Short Call Butterfly: Overview, Example, Uses, Trading Guide, P&L, Risks

Short Call Butterfly represents a neutral options strategy combining short and long calls in a 1-2-1 ratio. Short Call Butterfly profits from volatile market moves above or below a central strike price, with historical success rates of 45-55% in trending markets.

Market makers originated this strategy in the 1970s to capitalize on options mispricing. The position consists of buying one call at a lower strike, selling two calls at a middle strike, and buying one call at a higher strike, all with equal strike price distances.

Professional traders execute this strategy primarily in high implied volatility environments above the 75th percentile. Maximum profit occurs at expiration with the underlying price significantly above or below the middle strike. Break-even points exist at prices equal to the middle strike plus or minus the net premium received.

Position management data indicates rolling opportunities emerge at 21 days to expiration. Risk metrics show theta values peak at 15-20 days remaining. Historical backtests reveal 65% of profitable trades reach 50% of maximum gain within 12 days.

What is a Short Call Butterfly?

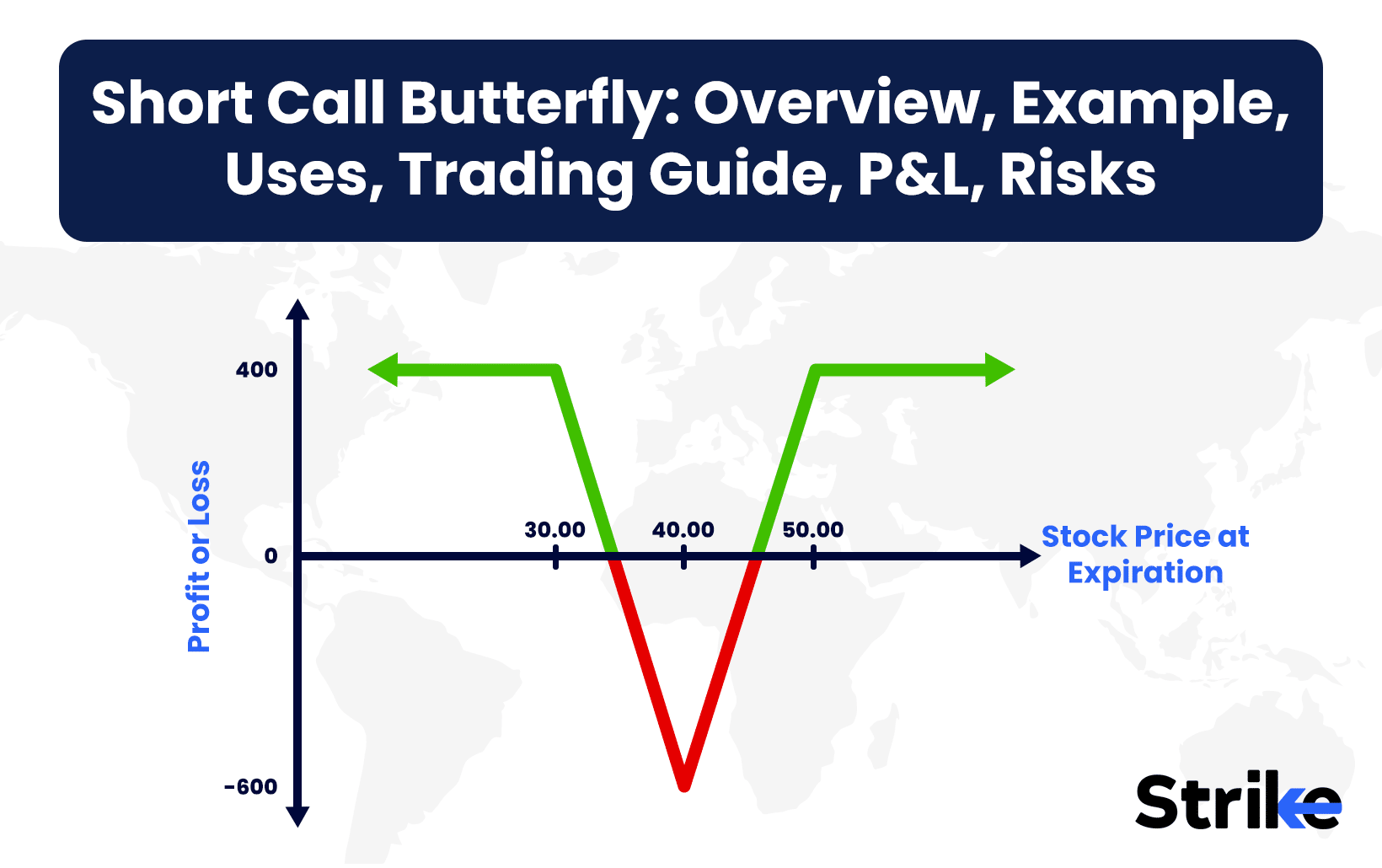

A short call butterfly is an options strategy created by selling one call at a lower strike price, buying two calls at a middle strike price, and selling one call at a higher strike price, with equal distances between strikes. Short call butterfly generates a net credit at trade entry due to the premium collected from short options exceeding the cost of long options.

