The ratio call spread is an options trading strategy that aims to leverage premium decay over time for potential profit. The ratio call spread helps traders sell more puts than are purchased in anticipation that time erosion of premium will provide profits, even if the underlying stock closes above the short strike on expiration.

However, the tradeoff is taking on increased risk compared to a regular spread if the market moves strongly against the position. To open a ratio put spread, an options trader simultaneously sells multiple puts at a lower strike price than puts that are purchased at a higher strike price. The ratio of short to long puts is determined by the trader’s risk tolerance and outlook. As time passes, premium on all positions declines if volatility falls or remains stable.

Profits are pocketed if this “time premium” is sufficient to offset assignment risk from an adverse stock move. However, because multiple puts are short, ratio put spreads are risky if the underlying plummets and all short puts are assigned. Careful analysis of probabilities and proper position sizing is important to manage risk prudently, with this strategy seeking to benefit from premium decay through leveraged positions.

What is a Ratio Call Spread in options trading?

A ratio call spread is an options trading strategy that involves buying and selling call options on the same underlying asset but with different strike prices and in disproportionate numbers. The goal is to profit from a large move in the underlying asset while limiting losses if the move is smaller.

The setup involves buying more call options with a lower strike price and selling fewer call options with a higher strike price. For example, a trader might buy 2 call options with a Rs. 50 strike and sell 1 call option with a Rs. 60 strike. The calls purchased outnumber the calls sold, hence the term “ratio”.

Buying more calls than are sold creates a bullish bias to the trade. The trader expects the underlying stock to rise past the higher strike price so the purchased calls become profitable. However, the sold call provides some downside protection and reduces the net cost of the trade.

The maximum loss on a ratio call spread is limited to the net premium paid. This occurs if the underlying stock stays below the lower strike at expiration. All the options expire worthless in this case.

The potential profit is uncapped to the upside if the stock rises far above the higher strike. Each purchased call gains value, while the sold call limits gains to some degree. A larger move in the stock leads to greater profits from the extra calls that were purchased.

A key advantage of a ratio call spread is the lowered cost to establish the trade. The sold call generates immediate income to help offset the debit paid for the purchased calls. This defines the maximum risk while freeing up capital for other opportunities.

The ideal conditions for a ratio call spread are when a trader expects a sizable move in the underlying asset but wants to reduce costs. Buying more calls increases leverage, while the sold call offers protection if the forecast is wrong.

Ratio call spreads sometimes use out-of-the-money, at-the-money or in-the-money options. A deeper in-the-money setup reduces the overall cost but depends on a larger move in the stock to become profitable. An out-of-the-money structure costs less but relies on a bigger rally to exceed the higher strike price.

Managing a ratio call spread sometimes involves closing the position before expiration to lock in profits or cut losses. Letting the options expire exposes the trade to stock movements through the last trading day and potentially broader bid/ask spreads.

The usage of ratio call spreads in actual transactions is demonstrated in the following instances.

- A trader buys 2 SPY Rs. 300 call options and sells 1 SPY Rs. 310 call option. Each contract controls 100 shares, so the trader is long 200 SPY calls and short 100. The net cost is Rs. 2 per share after the short call offsets some of the purchase price.

- With SPY at Rs. 320 at expiration, the purchased calls are worth Rs. 20 each for a gain of Rs. 4,000. The sold call loses Rs. 10, so the total profit is Rs. 3,000. More calls were bought than sold, so the position benefits from greater exposure to the price move.

- The Rs. 300 calls would expire worthless if SPY closed at Rs. 290. The Rs. 310 call would gain Rs. 1, resulting in a maximum loss of Rs. 200 on the trade. The defined risk allowed this trader to make an aggressive bullish trade for a low cost.

A ratio call spread involves a greater number of purchased calls relative to sold calls. The strategy benefits from upside move in the underlying asset while limiting losses. Careful selection of the strike prices helps manage costs and risks. Traders utilise ratio call spreads when they expect a sizable rally in stock but want to define their capital at risk.

What is the Purpose of Ratio Call Spreads?

The primary purpose of using a ratio call spread strategy is to establish a bullish options trade at a lower net cost while benefiting from unlimited profit potential in the event of a large upside move in the underlying stock. The strategy aims to capture significant gains if the trader’s bullish forecast is correct while strictly defining maximum risk if the stock fails to rally as expected.

Ratio call spreads accomplish this by purchasing more call option contracts than are sold. The sold calls generate immediate premium income that offsets a portion of the debit required to buy the additional calls. This lowers the overall cost of the trade compared to simply buying calls outright.

The purchased calls give the trader upside exposure and leverage if the stock price rises. Buying more calls than are sold increases this exposure significantly. The sold calls cap profits from the extra calls purchased but allow those profits to expand without limit if the stock continues marching higher.

By skewing the number of traded calls to the purchase side, ratio call spreads create leveraged profits from the long calls if the trader’s bullish thesis is proves right. The short calls simply lower the price to establish the position and do not hamper the profit potential on the upside.

In addition to lowering costs, ratio call spreads strictly define maximum risk. The most lost is the net debit paid to open the trade. This creates a very favourable risk-reward scenario. The trader enjoys uncapped profit potential at a known and fixed maximum loss amount.

Being able to risk a small amount of capital relative to the profit potential is a key reason many traders utilise ratio call spreads. The strategy offers a lot of leverage on the trader’s bullish view for a modest cash outlay.

