of using Ratio Put Spread?

Ratio put spreads offer traders defined, fixed risks while providing uncapped profit potential on downside moves. Here are six key advantages of using ratio put spreads as an options trading strategy.

1. Defined and Limited Risk

The maximum loss is strictly quantified based on the net debit paid to establish the position. Short puts cap and limit downside risk, even if the stock drops to zero. Known, fixed bets, unlike short stock, which has unlimited potential loss.

2. Leverage

More long puts versus short puts provide greater sensitivity to downside moves. The asymmetry acts like leverage on a short stock position for enhanced profits. Controls more shares for less cost compared to buying stock outright.

3. Unlimited Profit Potential

Ability to realise uncapped gains if the stock falls sharply below the short put strike. Additional long puts offer runaway profits in substantial downdrafts theoretical limit on how much sometimes is made on the upside.

4. Lower Capital Requirements

The initial net debit cost to trade is smaller than taking equivalent short stock position.

Defined risk allows leveraging limited trading capital to control larger positions. Short puts generate income, helping offset the cost of long puts.

5. Volatility Targeting

Benefits from rich option premiums if volatility is high when initiating trade. Profits from potential volatility compression after establishing the position. Skew also adds value, with downside priced into options.

6. Hedge Against Market Corrections

Provides protection against moderate downturns with the long put options. Sometimes, hedges a long stock portfolio against controlled pullbacks. Offers means of profiting from or mitigating bearish scenarios.

The ability to benefit from leverage, volatility, and bearish outlooks with limited capital makes this a strategic options strategy. Skilled options traders find important advantages in ratio put spreads when implementing and managing them properly.

What are the Disadvantages of Using Ratio Put Spreads?

Ratio put spreads require precision in forecasting, managing risks, and timing volatility properly. Here are seven potential disadvantages and risks to consider when trading ratios put spreads.

Requires Market Timing Skill

Using ratio put spreads effectively requires accurately forecasting the magnitude and timing of the expected downside move in the underlying stock. The strategy is ineffective if the bearish view is overly aggressive relative to the price decline. Lack of precision in market timing sometimes leads to losses on these more complex spread positions.

Complex Risk Management

Proper position sizing must account for the imbalanced ratio between the long and short sides. Legging carefully into the spread is needed to manage early assignment risks. The short-put sides require planning proper exits if challenged by a surge higher against the directional outlook.

Unlimited Losses Possible

While maximum loss is theoretically capped, in practice, unlimited upside losses sometimes occur. This could happen if the stock rises sharply above the short put strikes. The short puts would have to be covered at great expense in a sudden upward surge.

Magnified Losses on Short Puts

The greater number of short-put contracts creates more exposure to losses on the downside. Powerful upward moves in the stock sometimes lead to substantial and magnified losses on the short-put side. This requires expertise to mitigate the downside risks.

Volatility Sometimes Hurt

Long options lose value from time decay if projected volatility increases significantly after the spread is executed. Inverted skew pricing in upside convexity also hurts. Expected time decay benefits sometimes do not materialize as planned.

Tied Up Margin Requirements

The naked short puts require margins for potentially having to buy more shares. This additional margin requirement sometimes ties up useful trading capital. It also limits the number of contracts that can be traded.

Early Assignment Risks

The short puts carry the risk of early assignment before expiration. This sometimes alters the intended risk profile of the spread position. It requires proactive management and planning around the early exercise possibility.

The complexities sometimes lead to magnified losses if not executed expertly. While offering advantages, ratio put spread also has distinct disadvantages to consider.

Is using Ratio Put Spread risky?

Yes, there are risks involved when using ratio put spreads as an options trading strategy that need to be properly managed. Ratio put spreads carry inherent risks that traders must be aware of and account for when employing this strategy. The primary risks stem from the short put leg and the leverage created from the imbalance between more long puts and fewer short puts.

When to use a Ratio Put Spread?

Ratio put spreads are most appropriate when moderate to large downward price moves are expected in the underlying asset. Their defined risk nature makes them attractive for speculating on bearish outlooks around events, volatility spikes, or technical overreactions relative to other instruments with uncapped losses.

How to set up a Call Calendar?

To establish a call calendar spread, you first choose a near-term expiration for the short call, typically less than 1 month, and a longer 3-6 month expiration for the long call. Then, determine an appropriate strike price based on the trend and forecast, often an at-the-money or slightly out-of-the-money strike with decent liquidity.

Next, buy the long-dated call to establish upside potential and sell the near-term call to generate income that offsets the long call cost. Incorporate risk management through long puts or stop-losses on the short call side. Size appropriately and target the trade’s ‘sweet spot’ around 1-2 months prior to short call expiry when its faster time decay outpaces the long call. Proper construction maximises the time decay benefits inherent in a call calendar spread.

