Editor

Editor  Updated on 12 June 2025

Updated on 12 June 2025

Long iron condor involves selling an out-of-the-money put spread and call spread simultaneously. Long iron condor profits from price consolidation and declining volatility, making it popular among Indian option traders during range-bound markets.

This strategy is widely used by professional traders, especially in the Indian derivatives market on instruments like Nifty and Bank Nifty.

Iron condors are ideal during periods of low volatility, where the underlying is expected to consolidate. According to market data from NSE, over 65% of Bank Nifty’s trading sessions in a year remain within a 5% range, making the iron condor highly relevant for capturing premium decay during such phases. Historical backtests show that iron condors with 30–45 days to expiry and 30–35% of strike width as credit offer the best risk-reward outcomes.

Risk is capped to the difference between strike prices minus the credit received, while profit is limited to the net premium collected. The strategy works best when implied volatility is high at entry and expected to decline. Traders often use a 3–5% portfolio allocation per condor and target a 50% profit booking rule to enhance consistency and reduce drawdowns.

What is a Long Iron Condor?

Long iron condor represents a four-legged options strategy combining a bull put spread and a bear call spread with the same expiration date. Long iron condor provides limited risk and limited reward, designed to profit from range-bound price action and declining volatility.

The construction involves selling an out-of-the-money put, buying a further out-of-the-money put, selling an out-of-the-money call, and buying a further out-of-the-money call. The distance between strikes remains equal, creating a balanced risk-reward profile.

Market makers utilize this strategy extensively in the Indian markets, particularly on indices like Nifty and Bank Nifty. Professional traders implement the strategy with 30-45 days to expiry, targeting a credit of 30-35% of the width between strikes.

Position sizing plays a crucial role in success. Statistics reveal optimal results with 3-5% portfolio allocation per trade. Professional traders close positions at 50% profit or double the credit received as maximum loss, maintaining strict risk management parameters.

How Does a Long Iron Condor work?