Ratio call spreads allow traders to efficiently gain exposure to large upside moves at a low cost. Simply buying calls naked would require a much higher investment to amass the same number of contracts. The sold calls subsidise the purchase through their premiums.

Here are three instances that show how ratio call spreads are used.

- A trader expects stock XYZ to rise from Rs. 50 to Rs. 60 within 2 months. They buy 5 XYZ 50 call options at Rs. 2 and sell 2 XYZ 55 calls at Rs. 1. The net debit is Rs. 5 per share. The maximum risk is capped at Rs. 500. The bought calls are for Rs. 10 each and a Rs. 5,000 profit if XYZ reaches Rs. 60.

- A trader forecasts a surge in TSLA ahead of earnings but wants to limit their cash outlay. They implement a 10:3 ratio call spread, buying 10 of the Rs. 100 calls while shorting 3 of the Rs. 110 calls. The structure benefits from a big TSLA rally with fixed and low capital risk.

- A speculator who expects a short squeeze in a heavily shorted small-cap stock uses a ratio call spread to capture a potential explosive upside move while defining their loss. The strategy offers directional exposure while freeing up capital for other opportunities.

Ratio call spreads provide leveraged upside exposure at a fraction of the cost of buying naked calls. They allow traders to risk less capital while benefiting from potentially huge gains if their bullish forecast proves correct. Selling fewer calls than purchased caps risks and subsidises the trade through the short call premiums. Ratio call spreads accomplish their purpose when markets experience explosive upside moves.

What is the basic structure of a Ratio Call Spread?

A ratio call spread is an options trading strategy that involves the simultaneous purchase and sale of unequal numbers of call option contracts on the same underlying stock. The “ratio” refers to the imbalance between the number of calls bought at one strike versus the number of calls sold at a different strike.

A ratio call spread’s fundamental composition often consists of the following.

1.Long Call Contracts

- The trader buys to open a number of call option contracts at a lower strike price. This is the long call leg.

- The goal is for the stock to rise above this strike so these calls become profitable.

- The purchased calls have unlimited profit potential as the stock price rises.

2. Short Call Contracts

- The trader sells to open more call contracts at a higher strike price. This is the short call leg.

- The goal is for these short calls to expire worthless or be closed at a lower price later.

- The premium collected from the short calls helps fund the long-call purchases.

3. Uneven Contracts

- More short calls are sold than long calls purchased, creating the uneven ratio.

- Common ratios are 1×2, 1×3, 2×3. For example, 1 long call and 2 or 3 short calls.

- The higher the ratio, the lower the net debit and the greater the leverage.

4. Net Debit

- The total premium paid for the long calls will exceed the premium collected from the short calls.

- But, the imbalance lowers the net debit cost to establish the spread position.

- The maximum loss is limited to the net debit paid if the stock falls below the strike.

5. Same Expiration

- All the calls in the spread have the same expiration month, so they align.

- This defines the fixed period of time the position will be open.

- Shorter expirations are common for greater time decay effects.

6. Strike Selection

- The long strike is chosen below the current stock price.

- The short strike is above the current price, so the calls have no intrinsic value.

- The spread between the strikes helps limit the net debit.

7. Risk Profile

- The maximum loss if the stock drops is the net debit paid.

- Breakeven is the long strike plus net debit.

- Unlimited profit potential exists if the stock rises substantially.

The ratio call spread offers a leveraged long position similar to owning the stock but with a lower break-even point resulting from the short call premium helping fund the trade. The uneven number of contracts at different strikes provides leverage.

After establishing the position, the trader aims to manage the spread as the stock fluctuates actively, adjusting to lock in profits or reduce risk. The following are basic management strategies.

- Closing the entire spread to capture profits if the stock rises quickly.

- Buying back the short calls individually at a lower price as they go in-the-money.

- Rolling the short calls outward in time or to higher strikes to avoid assignment risk.

- Widening the strikes if the stock declines and the outlook changes.

- Closing the whole spread at a loss if the stock drops below breakeven.

The basic structure of a ratio call spread involves buying fewer lower-strike calls and selling more higher-strike calls at a discounted net debit. The imbalance provides leveraged upside exposure above the long strike with capped downside risk defined by the net debit paid. Active management of the moving parts is required to optimise results. Ratio call spreads provide an effective approach to bet on upward momentum in the underlying stock when constructed appropriately for the forecast.

What are the key components of a Ratio Call Spread?

A ratio call spread has several integral components that create the structure and define its risk-reward profile. The following are the essential components.

1.Long Call Leg

- The ratio call spread involves purchasing call options to establish a bullish position. This constitutes the long call leg of the trade.

- More calls are bought than sold. For example, a 2:1 ratio involves long 2 calls for every 1 short call.

- The long calls have a lower strike price than the short calls. This creates leverage to the upside above the higher strike.

- Buying more calls increases exposure to gains if the stock rallies as expected. This defines the profit potential.

2. Short Call Leg

- Short calls are sold to generate income and offset the cost of the long leg. Less calls are sold than bought.

- The short calls have a higher strike price than the long calls. This defines the maximum profit zone.

- Selling calls lowers the net debit and caps the potential loss if the trade loses money.

3. Disproportionate Contracts

- Having more long contracts than short is what defines a ratio spread. Common ratios are 2:1, 3:2, or 5:3.

- The greater the imbalance between longs and shorts, the more leverage is created through the extra-long calls.

4. Different Strike Prices

- The long and short legs utilise different strike prices. The longs are lower than the shorts.

- The spread between the strikes determines the maximum profit potential if the stock rises past the short strike.