Call calendars involve the strategic combination of a longer-dated long call and a shorter-dated short call. Careful selection of expirations and strike prices is crucial to benefit from time decay. Managing risks and understanding the “sweet spot” timing maximises the probability of success in trading calendar call spreads.

How to use Ratio Put Spread?

To set up a ratio put spread, first identify ideal bearish market conditions, then choose appropriate strike prices with the long puts 10-20% OTM and short puts at-the-money for leverage. Determine the ratio, often 2:1 or 3:2, long to short puts, legging into the trade buying long puts first to limit early assignment risk. Calculate the net debit and the maximum potential loss, and manage risk proactively using stop losses and monitoring time decay.

As the underlying declines, take profits at the target level, legging out profitable pieces first and letting short puts expire worthless for maximum gains. Proper ratio put spread construction and management allows benefiting from downward moves while defining and limiting risk.

Proper setup of ratio put spreads requires strategic strike selection, determining an optimal ratio, careful legging in, calculating net debit costs, and proactively planning risk management tactics. Ratio put spreads when used correctly, provide a profitable strategy to take advantage of mild downside expectations.

When to enter a Ratio Put Spread?

The most appropriate time to initiate ratio put spreads is when thorough analysis identifies a high probability of the underlying asset price moving lower over the selected time.

Utilising a blend of fundamental, technical and volatility analysis to determine a bearish bias with an expected downward trajectory gives the highest chance of profitability. Entering when the bias is ambiguous or mildly bearish sometimes does not produce the desired results.

Establishing the position when implied volatility is at higher relative levels provides additional edge. The elevated volatility gets priced into the short put sold, which has more potential to decline as volatility reverts lower over time.

The higher volatility also boosts the time value of the longer-dated options, enabling maximum decay as volatility decreases. This adds to the gains independent of downward price moves.

Initiating the trade just prior to binary events with an expected negative outcome for the underlying price allows for maximising the leveraged gains. For example, entering a ratio puts spread heading into an earnings report where the stock sometimes falls on poor results.

The probability of benefiting from the post-event price decline is highest when setting up the position in anticipation of the catalyst. The defined risk protects capital if the event proves to be a non-factor.

High uncertainty and fear in overall market psychology that sometimes are overdue for a relief pullback provides added opportunity. Ratio put spreads help hedge or profit from the expected volatility and downdraft.

Extreme bearish sentiment that is unsustainably stretched also offers an advantageous entry point. Reversion sometimes fuels fast profits as the exaggerated pessimism corrects.

A deterioration in fundamental data or reversal in overall technical trend that flips the bias on an asset from bullish to bearish serves as an opportune entry point.

The shifting conditions align with the directional assumption behind the ratio put spread, increasing the probability the price move plays out favourably.

The ideal scenario to initiate ratio put spreads is when bearish biases are confirmed through insights gained from rigorous analytics on market conditions, sentiment, events and data. The higher conviction overrides more marginal or speculative environments.

When to exit Ratio Put Spread?

The prediction is deemed invalid if the price of the underlying asset starts to move in the opposite direction of the bearish assumption and rises above the strike price of the short options. The upside breakeven point has not been reached, and the position should be excited to avoid incurring maximum loss.

Closing the spread as the underlying exhibits bullish momentum minimises the loss amount compared to holding until expiration. It also frees up capital for better opportunities.

Time decay will quickly deplete the position if implied volatility drops significantly, but the actual stays range is bound much above the long put strike prices. With expiration approaching, the likelihood of a profitable downward move decreases.

Exiting the spread allows salvaging the remaining premium value and redeploying that capital more effectively based on updated market views. Letting the options expire worthless results in maximum loss.

The forecast has fully played out if the trader’s downside price target is reached and the underlying price exhibits the expected decline. The ratio put spread will be deep in-the-money at or near the maximum potential profit.

Closing the spread locks in gains and eliminates further upside risk. The capital is sometimes freed up for new positions rather than left at the whims of unpredictable market movements.

Holding the ratio put spread becomes ineffective if fundamental or technical research changes the bias on the underlying asset to favour a bullish outlook. A directional change negates the premise behind initiating the bearish position.

Exiting quickly when the market narrative shifts preserve capital versus stubbornly sticking with obsolete assumptions that no longer apply. The freed-up cash sometimes plays the new bullish outlook.

Hedging Objectives Are Satisfied

For ratio put spreads used as portfolio hedges against tail risks or temporary dips, maximum gains are sometimes achieved well before expiration. The protection is no longer required if the hedge protects capital against the expected decline.

Closing the spread and realising profits as the objectives are fulfilled enables recycling the hedged capital into higher potential return opportunities rather than leaving it parked as deadweight for months.

What are the examples of Ratio Put Spread?