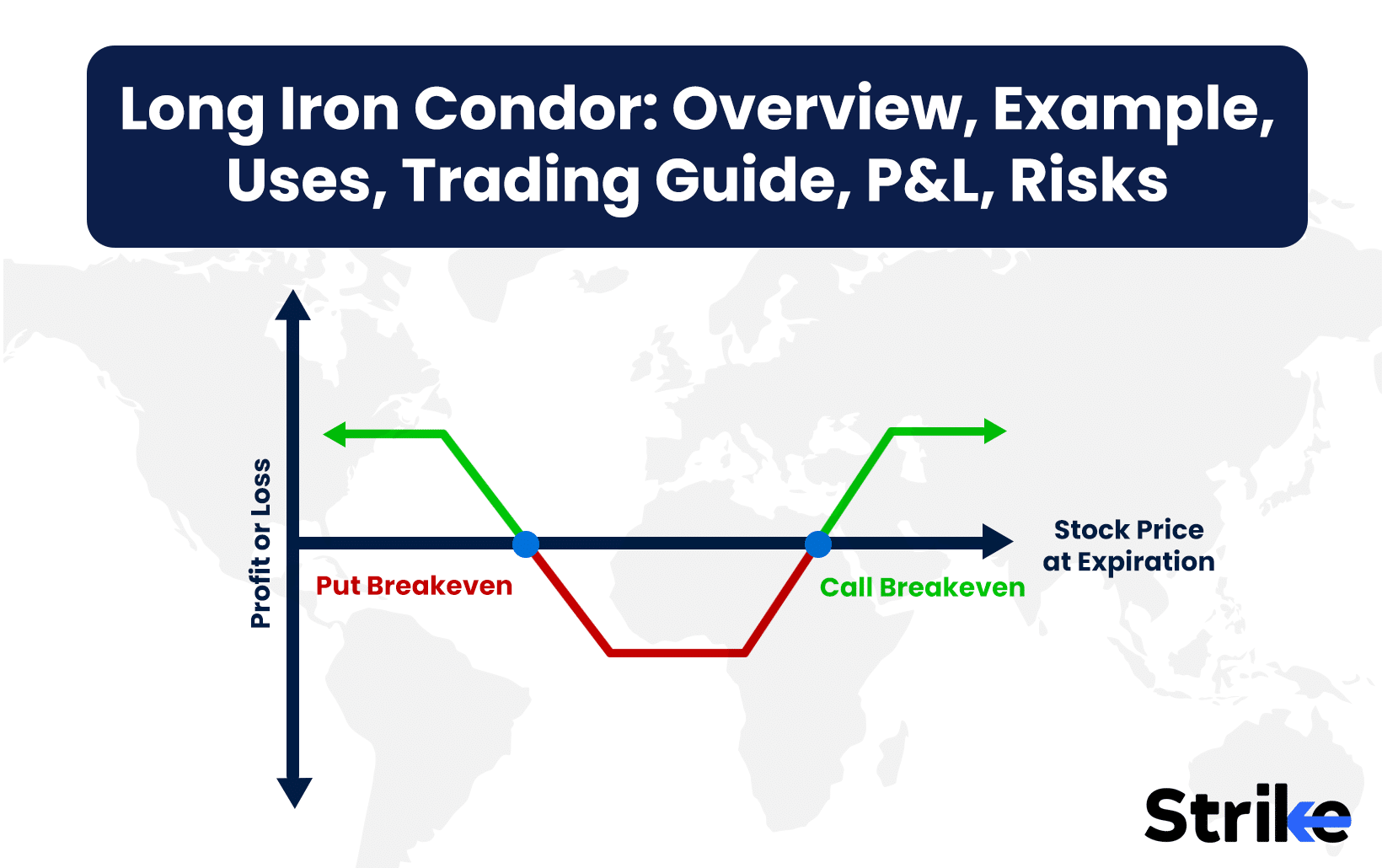

An iron condor works when the underlying asset’s price is expected to range between two important price points. A credit spread on a call and put are deployed simultaneously, making it a 4-legged strategy. A one-sided price momentum is not expected. The goal is to collect a net credit upfront and let time decay work in your favor while the price stays consolidated between the two strike prices. Iron condors are popularly called a non-directional 4-legged strategy.

Long iron condor / reverse iron condor strategy is deployed when the market has been consolidating but is expected to break out in either direction near expiry. It is a debit strategy, meaning a net premium is paid upfront.

The idea is to benefit from volatility expansion and directional movement. The trade becomes profitable when the underlying closes outside the breakeven points on either side.

This is a four-legged strategySell 1 Far OTM Put 24000 PE @ ₹100

- Buy 1 OTM Put 24050 PE @ ₹115

- Buy 1 OTM Call 24450 CE @ ₹111

- Sell 1 Far OTM Call 24500 CE @ ₹95

Lot size is 75. Premium received is ₹195 (₹100 + ₹95), and premium paid is ₹226 (₹115 + ₹111). Therefore, the net debit is ₹31.

The total net debit is ₹31 × 75 = ₹2,325. This is the maximum loss in the trade. Loss occurs when the price expires between the two bought strikes: 24050 and 24450.

When this happens, none of the options provide enough intrinsic value, and the net debit becomes the loss. Maximum loss = ₹2,325.

Maximum profit occurs when the underlying expires outside the outer strikes. This means the price ends either below 24000 or above 24500.

In such cases, the far OTM options expire worthless, and the inner options provide the maximum spread. Wing width = 50 points.

Max Profit = Wing Width − Net Debit = ₹50 − ₹31 = ₹19

Total Profit = ₹19 × 75 = ₹1,425

- Lower Breakeven (LB) = Lower Long Put Strike − Net Debit = 24050 − 31 = ₹24019

- Upper Breakeven (UB) = Upper Long Call Strike + Net Debit = 24450 + 31 = ₹24481

Profits occur when the underlying expires outside these breakeven levels.

Short Iron Condor is used after a strong one-sided move, with the expectation that the market will now consolidate. It’s a credit strategy, where a net premium is received upfront.

The goal is for the price to remain in a narrow range until expiry. This allows all options to decay in value, enabling the trader to retain the credit as profit.

- Sell 1 OTM Call 24650 CE @ ₹50

- Buy 1 Far OTM Call 24900 CE @ ₹20

- Sell 1 OTM Put 23700 PE @ ₹50

- Buy 1 Far OTM Put 23350 PE @ ₹25

Lot size is 75. Total premium received is ₹100 (₹50 from call + ₹50 from put), and total premium paid is ₹45 (₹20 + ₹25). Net credit = ₹55.

The maximum profit is the net credit collected, which is ₹55 × 75 = ₹4,125. This occurs when the underlying expires between the sold strikes: 23700 and 24650.

All options expire worthless in this zone. Hence, the trader keeps the premium.

Max loss happens when the price moves beyond the outer wings—below 23350 or above 24900. These positions generate losses because the bought options are insufficient to hedge.