- Wider spreads mean higher potential profit but also increase the net debit.

5. Net Debit to Open

- After selling the short calls, there is generally still a net debit to open the trade.

- This net debit amount defines the maximum risk on the trade since losses cannot exceed it.

- The higher the net debit, the higher the profit potential in exchange for increased risk.

6. Capped Downside Risk

- Downside risk on the trade is strictly limited to the net debit paid when establishing the position.

- Both call legs expire worthless, and the net debit defines the loss if the stock drops below the long strike.

- Selling short calls ensures the defined maximum loss – the trader cannot lose more than the net cost.

7. Uncapped Upside Potential

- The long calls gain value if the stock rallies above the short call strike, and profits are uncapped.

- The brief calls simply reduce cost – they do not restrict potential profits on the upside.

- More aggressive ratios create greater upside exposure through the imbalance of extra longs.

The critical components of a ratio call spread work symbiotically to create a leveraged bullish strategy with defined risk parameters. Carefully selecting the ratio, strikes, and net debit amount allows traders to fine-tune the risk-reward profile based on market conditions and assumptions.

How does Ratio Call Spread work?

A ratio call spread utilises a combination of purchasing more call option contracts that are sold to create leveraged profits with limited risk. Here is an overview of how the strategy functions.

1.Establishing the Trade

- The trader gets a more significant number of call options than they sell short. For example, buying 4 calls and selling 2 calls.

- The calls purchased are at a lower strike price than the calls sold short. For example, long 4 XYZ 50 calls and short 2 XYZ 55 calls.

- Net debit is paid to open the trade after offsetting the short-call premiums. This defines maximum risk.

- The potential profit on the spread equals the difference between the long and short strikes minus the net debit paid.

2. Leverage from Extra Long Calls

- Having more long calls than shorts provides greater exposure to upside profits if the stock rallies.

- The additional long contracts increase leverage and amplify gains above the higher short strike.

- The short calls simply reduce the net cost and cap risk, they do not limit potential profit.

- Wider ratios like 5:2 or 10:3 create more leverage through the imbalance between longs and shorts.

3. Capped Downside Risk

- Maximum loss on the trade is strictly limited to the net debit paid when opening the position.

- The calls expire worthless, and the net debit is lost if the stock closes lower than the long strike at expiry.

- Selling shorter-dated calls with the same or higher strike as the longs definitively caps the potential loss.

- Defined downside risk allows a leveraged bullish trade without exposing the trader to uncapped losses.

4. Managing Early for Profit

- As the underlying stock rallies, the long calls gain intrinsic value while the shorts lag.

- The trader sells the profitable longs and captures the gains prior to expiration if a target profit is reached.

- Managing the upside early allows the trader to lock in profits and avoid early assignments on the short calls.

5. Impact of Time Decay

- Time decay negatively impacts the long calls more significantly since there are more of them.

- The time value erosion of the short calls works in the trader’s favour.

- Monitoring time decay and actively managing around expirations is key to maximising profits.

Ratio call spreads work through the imbalance of more purchased calls than sold calls. This provides greater upside exposure at a defined maximum risk. The limited downside and leveraged upside make ratio call spreads an attractive strategy when forecasting a big rally in an underlying stock.

What is the strategy of Ratio Call Spread?

A ratio call spread is an options trading strategy designed to profit from a strong upside move in the underlying stock while strictly limiting downside risk. The strategy aims to maximise leverage and optimise the risk-reward profile.

The trader buys more call option contracts than they sell at different strike prices to create disproportionate upside exposure. For example, going long 5 calls at the Rs. 50 strike while shorting 2 calls at the Rs. 60 strike.

More calls are purchased than sold to increase the leverage if the stock rallies past the higher strike. This expands profit potential while the sold calls simply help reduce the net cost of the trade.

The goal is to benefit from unlimited upside if the stock makes a large move higher while defining max loss on the trade if it does not. The defined downside risk creates a favourable asymmetric payoff profile.

Traders utilise ratio call spreads when they have a strongly bullish forecast but want to implement the trade at a lower net cost. The short calls generate premium income to offset the price of the extra-long calls.

Ratio call spreads allow traders to efficiently establish leveraged upside exposure for a fraction of the capital required to purchase naked calls. This frees up capital for other opportunities.

The strategy gives traders expanded upside potential without requiring a large directional move in the stock. Smaller incremental gains sometimes become amplified by the additional long call options.

Proper strike selection is key to implementing the strategy effectively. The spread between the long and short strikes helps determine the overall risk profile. Wider spreads increase leverage but also raise the cost of establishing the trade.

Managing the position around expiration at 50% or greater of maximum profit allows traders to capture sizable gains while avoiding the time decay and volatility crush that sometimes hit into expiration week.

The ratio call spread strategy works best when high implied volatility provides richer option premiums. Higher IV raises the value of the short calls, increasing the income used to offset the longs.

How does volatility impact the effectiveness of a Ratio Call Spread?

Volatility is a major factor influencing the profit potential and probability of success when using ratio call spreads. Higher implied volatility in the options tends to benefit the strategy, while low volatility reduces its effectiveness.

Higher IV increases the value of both the purchased calls and the sold calls. However, since more calls are bought than sold, the long leg gains more value than the short leg loses. This dynamic works in favour of the ratio spread.

The additional premium income from the short calls in a high IV environment further subsidises the cost of the extra long calls. This allows establishing a greater upside exposure at a lower net debit.