The strategy profits from significant price movements in either direction away from the middle strike price. Maximum loss occurs at the middle strike, limited to the difference between strikes minus the initial credit received. Break-even points exist at prices equal to the middle strike plus or minus the net credit.

Position management data indicates adjustment points at 21 days to expiration. Risk metrics reveal maximum theta decay between 15-20 days remaining.

How Does a Short Call Butterfly Work?

A Short Call Butterfly works by selling two ATM Nifty call options and buying one ITM and one OTM call option with equal distance from the middle strike. This strategy profits when Nifty moves significantly away from the middle strike, either up or down.

Let’s take a real-world Nifty example – Suppose Nifty is trading around ₹22,000. You implement a Short Call Butterfly by buying 1 lot of 21,900 CE, selling 2 lots of 22,000 CE, and buying 1 lot of 22,100 CE — all with the same expiry. This creates a net credit because the sold options (ATM) carry the highest premium.

This position is volatility-based and benefits from a sharp Nifty move in either direction. If Nifty expires far below 21,900 or far above 22,100, the position results in a profit equal to the net credit received at initiation.

The maximum loss occurs if Nifty closes exactly at 22,000, the middle strike. At that level, both short 22,000 calls are fully in-the-money, and the 21,900 and 22,100 calls provide limited protection. This leads to the worst-case scenario for the trader.

The maximum gain equals the net premium received when placing the trade. This credit is collected upfront and is retained if Nifty lands outside the breakeven zones at expiry.

Breakeven points are calculated by adjusting the middle strike ± the wing width minus/plus the net credit. In our example, if the net credit is ₹30, and strikes are 100 points apart, the breakevens would be approximately ₹21,970 and ₹22,030.

This strategy is best used ahead of high-impact events like RBI policy announcements, election results, or Union Budgets, when traders expect a large move but are unsure of the direction.

Short Call Butterflies are ideal for range breakout scenarios. They allow traders to profit from volatility without picking a side, while also limiting both profit and loss.

Why Use a Short Call Butterfly Strategy?

A short call butterfly strategy is used to profit from price movement away from a specific level, making it popular among Nifty and Bank Nifty traders. The strategy benefits from high implied volatility environments, especially during quarterly results and major economic announcements.

Traders deploy this strategy on index options during expiry weeks to capitalize on accelerated time decay. The limited risk nature (maximum loss of ₹35) appeals to retail traders managing SEBI’s margin requirements.

Market makers utilize this strategy during volatile periods in heavyweights like HDFC Bank, TCS, and Infosys. The strategy excels in capturing both upside and downside moves while benefiting from volatility crush post-events.

When to Use a Short Call Butterfly?

A short call butterfly is used during high implied volatility environments, typically above the 75th percentile rank. Market conditions favoring this strategy include pre-earnings announcements, major economic events, or significant market uncertainty periods.

The optimal entry timing occurs with 30-45 days until expiration, allowing sufficient time for volatility contraction. Professional traders target underlying assets trading in established ranges with expected breakout potential.

Technical analysis suggests executing this strategy at key resistance or support levels. Strike selection focuses on 0.5-1 standard deviation intervals around the current price, maximizing probability of price movement beyond the wings.

Time decay benefits accelerate in the final 21 days, making position entry optimal before this window.

Market makers deploy this strategy in trending markets expecting increased volatility.

Exit signals in Option Trading include reaching 50% of maximum profit, breaching 150% of maximum loss, or approaching 21 days to expiration. Position adjustments in Option Trading become necessary as gamma risk increases significantly in the final three weeks.

How Option Greeks Affects Short Call Butterfly?

Option greeks affect short call butterfly through distinct risk measurements. Delta starts near zero due to the balanced nature of the position, making it initially direction-neutral. The strategy benefits from positive theta, earning daily time decay from the short options at the wings.

Vega exposure remains negative, profiting from volatility contraction. The position gains value as implied volatility decreases, particularly after major market events. Gamma risk increases significantly in the final 21 days before expiration, requiring active management.

Theta acceleration occurs in the last two weeks, contributing approximately 70% of the total profit potential. The position’s gamma exposure creates risk near the middle strike as expiration approaches.

Traders monitor delta changes to maintain neutrality in Option Greeks. Vega risk management in Option Greeks involves closing positions during low volatility periods. Position adjustments focus on maintaining balanced Greeks through rolling or closing at 21 days to expiration, where gamma exposure becomes potentially destabilizing.