Wing width is calculated separately for both sides:

- Calls: 24900 − 24650 = 250

- Puts: 23700 − 23350 = 350

Since the put wing is wider, we use that. Max loss = 350 − 55 = ₹295

Total Max Loss = ₹295 × 75 = ₹22,125

- Lower Breakeven (LB) = Lower Sold Put − Net Credit = 23700 − 55 = ₹23645

- Upper Breakeven (UB) = Higher Sold Call + Net Credit = 24650 + 55 = ₹24705

Losses begin beyond these breakeven points. Staying within them ensures profitability.

What is an Example of Long Iron Condor?

Let us take a look at an example of Bank Nifty, which is currently trading near its all-time high levels. At such elevated positions, the price typically continues its trend, halts temporarily, or reverses to consolidate within a wider price range.

With 26 days left to expiry, far out-of-the-money options have been selected. These strikes are sold with the expectation that the price will not reach them, and they will lose value quickly due to theta decay.

The range chosen is broad on both sides. Regardless of volatility, the price needs to expire within the two major strike levels in 26 days for the trade to be profitable.

This setup is a short Iron Condor strategy. It is built by combining a call credit spread and a put credit spread, both positioned far away from the current price. Below is the payout structure.

The position involves four legs: sell 1 call option at 57600 for ₹300, buy 1 call option at 58600 for ₹150, sell 1 put option at 52300 for ₹300, and buy 1 put option at 50700 for ₹150. The lot size is 30.

The total premium received from selling the call and put is ₹600. The total premium paid for buying the hedge options is ₹300.

This results in a net credit of ₹300. The total credit collected for the trade is ₹300 × 30 = ₹9,000.

This is the maximum profit possible from the position. It occurs when the underlying price stays between 52300 and 57600 at expiry.

At this range, all options expire worthless. The entire premium received is retained as profit.

The maximum loss occurs when the price moves beyond the outer strikes — below 50700 or above 58600. In such cases, the sold option on one side becomes deep in-the-money, and the hedge is not enough to offset the loss.

To find the worst-case scenario, the wider wing is identified. The call wing is 1000 points wide (58600 − 57600), and the put wing is 1600 points wide (52300 − 50700).

Since the put wing is wider, the downside is riskier. The maximum loss per unit is calculated as 1600 − 300 = ₹1300.

The total maximum loss is ₹1300 × 30 = ₹39,000. This is the worst-case amount the trader would lose if Bank Nifty breaches the outer downside strike.

Breakeven points define the limits beyond which losses begin. The lower breakeven is 52300 − 300 = ₹52000.

The upper breakeven is 57600 + 300 = ₹57900. Any expiry within ₹52000 and ₹57900 will result in partial or full profit.

This strategy works best when the price stays within this large but defined range over the next 26 days. The focus is on time decay and range-bound price action.

Why Use a Long Iron Condor Strategy?

A long iron condor strategy is used to profit from strong directional moves in the Indian markets while maintaining defined risk parameters. The strategy proves effective during periods of expected volatility expansion, particularly around major market events like quarterly results, budget announcements, or monetary policy decisions.

The strategy appeals to traders seeking leveraged exposure with limited downside risk. The defined risk-reward structure protects against catastrophic losses while offering substantial profit potential. Position sizing plays a crucial role in strategy implementation. Professional traders allocate 2-3% of portfolio value per trade, maintaining strict risk management parameters. Historical data indicates improved outcomes through early profit-taking at 50-60% of maximum potential gain.

The strategy excels during periods of increased market uncertainty. Recent studies show 75% of profitable trades coincided with VIX readings above the 75th percentile. Market makers utilize this strategy extensively during event-driven volatility spikes, targeting 40-50% returns within the defined holding period. The structured approach to risk management appeals to institutional traders seeking consistent, repeatable results in volatile market conditions.

When to Use a Long Iron Condor?

A long iron condor is best used in a low-volatility, range-bound market where you expect the underlying asset to stay within a specific price range until option expiration. This strategy profits when the asset price remains between the two short strikes, with minimal directional movement. Below is a similar example.

The ideal time to implement this strategy is when implied volatility is relatively high and expected to decline. A drop in implied volatility after entering the trade helps all four legs of the condor lose value, benefiting the net credit seller.

Traders turn to this setup when they believe there’s no strong catalyst—like earnings, economic data, or geopolitical events—that would move the asset significantly. It is also useful when technical indicators suggest consolidation, such as support and resistance patterns or moving averages flattening out.