With elevated IV, the range of potential outcomes for the underlying stock increases compared to low volatility conditions. This expanded range provides greater profit potential for the leveraged long call ratio spread.

Since ratio call spreads have defined, capped risk, inflated IV from the short calls does not negatively impact the max loss. Higher IV allows capturing greater upside at the same fixed risk point.

Low IV has the opposite effect on ratio spreads, reducing their advantage. With minimal extrinsic value, the short call premiums decline. This provides less income to offset the cost of the extended leg.

The overall debt paid is usually higher in low-volatility environments, reducing the leverage capacity of the trade. The risk-reward profile deteriorates as cost rises and the range of outcomes narrows.

Since the short calls have little time value to erode, they offer minimal protection against early unfavourable stock moves. The leverage from the extra longs is muted.

In low IV conditions, other strategies, like buying calls outright, sometimes provide better exposure to the upside. The benefits of the ratio structure are reduced without volatility expansion.

To maximise success with ratio call spreads, traders should implement them when implied volatility is stretched to the higher end of its historical range. This ensures sufficient risk-reward to justify the leverage created from the extra-long calls.

Monitoring changes in IV once in the trade allows the trader to manage early or roll the position as needed. For example, buying back short calls when IV plummets helps maximise profits.

What are the advantages of using Ratio Call Spread?

Ratio call spreads give traders the following seven important benefits, among others.

1.Leveraged Profit Potential

- Buying more calls than selling provides greater exposure to upside gains if the stock rallies.

- The extra-long calls act as profit multipliers above the short-call strike price.

- Aggressive ratios like 5:2 maximise the leverage potential from the imbalance of longs.

2. Lower Cost Structure

- Selling calls against the extra longs generates premium income to reduce the net debit.

- The short calls subsidise the increased leverage created by the additional longs.

- A lower net cost allows for efficiently establishing a leveraged bullish options position.

3. Strictly Defined Risk

- Maximum loss is strictly limited to the net debit paid when opening the trade.

- Selling short calls with the same or higher strike caps the downside risk.

- The upside is uncapped while the downside is fixed – creating an asymmetric risk profile.

4. Capital Efficiency

- The defined and limited risk allows capital to be deployed more efficiently.

- Compared to buying naked calls, less cash is tied up for the same directional exposure.

- The remaining money is sometimes used for other trades rather than tied up in margin requirements.

5. Expanded Range of Profitability

- The extra leverage from the long calls allows smaller, incremental gains in the stock to become profitable.

- Wider upside breakeven points mean the trade is good without substantial stock movements.

- Less reliance on major price appreciation to turn a profit.

6. Management Flexibility

- Ratio spreads allow for active management to lock in profits or reduce losses.

- Traders sometimes close positions early if the stock is surging to avoid upside risks.

- Investors sometimes bring back short calls to prevent further losses if the stock drops.

7. Higher Probability of Success

- The short leg helps fund the trade while also reducing the breakeven point.

- Requires a smaller stock move to profit compared to buying calls outright.

- Defined downside risk increases the odds of gain relative to potential loss.

Ratio call spreads efficiently provide leveraged upside exposure while capping risk. For traders with a moderately to strongly bullish outlook, ratio call spreads present an advantageous strategy to implement that exposure at a low cost. The imbalance of more longs than shorts unlocks additional profit potential.

What are the Disadvantages of using Ratio Call Spreads?

Ratio call spreads offer several appealing qualities, but there are seven negative aspects and issues to take into account, including the following.

1.Greater Loss Potential

- While max loss is capped, the greater number of long calls means the potential loss amount is higher.

- The net debit to open the trade sometimes is substantial depending on the strikes and ratio used.

- A larger loss amount requires a higher degree of confidence in the bullish forecast.

2. Increased Complexity

- Determining the optimal ratio, strikes, and technical structure requires thorough analysis.

- Requires understanding of leverage implications and balance of risk versus reward.

- Complexity sometimes provides unanticipated hazards and outcomes if improperly designed.

3. Exposure to Rapid Time Decay

- Time value erosion accelerates on the long calls as expiration approaches.

- The multiplying impact of time decay on the additional longs sometimes rapidly negates their leverage potential.

- Requires close monitoring and management around expirations.

4. Potential for Unlimited Losses

- While maximum loss is set at initiation, early assignment on short calls could expose traders to greater losses if the stock declines rapidly.

- Failure to properly monitor and manage assignments leads to cascading losses.

5. Larger Bid/Ask Spreads

- The less liquid nature of ratio spreads often results in wider bid/ask spreads.

- This increased friction elevates closing costs and negatively impacts overall profitability.

6. Requires Accurate Forecast

- Realising the maximum gains relies on the stock moving above the higher strike price before expiration.

- An incorrect forecast on direction, timing, or magnitude means the trader accrues losses.

- Inability to benefit from leverage if the price action does not align with assumptions.

7. Prematurely Capped Profits

- The short calls cap upside potential profits if the stock continues rising past the higher strike.

- Sometimes, they sacrifice substantial additional gains by having sold call options prematurely.

While ratio call spreads offer leverage, they also come with increased complexity, require precision in forecasting, are vulnerable to time decay, and involve capping potential profits from a significant upside move. Weighing these disadvantages against the advantages allows traders to determine if and when ratio call spreads to align with their trading plan, outlook, and risk preferences.

What’s the potential loss scenario in a Ratio Call Spread?

The maximum loss on a ratio call spread is strictly defined and limited to the net debit paid when establishing the trade. The loss is capped due to the short call leg, which offers downside protection.