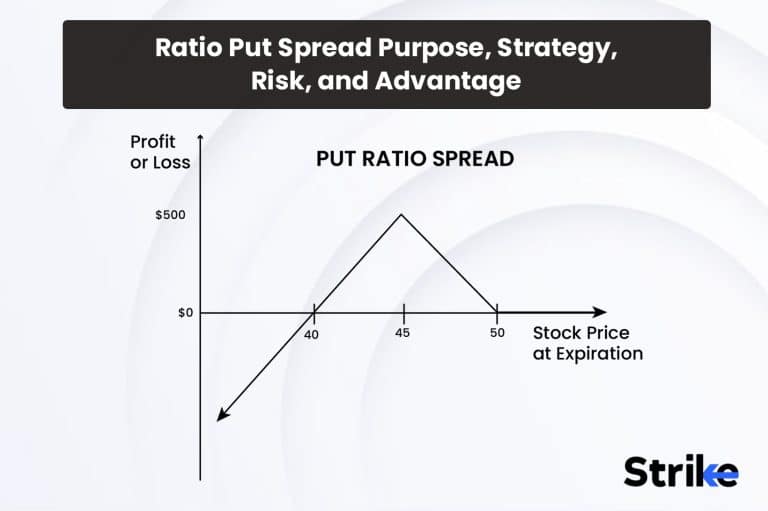

Let’s look at an example of a 2:1 ratio put spread on stock XYZ, currently trading at Rs. 50 per share. The trader opens the position in the manner described below.

– Buy 2 Sept 50 Put contracts @ Rs. 2 premium

– Sell 1 Sept 45 Put contract @ Rs. 1 premium

The net debit to open the spread is Rs. 200 per contract = (2 long puts x Rs. 2 premium) – (1 short put x Rs. 1 premium)

– Maximum Loss: Rs. 200 per contract if XYZ stays above Rs. 45 at September expiration

– Maximum Gain: Rs. 300 per contract if XYZ drops below Rs. 50 at September expiration

– Break Even Point: By September expiration, if XYZ drops to Rs. 47.50 or lower.

The trader expects XYZ stock to decline over the next month. By utilising a 2:1 ratio put spread, they acquire leveraged exposure to profit from the downtrend while strictly defining maximum loss if the forecast is incorrect.

Scenario 1 – Price Declines

The following P&L occurs if XYZ stock drops to Rs. 40 by September expiration.

– Long Rs. 50 Puts: Rs. 10 in-the-money x 2 contracts = +Rs. 1000 gain

– Short Rs. 45 Puts: Expires worthless = Rs. 0 loss

– Net Profit on Spread: +Rs. 1000 – Rs. 200 debit = +Rs. 800

The 2:1 ratio allows accumulating Rs. 1000 in intrinsic value with just Rs. 200 of capital at risk, amplifying the percentage return.

Scenario 2 – Price Rallies

The following P&L occurs if XYZ rallies to Rs. 60 by September expiration.

– Long Rs. 50 Puts: Expires worthless = Rs. 0

– Short Rs. 45 Puts: Assign -500 loss x 1 contract = -Rs. 500 loss

– Net Loss on Spread: -Rs. 200 original debit

Despite XYZ rallying 10 points, the maximum loss is capped at the original Rs. 200 debit paid. The defined risk prevented uncapped losses that shorting stock would produce.

This example demonstrates the asymmetric risk-reward profile and leverage the potential of ratio put spreads. The 2:1 structure increased profits in the bullish decline while capping and defining losses if the price rose instead.

What is the difference between Ratio Put Spread and Ratio Call Spread?

The main difference between ratio put spread and ratio call spread is that ratio put spreads have a bearish bias and profit from a decline in the underlying asset’s price. Ratio call spreads have a bullish bias and profit from the rising price. The directional assumption is the core difference between the two strategies.

With ratio put spreads, the maximum loss is capped at the net debit paid. The maximum gain is unlimited downside profit potential. For ratio call spreads, maximum profit is capped at the net credit received. Maximum loss is uncapped downside if the underlying price drops. The risk profiles are inverted.

Ratio put spreads use more long puts than short puts to benefit from leveraged gains if the price drops below the long strike.

Ratio call spreads use more short calls than long ones to benefit from leveraged gains if the price rises above the short strike. The leverage components move counter to each other.

Ratio put spreads benefit from a decline in implied volatility – the short puts sold have higher vol prices that erodes quickly as vol drops. Ratio call spreads benefit from increased implied volatility – the long calls purchased appreciate as rising vol gets priced into options.

For ratio put spreads, the trader buys puts at a higher strike price than the puts sold. This defines maximum profit if the price drops below the long strike.m For ratio call spreads, the short calls are sold at a higher strike price than the long calls bought. This defines maximum profit if the price exceeds the short call strike.

While both strategies involve uneven numbers of long vs short options for leverage, ratio put spreads and call spreads have opposing risk profiles, directional assumptions, and ideal volatility environments for profitability.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 52")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 53")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 54")

: Overview, 10 Types of Indicators, Settings for Different Markets 56")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 58")

No Comments Yet.