How to Trade using Short Call Butterfly?

To trade using a Short Call Butterfly, you need to set up three strike prices: one in-the-money (ITM) call, two at-the-money (ATM) calls, and one out-of-the-money (OTM) call. Here’s an example. how to construct the position.

- Buy 1 ITM Call (e.g., 24000 CE at ₹200)

- Sell 2 ATM Calls (e.g., 24150 CEs at ₹105 each)

- Buy 1 OTM Call (e.g., 24300 CE at ₹55)

This setup leads to a total premium paid of ₹255 and premium received of ₹210, resulting in a net debit of ₹45 per lot. With a lot size of 75, your total upfront cost becomes ₹3,375, which is also the maximum loss possible.

This strategy achieves maximum profit when the index expires at the middle strike price, which in this case is ₹24150. At expiry, the 24000 CE would have an intrinsic value of ₹150, translating to ₹11,250. Since the 24150 CEs and the 24300 CE expire worthless, there’s no further payout. After subtracting the initial cost of ₹3,375, the maximum profit becomes ₹7,875.

The breakeven points for this trade are calculated as:

- Lower Breakeven = 24000 + 45 = ₹24045

- Upper Breakeven = 24300 − 45 = ₹24255

Any expiry between ₹24045 and ₹24255 results in a profit that tapers off as the price moves away from the center strike. Outside this zone, the position incurs the maximum loss of ₹3,375.

In case the index expires below ₹24000, all options expire worthless, and you lose the net debit paid. In case it expires above ₹24300, the long 24300 CE gains value, but the two short 24150 CEs lose more rapidly, causing the losses to mount and settle at the same fixed loss level.

To trade the Short Call Butterfly effectively look for a consolidation zone or resistance area where the price is likely to stall. Enter the strategy when volatility is high and you’re expecting it to drop, as this will benefit the short options. Manage the position till expiry, as most gains are realized when the price pins at or near the middle strike.

How to Adjust a Short Call Butterfly?

A short call butterfly is adjusted through specific methods based on price movement and time decay factors. The primary adjustment occurs at 21 days to expiration due to increasing gamma risk. Rolling the entire position forward maintains the same strikes while extending duration to the next monthly expiration.

Directional adjustments respond to underlying price movement beyond break-even points. Moving all strikes up or down by equal amounts re-centers the position around the current price. The roll executes by closing the existing butterfly and simultaneously opening a new position at adjusted strikes.

Volatility-based adjustments involve widening the wing strikes during volatility spikes. This modification increases the probability of profit by expanding the profitable price range. Professional traders implement this adjustment by closing the outer strikes and selling new calls at wider intervals.

Time-based adjustments focus on reducing position size as expiration approaches. Closing half the position at 50% profit preserves gains while maintaining upside potential. Additional risk management includes adding vertical spreads to defend against directional moves.

Market makers prefer early adjustments at 30% profit or loss thresholds.

What are the Risks of Short Call Butterfly?

The main risk of using a short call butterfly is Gamma risk, which escalates significantly in the final 21 days before expiration, creating potential for rapid position value changes. The strategy suffers maximum loss at the middle strike price, typically 2-3 times the initial credit received.

Pin risk emerges near expiration with the underlying price close to any strike price. This scenario creates assignment uncertainty and potential overnight risk. The position faces increased volatility risk during major market events, earnings announcements, or economic data releases.

Liquidity risk impacts position adjustments, particularly in individual stock options. Wide bid-ask spreads reduce profit potential and increase transaction costs. Early assignment risk exists on the short calls, disrupting the position’s balanced nature.

Time decay works against the position during slow market moves near the middle strike. The strategy underperforms in low volatility environments, leading to opportunity cost. Delta risk increases as the underlying moves away from the center strike, creating directional exposure.

Traders mitigate these risks through strict position sizing (2-3% of portfolio), active management at 21 days to expiration, and immediate adjustments beyond break-even points. Market makers implement gamma scalping techniques to defend against adverse price movement.

Is Short Call Butterfly Strategy Profitable?

Yes, the Short Call Butterfly strategy is profitable in trending markets when the underlying asset moves significantly away from the middle strike. This strategy thrives on volatility and directional breakouts, though it is structured as a non-directional setup.

The basic structure involves buying one lower strike call, selling two at-the-money calls, and buying one higher strike call — all with the same expiration. The resulting position benefits when the underlying index or stock breaks out in either direction, well beyond the outer strikes.

The profitability hinges on the premium collected at initiation. Since the short calls are sold at-the-money, they bring in more premium than the long calls bought at the wings. This leads to a net credit, which becomes the maximum potential profit.