For example, a trader buys 3 SPY 350 calls for Rs. 2 and sells 1 SPY 360 call for Rs. 1. The net debit to open the trade is Rs. 5 per share, or Rs. 500 total, given the standard contract size.

The maximum loss would occur if SPY expires below 350 at expiration. In this case, all the 350 calls expire worthless. The 360 short call would also expire worthless, meaning the trader loses the entire Rs. 500 debit paid upfront.

The short 360 call ensures the trade has defined risk. Regardless of how low SPY goes, the most the trader sometimes loses is their net debit. The short call limits and caps the downside exposure.

Maximum loss occurs whenever SPY is below the long call strike at expiration. For example, if SPY is at 340, the outcome is still a Rs. 500 loss, which was specified and fixed at the start of the deal.

Early assignment of the short call could technically lead to further losses. The trader would be required to purchase shares at a price that was Rs. 10 greater than the existing value if SPY rose over 360.

However, buying back the short call at the time of assignment caps this risk. Careful monitoring and management prevent uncontrolled losses due to early exercise.

While maximum loss is known, it does become greater in absolute terms the more calls bought relative to sold. For example, a 10:3 ratio spread has a higher max loss amount than a 2:1 ratio spread.

The wider the spread between the long and short strikes, the greater the debit paid upfront. Wider spreads increase leverage but also increase potential maximum loss.

The loss scenario is mitigated by selling shorter-dated calls at the same or higher strike as the long calls. This definitively caps risk close to expiration.

When to use a Ratio Call Spread?

Here is an overview of when it is appropriate to use a ratio call spread strategy.

1.Bullish Outlook with Specific Price Target

Ratio call spreads enable profiting from the upward advance while tightly defining risk when a trader has an optimistic prediction with a definite upward price objective for the stock. The added leverage amplifies gains within the defined maximum profit zone.

2. Expecting a Short Squeeze

During potential short squeeze conditions, ratio call spreads allow traders to benefit from a massive, uncontrolled upside spike while limiting the downside if the squeeze fails to materialise.

3. Increased Volatility Ahead of Earnings

Ratio call spreads enable profiting from pricey option premiums when implied volatility increases ahead of an earnings event. The short calls are sometimes sold at inflated values to offset the longs.

4. Moderately Bullish Outlook

Ratio call spreads offer an effective approach to executing a directional options strategy when a trader is mildly positive. Less capital is put at risk for a given amount of upside exposure.

5. Unwillingness to Risk Large Amounts

Traders who want to minimise their cash exposure but retain upside leverage sometimes define risk and provide upside exposure on a limited budget using a spread ratio.

6. Slightly Bullish Outlook Needing Leverage

The additional long calls in a ratio spread give enhanced returns when a trader has a modest bullish bias but requires leverage to make a significant profit.

7. Trading Small Accounts

Ratio call spreads allow smaller account sizes to implement leveraged options trades while minimising the impact of trading capital tied up in one position.

8. Capitalising on High Implied Volatility

Periods of excessively high IV are sometimes capitalised on using ratio call spreads. Short calls generate larger premiums to subsidise the long calls when IV is inflated.

9. Danger of Extended Stock Declines

Ratio call spreads provide upside potential while limiting losses in a larger-than-anticipated negative stock move.

10. Momentum Expected to Continue

Ratio call spreads enable leveraged exposure to a more sustained upside when it is believed that upward momentum will continue. Gains sometimes compound as momentum builds.

Ratio call spreads align well with moderately to strongly bullish forecasts where leverage is desired to enhance upside profits while strictly limiting the downside risk. The ability to maximise gains and minimise losses in volatile conditions makes ratio call spreads a versatile strategy.

How to set up a Call Calendar?

A call calendar spread, also known as a time spread, involves buying a short-term call option and selling a longer-term one on the same underlying stock. The steps to set up this technique are as follows.

1. Identify a suitable stock and forecast its movement over a specific timeframe. The strategy benefits from a store expected to rise moderately in the near-term but remain flat or fall later.

2. Choose two call option expiration dates that align with the forecasted movement. For example, buy a call expiring in 1 month and sell a call expiring in 3 months.

3. Select strike prices for the two calls. Typically, both are at-the-money or very close to the current stock price. More immediate strikes maximise time decay differences.

4. Buy the shorter-term call to establish a bullish position and capture gains if the stock rises as expected in the near term.

5. Sell the longer-dated call to generate income to offset the cost of the purchased call. The sold premium creates a credit.

6. Structure the trade for a net credit. The short call’s time value yield should fully fund the purchased call debit. No cash outlay is ideal.

7. Determine proper contract sizing for the two legs. Most often, a 1:1 ratio is used, buying 1 call and selling 1 call at each strike.

8. Place the trade by buying the short-term call and simultaneously selling the longer-term call. Managing as a package locks in the spread.

9. Calculate maximum profit and loss. Max profit is capped at the net credit amount. Max loss is the strike price difference minus credit.

10. Actively manage the position as the stock moves and as expiration approaches. Buy back short calls early to lock in gains.

11. Close the position before the shorter-term call expires to avoid assignment risk. Calendar spreads are intended to capture time decay, not direction.

12. Time the entry properly when volatility is maximised so sufficient time premium exists to fund the purchased call.

Call calendar spreads allow benefiting from short-term stock gains and time decay. The short call funds the long call purchase for a built-in hedge. Careful adherence to the structure, management, and objectives is key to successfully utilising this strategy.

How to use Ratio Call Spread?