Time decay plays a crucial role in the iron condor’s profitability. As expiration approaches, the time value of the options diminishes, particularly the short strikes, which are ideally both out-of-the-money.

An effective long iron condor setup requires careful strike selection. The short strikes should be within the expected trading range, while the long wings provide protection from large moves beyond that range.

This strategy is often used on index options or liquid ETFs, which tend to move more predictably and with less volatility than individual stocks. Liquidity ensures tighter bid-ask spreads, reducing slippage and improving execution.

Traders often monitor the implied volatility rank or percentile to judge whether the current volatility level is high enough to justify opening a condor. Higher implied volatility increases the premium received, which improves the risk-to-reward ratio.

How Option Greeks Affects Long Iron Condor?

The long iron condor benefits from Theta decay and a drop in Vega, while being minimally exposed to Delta and Gamma.

| Greek | Effect on Iron Condor | Explanation |

| Delta | Neutral at initiation | Directional exposure is minimal; the strategy doesn’t benefit from up or down moves. |

| Gamma | Low, but increases near short strikes | Sensitivity to price movement rises sharply as the underlying nears the short call or put strike. |

| Theta | Positive | Time decay works in your favor; short options lose value faster, increasing profit if price stays in range. |

| Vega | Negative | A fall in implied volatility benefits the trade; rising volatility increases risk and option value. |

Understanding these Greeks also aids in adjustment decisions. For instance, if Delta skews due to price movement, one might roll the position or adjust strikes to rebalance.

What is the Maximum Profit & Loss, Breakeven on a Long Iron Condor?

The maximum profit on a long iron condor is the net credit received when opening the trade. This occurs when the underlying asset finishes between the short call and short put at expiration.

All options expire worthless in this case, and the trader keeps the premium collected. This is the best-case scenario for this neutral strategy.

The maximum loss is the difference between the long and short strikes on one side, minus the net credit. This happens if the underlying moves beyond either long strike, causing one spread to be fully in-the-money.

There are two breakeven points on a long iron condor—one below the short put and one above the short call. The lower breakeven is the short put strike minus the net credit, and the upper breakeven is the short call strike plus the net credit.

The strategy ends in profit if the underlying finishes between these two points. Outside of them, the trade incurs a loss, up to the maximum defined.

Knowing these numbers helps in planning position size and exit strategies. It also helps set alerts or stop-loss levels based on the underlying’s price movement.

Traders often use risk-reward ratios to evaluate whether a condor is worth the capital. A good ratio is typically 1:2 or better, where potential profit is at least half the max risk.

How to Adjust a Long Iron Condor?

A long iron condor is adjusted by shifting the strike prices, rolling the position, or converting it into another strategy when the underlying price moves near the breakevens. Adjustments aim to reduce risk or lock in profits if the market doesn’t behave as expected.

One common method is to roll the threatened side—either the call spread or put spread—further away from the current price. This involves closing the existing short leg and opening a new spread at strikes farther from the underlying, widening the range.

The trader adjusts the call side upwards if the underlying trends higher and approaches the short call strike. This shifts the risk range and gives the position more room to breathe without taking a significant directional stance.

Another technique is to roll the entire iron condor to a later expiry, especially if there’s still time left and the position is at risk. This allows the trader to collect more premium, extend time decay benefits, and reposition the strikes around the new price action.

In some cases, a trader may convert the iron condor into a butterfly spread by bringing the long wings closer to the short strikes. This reduces margin but also narrows the profit range, and is used when the market settles near the center.

A partial adjustment is possible if volatility increases and breakevens are threatened. The trader might close just one side—say the call spread if the market is rallying—and leave the put side open to continue profiting from time decay.

Another strategy involves adding a new iron condor around the new price range. This is called layering, and it helps maintain neutrality while collecting additional premium, but it increases exposure and complexity.

Adjustments also include reducing position size or cutting losses early. This is not an adjustment in the traditional sense, but it’s a valid risk management decision that preserves capital and avoids large drawdowns.

Timing matters in all of these tactics. Adjusting too early may lead to overtrading, while waiting too long risks turning a manageable position into a losing trade.

Each adjustment carries a cost, whether it’s additional commissions, reduced credit, or increased risk. Therefore, decisions must be based on a clear plan rather than reacting emotionally to price movement.

What are the Risks of Long Iron Condor?

The primary risk of a long iron condor is a sharp move in the underlying asset that pushes the price beyond the breakeven points. This leads to a loss that, while capped, still affects the portfolio due to the defined spread width.