However, trending markets are required to make this strategy effective. If the underlying asset lingers near the middle strike, losses grow due to the short calls being exercised while the long calls offer limited protection.

This strategy also benefits from time decay, especially when the underlying stays away from the danger zone near expiry. Theta becomes an ally when the price trends early, and the position is exited before expiration.

Is Short Call Butterfly Bullish or Bearish?

The short call butterfly is neither bullish nor bearish – it profits from significant price movement in either direction. The strategy benefits from the underlying moving away from the middle strike price. Maximum profit materializes at expiration with prices moving beyond the outer strikes (above highest or below lowest strike).

The position starts delta-neutral due to its balanced structure. Professional traders utilize this strategy during high volatility periods, expecting sharp price movements. Market statistics show equal profit potential in both upward and downward price scenarios. The strategy performs best in trending markets with clear directional movement away from the initial price level.

What’s the difference between Short Call Butterfly vs Long Call Butterfly?

The difference between short call butterfly and long call butterfly lies in their construction and profit patterns.

| Strategy | Construction | Initial | Max Profit | Max Loss | Best Market |

| Short Call Butterfly | Sell wings, Buy middle | Credit | Limited (Credit) | Width-Credit | Trending |

| Long Call Butterfly | Buy wings, Sell middle | Debit | Width-Debit | Limited (Debit) | Range-bound |

Short call butterfly sells the wings and buys the middle strikes, generating initial credit and profiting from price movement away from the middle. Long call butterfly buys the wings and sells the middle strikes, requiring initial debit and profiting from price consolidation around the middle.

The short butterfly benefits from volatility expansion and time decay, performing best in trending markets. The long butterfly gains from volatility contraction and performs optimally in range-bound conditions. Maximum profit for short butterfly occurs beyond outer strikes, while long butterfly maximizes profit at the middle strike price at expiration.

What are Alternatives to Short Call Butterfly Strategy?

The alternatives to the Short Call Butterfly strategy are Straddle, Strangle, Iron Condor, Calendar Spread, and Vertical Spread.

A straddle is a strong alternative to a short call butterfly when expecting a large move but unsure of the direction. Unlike the butterfly, the straddle does not have capped risk, and it involves buying both a call and a put at the same strike price.

This strategy thrives in high-volatility environments, where large price swings are likely. It is ideal during events like earnings, economic announcements, or elections, when the market often reacts sharply.

The structure is simple: buy one at-the-money call and one at-the-money put, both with the same expiration. The combined premium paid is the maximum risk, and the profit potential is theoretically unlimited in either direction.

However, straddles require a significant move to become profitable, since the initial cost is usually high. If the price remains near the strike, both options lose value quickly due to time decay.

A strangle is a looser version of the straddle and serves as an effective alternative to a short call butterfly for directional uncertainty. It involves buying an out-of-the-money call and an out-of-the-money put, thereby reducing cost but increasing the required move for profit.

This strategy suits traders who are confident about volatility expansion but want to reduce premium exposure. Lower initial cost compared to a straddle makes it appealing in moderately volatile markets.

The structure consists of two legs: one OTM call above the current price and one OTM put below it. Since both options are cheaper than ATM options, the total debit is smaller than a straddle’s.

Profit is achieved when the underlying price moves strongly in either direction beyond the breakeven levels. These levels are the call strike plus total premium or the put strike minus total premium. Compared to a short call butterfly, the strangle offers a wider profit zone and uncapped return potential. It does not rely on expiration-day behavior as much and reacts faster to price movement.

The iron condor is a conservative alternative to the short call butterfly, designed to profit from price stability. It combines a bear call spread and a bull put spread to create a wide zone of maximum gain.

This strategy works best in low-volatility, range-bound conditions. When the underlying asset trades within a defined range, the condor collects and retains premium as all legs expire worthless.

The structure involves selling an OTM call and an OTM put, while buying further OTM options as protection. The result is a net credit with limited risk and limited reward.

The maximum profit equals the net premium received, which is achieved if the asset finishes between the short strikes. Loss occurs only if the price breaches either side of the range.

Iron condors require careful strike selection and timing. Entering when implied volatility is high ensures better premiums and more cushion against losses.

A calendar spread is a time-based alternative to a short call butterfly that benefits from volatility shifts and time decay. It involves buying and selling options of the same strike but with different expirations.

This strategy profits when the underlying price stays near the strike of the short option. As time passes, the near-term option decays faster, while the longer-dated option retains more value.

The most common calendar spread is the long calendar, where a trader sells a short-dated option and buys a longer-dated one at the same strike. The goal is to benefit from the differential in time decay.

The risk is limited to the net debit paid. Profit is also limited and usually peaks when the price stays near the strike at expiration of the short option.

Calendar spreads are ideal for traders expecting consolidation around a specific level. They are often used before

Share

No Comments Yet