Here is a step-by-step guide on how to use a ratio call spread.

1. Identify a stock with a bullish outlook and forecast the magnitude and timing of the expected uptrend. Ratio call spreads benefit from strong, sustained upside momentum.

2. Choose the ratio of long calls to short calls depending on the bullishness of the forecast and desired leverage. More aggressive ratios like 5:2 provide greater upside exposure.

3. Select the strike prices for the long and short legs. Longer-dated at-the-money strikes balance risk, reward, and cost considerations.

4. Buy the desired lower strike call options to establish the bullish long leg. This forms the basis of the position’s upside exposure.

5. Sell fewer higher strike calls to generate premium income that will offset a portion of the long call debit.

6. Calculate the net debit or credit for the trade. A net debit is typical for ratio call spreads. This defines maximum loss.

7. Determine the maximum profit potential above the short call strike based on the spread width and net debit amount. Wider spreads increase profit potential.

8. Evaluate the leverage created on the upside through the imbalance between the long and short legs. Ensure the leverage aligns with the forecast.

9. Monitor the position as it moves toward expiration. Manage early to lock in profits or reduce losses based on the stock’s price trend.

10. Close the spread once before expiration to avoid assignment risks on the short calls. Capture profits and avoid unwanted stock ownership.

11. Analyse stock performance compared to the initial forecast. Assess decisions regarding ratio, strikes, and timing to improve future trades.

12. Look for opportunities to use ratio call spreads when forecasting similar bullish conditions, high implied volatility, or expectations for a short squeeze.

13. Consider managing the upside exposure intraday if a forecasted breakout occurs rapidly. Buy back short calls to capture full profits from the longs.

14. Evaluate adjusting the position if the forecast changes. For example, buying back the shorts and closing the longs to avoid further losses.

15. Pay close attention to earnings dates and be prepared to close positions early before announcements to limit risks from volatility expansion.

Properly using ratio call spreads requires forecast analysis, strategic position sizing, active management, thoughtful adjustments, and learning from results to improve future trading outcomes when utilising this leveraged strategy.

How to Adjust a Ratio Call Spread?

Ratio call spreads allow for several adjustments to manage the trade or alter its risk-reward profile as market conditions change. The following are examples of common alterations.

Buy back the short calls: This removes the capped upside potential to allow the long calls to realise full profits. Doing so converts the position to straight, long calls.

Sell additional short calls: Adds more income from premiums to further reduce cost based on the trade. It also additionally caps the upside.

Roll up the short calls: To avoid assignment risk, roll the shorts to a higher strike if the stock price rises near the short strike. Pushes cap on profits higher.

Roll out the long calls: Purchasing longer-dated calls reduces time decay exposure on the long leg while maintaining upside exposure.

Adjust the call ratio: Buy more long calls to increase leverage or close some longs to reduce cost and risk exposure if the forecast changes.

Leg into call spreads: Turn long calls into call spreads to lock in some gains and reduce directional exposure.

Leg into straddles/strangles: Combine additional long puts or put spreads to create long straddles or strangles if expecting greater volatility.

Take profits on winning legs: Sometimes, sell the spread in pieces; selling winning legs while keeping losing legs open saves on commissions versus closing the entire spread.

Stop loss orders: Set stop loss orders on ratio call spreads to limit losses if the stock drops below a defined price threshold.

Hedge with put options: Buying puts or spreads creates downside protection against an adverse stock move while maintaining the call ratio position.

Collar the position: Fund buying puts protection on the trade by selling covered calls against the long stock position if assigned on the calls.

The ability to adjust and modify ratio call spreads allows for managing risk and reward as the stock price trends and as expiration approaches. Traders use these adaptive techniques to maximise profitable outcomes.

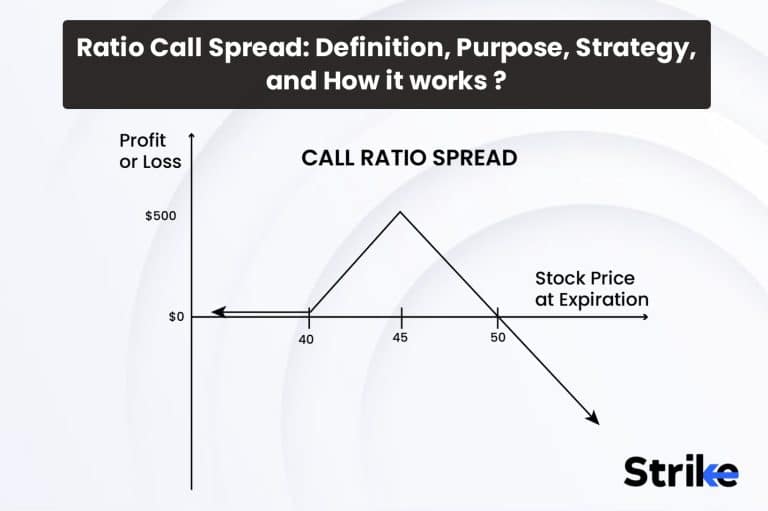

What are the examples of Ratio Call Spread?

Let’s assume a trader has a bullish forecast on hypothetical stock XYZ, currently trading at Rs. 50 per share. The trader expects XYZ may rise to Rs. 55-Rs. 60 range over the next 2 months.

To benefit from the upside potential while limiting risks, the trader implements a 5:3 ratio call spread on XYZ.