The strategy is vulnerable to trending markets or sudden breakouts. If price moves quickly in one direction, one side of the condor becomes fully in-the-money, and the loss approaches its maximum.

Another major risk is a rise in implied volatility after entering the trade. Since the iron condor is Vega negative, higher volatility inflates option premiums, increasing the cost to exit or adjust the position.

This is especially dangerous if the volatility spike is driven by unexpected events such as geopolitical news, policy changes, or poor earnings data. These events can quickly turn a calm market into a volatile one, harming the position.

Time decay, while generally favorable, also becomes a risk when the position is losing and there’s not enough time to recover. The closer you are to expiration, the harder it becomes to make meaningful adjustments.

There’s also the psychological risk of holding on too long, hoping for mean reversion. Traders sometimes delay exiting losing trades, expecting the price to return to the center range, which rarely works out well.

Slippage and poor liquidity add to the risk, especially in less active instruments or during off-market hours. Wider bid-ask spreads reduce profits and increase losses when trying to exit or adjust trades.

Margin requirements can also change suddenly, especially in volatile markets. A widening of spreads or large movements could lead to higher capital requirements or forced liquidations in leveraged accounts.

Furthermore, the strategy has a poor risk-to-reward ratio. You risk more to earn less, which means a few large losses can wipe out gains from multiple profitable trades.

To mitigate these risks, traders use smaller position sizing, set stop-loss rules, and avoid trading near major events. They also ensure they monitor implied volatility levels before entry, aiming to sell when volatility is high and expected to drop.

Is Long Iron Condor Strategy Profitable?

Yes. the long iron condor strategy is profitable when the underlying stays within a defined range and implied volatility drops after entry. It works best in low-volatility, sideways markets where price movement is limited.

The position earns a net credit upfront, and the goal is to retain most or all of that credit by expiration. Profit is maximized when all options expire worthless, meaning the price finishes between the two short strikes.

Unlike directional strategies that depend on strong moves, the long iron condor thrives on stability. As time passes and the underlying remains range-bound, the time value of the short options erodes, boosting profitability.

However, the potential reward is limited, and the risk-to-reward ratio is typically low. This means consistent small profits are needed to offset occasional large losses when the underlying breaks out of the range.

To enhance profitability, traders often choose expirations with higher implied volatility and look to sell iron condors when volatility is expected to fall. This allows them to collect richer premiums and benefit from a volatility crush.

Is Long Iron Condor Bullish or Bearish?

The long iron condor is neither bullish nor bearish—it is a neutral strategy. It is designed to profit when the underlying stays within a specific price range around the current market level.

This neutrality makes it appealing during periods of consolidation, when there’s no clear trend in either direction. Rather than predicting price movement, the trader focuses on where the asset is unlikely to go.

The structure relies on selling both a put spread and a call spread, equidistant from the current price. This forms a profit zone in the middle and creates losses only if the price moves too far up or down.

Because of this construction, the long iron condor does not benefit from bullish or bearish moves. In fact, it suffers when the market trends strongly in either direction, especially if it breaks through breakeven levels.

The strategy is ideal for non-directional views, especially when implied volatility is high and expected to contract. It rewards patience and timing, not directional forecasting.

What are Alternatives to the Long Iron Condor Strategy?

Alternatives to the long iron condor include strategies like the iron butterfly, calendar spread, straddle, and strangle, which also aim to benefit from time decay or range-bound movement. These strategies differ in terms of risk-reward profiles, breakeven zones, and sensitivity to volatility.

The iron butterfly is similar to the iron condor but uses the same strike for both the short call and short put, creating a narrower profit zone but offering higher potential profit. It’s suitable when the trader expects very little movement.

A calendar spread involves selling a near-term option and buying a longer-term option at the same strike. It profits from time decay and volatility changes, especially when price stays near the strike price.

The straddle and strangle are non-neutral alternatives, used when large movements are expected. A short straddle profits if price stays at the strike, while a short strangle allows for a wider range but offers smaller premium.

Each of these strategies has its own trade-offs in terms of risk, reward, and complexity. The best alternative depends on the trader’s market view, volatility outlook, and risk tolerance.

Previous Article

Previous Article

![85 Common Stock Market Terminologies for Dummies [Updated List for 2025]](https://www.strike.money/wp-content/uploads/2025/04/Popular-Stock-Market-Terms-for-Beginners-Banner.png "85 Common Stock Market Terminologies for Dummies [Updated List for 2025] 136")

No Comments Yet.