- Buy 5 XYZ 50 call option contracts

- Sell 3 XYZ 55 call option contracts

With the stock at Rs. 50, the trader buys 5 of the 50 strike call options at a price of Rs. 2.00 per contract. Each contract covers 100 shares, so this leg costs Rs. 1,000 (5 contracts x 100 shares per contract x Rs. 2.00 premium per share).

To offset part of the cost, the trader simultaneously sells 3 of the 55 strike calls at a price of Rs. 1.00 per contract. This leg brings in Rs. 300 in income (3 contracts x 100 shares x Rs. 1.00 premium).

The net debit to open the entire ratio call spread is, therefore, Rs. 700 (Rs. 1000 paid for long calls minus Rs. 300 received from short calls). This represents the maximum potential loss on the trade if XYZ finishes below 50 at expiration.

The break-even point is the lower strike of 50 plus the net debit of 0.70, or Rs. 50.70. Any share price above that at expiration results in a profit.

The maximum profit is uncapped on the upside above the higher short strike of 55. At any price above 55, the 5 long 50 calls gain value, while the 3 short 55 calls offset some of those gains.

For example, if XYZ rises to Rs. 60 at expiration, the long 50 calls are worth Rs. 10 each for a total value of Rs. 5,000 (5 contracts x 100 shares x Rs. 10). The short 55 calls lose Rs. 5 each, or Rs. 1,500 (3 contracts x 100 shares x Rs. 5). That’s a net profit of Rs. 3,500 on the spread (Rs. 5,000 – Rs. 1,500).

When to enter a Ratio Call Spread?

Traders find ratio call spreads attractive options trading vehicles in certain market conditions when used properly. Here are nine key considerations around when to potentially enter a ratio call spread.

Bullish Outlook: Since ratio call spreads have unlimited profit potential to the upside, they are best suited when moderately bullish on the underlying stock over the options expiration period. The long calls benefit from rising prices.

Expected Price Swing: A significant anticipated upside price swing or breakout provides the ideal environment for a ratio call spread. The leverage amplifies profits from the rally. There is a minimal cost to participate via the small debit.

Increase in Volatility: Increasing call premiums enhance the spread’s leverage potential and risk/reward ratio if you anticipate both an increase in stock price and a rise in volatility.

Momentum: Following a bullish technical breakout with increasing upside momentum and strong trends makes ratio call spreads more appealing to continue benefiting from the emerging move.

Portfolio Hedging: It is sometimes structured to provide partial portfolio hedging while retaining upside exposure. Short calls generate income to offset long risks.

Speculation: The leveraged structure with capped downside risk allows speculation on upside momentum. Small net debit provides attractive risk/return for aggressive bullish views.

Capital Efficiency: The uneven leg ratio requires less capital outlay than other bullish structures to establish the position, freeing the margin for other potential uses.

Risk Management: Ratio call spreads allow managing and defining maximum loss. Loss is capped at the net debit paid if wrong, unlike naked call strategies.

Affordability: The shorter-term structure with potential small net debit provides an appealing risk/return profile even for smaller accounts.

The trader must ensure proper construction, management, and alignment with their market outlook and risk tolerance when assessing entry timing. The key is balancing the desire for leveraged upside exposure against prudent risk control. Ratio call spreads sometimes efficiently enhance profits but creates substantial risk if used improperly.

When to exit Ratio Call Spread?

Here is an overview of ten common scenarios for when a trader looks to exit a ratio call spread position.

Cut Losses: Exiting the spread at a loss helps prevent further losses if the underlying stock drops below the long call strike. The maximum loss is the net debit paid, but covering at an opportune time reduces this.

Long Calls Profitable: The purchased calls obtain intrinsic value if the stock rallies above the long call strike. Locking those profits is allowed by closing the long call side if substantial.

Short Calls Tested: As stock rises, short calls move deeper in-the-money with higher assignment risk. Exiting the short calls via buyback or roll reduces this risk.

Max Profit Achieved: Much potential profit is probably realised if the stock soars well beyond the short call strikes before expiration. Closing the spread at this point is prudent.

Rising Volatility: An increase in volatility that boosts call premiums across the curve sometimes presents an opportunity to exit at an advantageous price, capturing time value.

Changing Outlook: The trader sometimes finds it sensible to exit the bullish spread structure if their market outlook shifts and they become less bullish on the stock. Protect capital.

Time Decay Effects: Utilising short-dated options sometimes causes substantial time value deterioration to occur rapidly. Exiting to capture the remaining time premium is sometimes beneficial.

Liquidity Changes: Reduced liquidity that widens bid-ask spreads on the options impacts exit costs and should prompt potential early exit.

Opportunity Cost: Closing the current spread frees up capital to pursue those other trades instead if more attractive options and trade opportunities arise.

Excess Unrealized Losses: Exiting curtails further unrealized losses and frees margin to deploy elsewhere if a loss threshold is reached.

Proper trade management entails planning exit strategies for various scenarios before establishing the ratio call spread position. Actively monitoring the moving parts of the spread and market conditions allows the trader to implement appropriate exits at opportune times.

Is using Ratio Call Spread risky?

Yes, using ratio call spreads does entail notable risks that traders should fully understand and account for.

While ratio call spreads provide leveraged upside potential, the uneven leg structure creates imbalanced risk exposures that must be prudently managed.

The primary risks include the following.

Leverage Risk: The same amplified leverage boosting potential gains on the upside also exaggerates losses on the downside. The losses sometimes mount rapidly if the forecast is wrong.

Assignment Risk: Short calls that go deep in-the-money before expiration face higher odds of early assignment. This sometimes forces stock purchase at an undesirable price and time. Requires close monitoring.

Unlimited Downside: Though maximum loss is technically capped at the debit paid, the imbalance poses an unlimited risk if the stock were to crash below the long strikes.

Bid-Ask Spread Costs: Entering and exiting the multi-leg spread incurs wider bid-ask spreads, immediately reducing profit potential.

Complex Structure: The added intricacy of the uneven legs increases the chances of construction or management errors that are sometimes costly.

Proper position sizing is vital to limit the risks posed by the leverage. Prudent strike selection and spread width also help contain the downside. Ongoing active management of the moving parts further aids risk reduction.

What is the difference between Ratio Call Spread and Call Ratio Backspread?

The following are the primary variations between call ratio backspreads and ratio call spreads.

Construction

- Ratio Call Spread: Involves buying a smaller number of call options at one strike and selling a larger number of calls at a higher strike. Creates a net debit position.

- Call Ratio Backspread: Involves selling a smaller number of call options at one strike and buying a larger number of calls at a higher strike. Creates a net credit position.

Risk Profile

- Ratio Call Spread: Capped downside risk with uncapped upside profit potential. Maximum loss if stock drops below long strike.

- Call Ratio Backspread: Capped upside profit potential with technically uncapped downside risk. Maximum loss if stock surges above short strike.

Bias

- Ratio Call Spread: Bullish bias, benefits from increased underlying stock price. Looking to profit from an upside move.

- Call Ratio Backspread: Bearish bias, benefits from decline or sideways move in stock. Looking for short calls to expire worthless.

Leg Ratio

- Ratio Call Spread: Typically sell more calls than bought. Common ratios like 1×2, 1×3, 2×3.

- Call Ratio Backspread: Buy more calls than sold. Common ratios like 3×2, 2×1.

Net Cost

- Ratio Call Spread: Net debit is required to open the spread position.

- Call Ratio Backspread: Net credit received to open the spread position.

While both strategies involve uneven call option legs, ratio call spreads and call ratio back spreads have opposite risk profiles and bias directions. Ratio spreads are net debit bullish trades, while ratio back spreads are net credit bearish trades. These structural differences make them distinct options strategies.

What is the difference between Ratio Call Spread and Put Ratio Backspread?

The main variations between a ratio call spread and a ratio back spread are listed below.

Position Type

- Ratio Call Spread: Uses only call options to create a net debit bullish position.

- Put Ratio Backspread: Uses only put options to create a net credit bearish position.

Maximum Profit

- Ratio Call Spread: Unlimited profit potential if the stock rises substantially.

- Put Ratio Backspread: Capped maximum profit if the stock declines below short put strike.

Maximum Loss

- Ratio Call Spread: Capped maximum loss at the net debit paid.

- Put Ratio Backspread: Uncapped losses if stock surges above long put strike.

Leg Construction

- Ratio Call Spread: Buys fewer lower strike calls and sells more higher strike calls.

- Put Ratio Backspread: Sells fewer higher strike puts and buys more lower strike puts.

Optimal Market Outlook

- Ratio Call Spread: Benefits from increase in underlying stock price.

- Put Ratio Backspread: Benefits from a decline or sideways move in stock price.

Assignment Risk

- Ratio Call Spread: Early assignment risks on short call leg if the stock rises.

- Put Ratio Backspread: Early assignment risks on the short put leg if the stock falls.

Management

- Ratio Call Spread: Actively manage short calls to avoid assignment if tested.

- Put Ratio Backspread: Actively manage short puts to avoid assignment if tested.

Ratio call spreads use call options to profit from an upside move, while put ratio backspreads use put options to profit from a downside move. Their opposing constructions, biases, and risk profiles make them distinct strategies.

What is the difference between Ratio Call Spread and Vertical Spread?

The main distinctions between a ratio call spread and a vertical call spread are listed below.

Leg Ratio

- Ratio Call Spread: Uneven number of long calls vs short calls. Typically, they sell more calls than buy.

- Vertical Call Spread: Equal number of long and short call contracts. Typically 1×1 or 2×2 ratio.

Maximum Loss

- Ratio Call Spread: Capped maximum loss at the net debit paid.

- Vertical Call Spread: Capped maximum loss at the net debit paid.

Maximum Profit

- Ratio Call Spread: Unlimited profit potential if the stock rises substantially.

- Vertical Call Spread: Capped maximum profit between strike prices less net debit.

Risk Profile

- Ratio Call Spread: Downside protected but unlimited profit upside.

- Vertical Call Spread: Defined maximum risk and maximum profit.

Position Bias

- Ratio Call Spread: Bullish bias, benefits from increase in stock price.

- Vertical Call Spread: Directional bias depends on strike selection. Sometimes, the structure is neutral to bullish.

Assignment Risk

- Ratio Call Spread: Elevated early assignment risk on short calls if the stock rises.

- Vertical Call Spread: Assignment risks balanced between legs.

Cost

- Ratio Call Spread: Credit from extra shorts lowers net debit costs.

- Vertical Call Spread: Typically wider net debit due to equal legs.

Management

- Ratio Call Spread: Requires active management of uneven legs.

- Vertical Call Spread: Simpler structure to manage.

Ratio call spreads have uneven legs providing leveraged upside exposure, whereas vertical call spreads have equal legs for defined risk. Ratio spreads require more active management but are sometimes structured at a lower net cost.

Previous Article

Previous Article

25")

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 28")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 29")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 30")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 34")

No Comments Yet.